CTP N.V. Q1-2024 Results

CTP REPORTS COMPANY SPECIFIC ADJUSTED EPRA EPS OF €0.20 DRIVEN BY STRONG LIKE-FOR-LIKE RENTAL GROWTH OF 5.0%; EPRA NTA PER SHARE UP TO €16.50

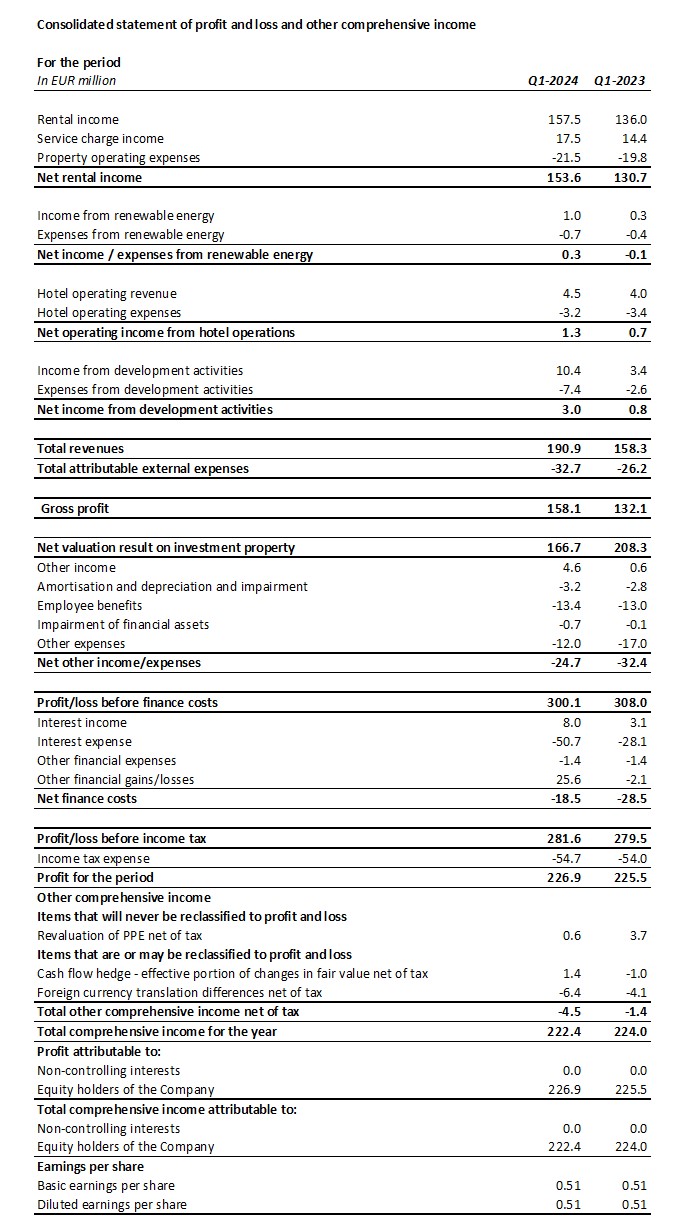

AMSTERDAM, 9 May 2024 – CTP N.V. (CTPNV.AS), (“CTP”, the “Group” or the “Company”) recorded in Q1-2024 Net Rental Income of €153.6 million, up 17.5% y-o-y, and like-for-like y-o-y rental growth of 5.0%, mainly driven by indexation and reversion on renegotiations and expiring leases. As at 31 March 2024, the contracted revenues for the next 12 months stood at €742 million and occupancy at quarter-end was 93%.

In the quarter, CTP delivered 169,000 sqm at a YoC of 10.7% and 95% let at completion, bringing the Group’s standing portfolio to 12.0 million sqm of GLA, while the Gross Asset Value (“GAV”) increased by 2.8% to €14.0 billion. EPRA NTA per share increased by 3.7% in the quarter to €16.50.

Company specific adjusted EPRA earnings increased by 11.7% y-o-y to €87.4 million. CTP’s Company specific adjusted EPRA EPS amounted to €0.20, an increase of 10.7%. The Group confirms its €0.80 – €0.82 Company specific adjusted EPRA EPS guidance for 2024.

As at 31 March 2024, projects under construction totaled 2.0 million sqm, most of which will be delivered in 2024, with a potential rental income of €146 million when fully leased and an expected yield on cost of 10.3%.

The Group’s landbank of 23.1 million sqm, of which 17.5 million sqm is owned and on-balance sheet, offers substantial secured future growth potential to CTP. With assuming a build-up ratio of 2 sqm of land to 1 sqm of GLA, CTP has the ability to build over 11 million sqm of GLA on its secured landbank. CTP’s land on balance sheet is held at around €50 per sqm and construction costs amount on average to approximately €500 per sqm, bringing total investment costs to approximately €600 per sqm. The Group’s standing portfolio is valued around €950 per sqm, which implies a revaluation potential of €350 per sqm of GLA build. CTP also expects to continue to make further land acquisitions to add to its future growth potential, with the Group track record of delivering over 10% new GLA per year.

Demand for industrial and logistics real estate in the CEE region is driven by structural demand drivers, such as professionalization of supply chains by 3PLs, e-commerce, and occupiers nearshoring and friend-shoring, as the CEE region offers the best cost location in Europe. We have now nearly 10% of our portfolio leased to Asian tenants which are producing in Europe for Europe.

Since our IPO in March 2021 we have more than doubled the GLA from 5.9 million to 12.0 million, grown the EPRA NTA per share by 98% from €8.32 to €16.50 and increased the Next 12 months contracted revenues by 116% from €344 million to €742 million. This is just the beginning, as the next growth phase is already locked in with our 2 million sqm of GLA under construction and 23.1 million sqm landbank.

We are confident that we can achieve our ambitious goals and reach 20 million sqm of GLA and over 1.2 billion annualized rental income before the end of the decade.”

Key Highlights

| In € million | Q1-2024 | Q1-2023 | % Increase |

| Gross Rental Income | 157.5 | 136.0 | +15.8% |

| Net Rental Income | 153.6 | 130.7 | +17.5% |

| Net valuation result on investment property | 166.7 | 208.3 | -20.0% |

| Profit for the period | 226.9 | 225.5 | +0.6% |

| Company specific adjusted EPRA earnings | 87.4 | 78.3 | +11.7% |

| In € | Q1-2024 | Q1-2023 | % Increase |

| Company specific adjusted EPRA EPS | 0.20 | 0.18 | +10.7% |

| In € million | 31 March 2024 | 31 Dec. 2023 | % Increase |

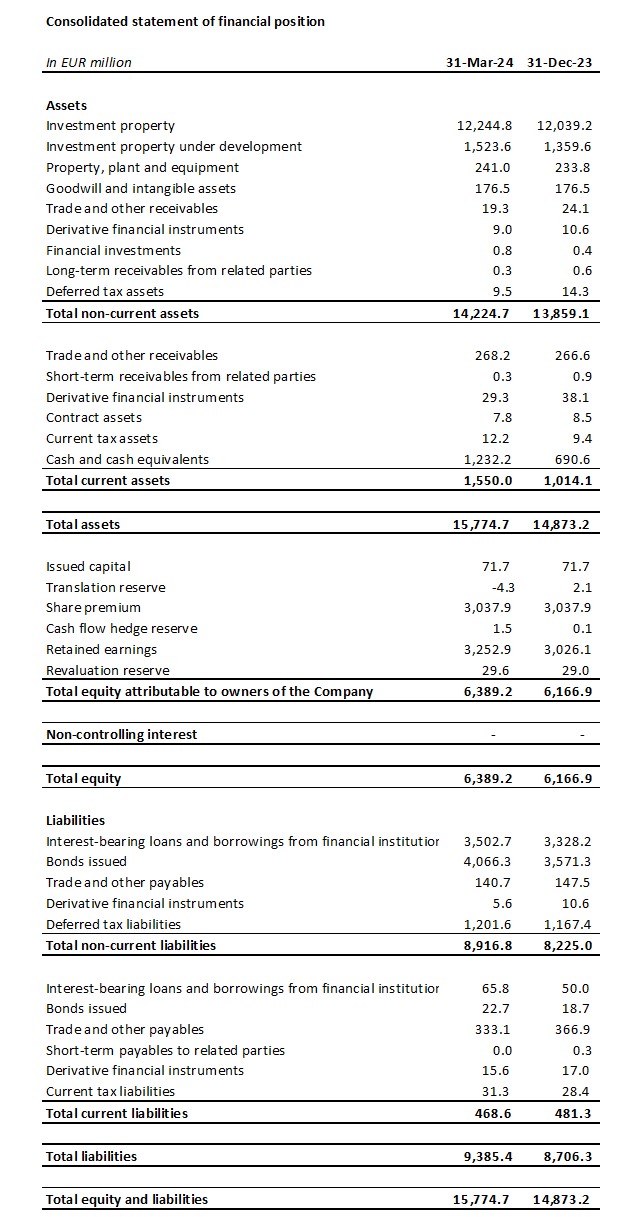

| Investment Property (“IP”) | 12,244.8 | 12,039.2 | +1.7% |

| Investment Property under Development (“IPuD”) | 1,523.6 | 1,359.6 | +12.1% |

| 31 March 2024 | 31 Dec. 2023 | % Increase | |

| EPRA NTA per share | €16.5 | €15.92 | +3.7% |

| Expected YoC of projects under construction | 10.3% | 10.3% | |

| LTV | 45.9% | 46.0% |

Continued strong tenant demand, 13% more sqm signed than the same quarter last year

In Q1-2024, CTP signed leases for 336,000 sqm, an increase of 13% compared to Q1-2023, with contracted annual rental income of €23 million, and an average monthly rent per sqm of €5.65 (Q1-2023: €5.31).

| Leases signed by sqm | Q1 | Q2 | Q3 | Q4 | FY |

| 2023 | 297,000 | 552,000 | 585,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 |

| Average monthly rent leases signed per sqm (€) | Q1 | Q2 | Q3 | Q4 | FY |

| 2023 | 5.31 | 5.56 | 5.77 | 5.81 | 5.69 |

| 2024 | 5.65 |

Around two-thirds of those leases were with existing tenants, in line with CTP’s business model of growing with existing tenants in existing parks.

CTP’s average market share in the Czech Republic, Romania, Hungary, and Slovakia stands at 27.4% as at 31 March 2024 and it remains the largest owner and developer of industrial and logistics real estate assets in those markets. The Group is also the market leader in Serbia and Bulgaria.

With over 1,000 clients, CTP has a wide and diversified international tenant base, consisting of blue-chip companies with strong credit ratings. CTP’s tenants represent a broad range of industries, including manufacturing, high-tech/IT, automotive, e-commerce, retail, wholesale, and third-party logistics. This tenant base is highly diversified, with no single tenant accounting for more than 2.5% of its annual rent roll, which leads to a stable income stream. CTP’s top 50 tenants only account for 32% of its rent roll and most are in multiple CTParks.

The Company’s occupancy came to 93%. The Group’s client retention rate remains strong at 94% (Q1-2023: 95%) and demonstrates CTP’s ability to leverage long-standing client relationships. The portfolio WAULT stood at 6.6 years (FY-2023: 6.6 years), in line with the Company’s target of >6 years.

Rent collection level stood at 99.9% in Q1-2024 (FY-2023: 99.9%), with no deterioration in payment profile.

Rental income amounted to €157.5 million, up 15.8% y-o-y on an absolute basis. On a like-for-like basis, rental income grew 5.0%, mainly driven by indexation and reversion on renegotiations and expiring leases.

The Group has put measures in place to limit service charge leakage, especially in the Czech Republic and Germany, which resulted in the improvement of the Net Rental Income to Rental Income ratio from 96.0% in Q1-2023 to 97.5% in Q1-2024. Consequently, the Net Rental Income increased 17.5% y-o-y.

An increasing proportion of the rental income generated by CTP’s investment portfolio benefits from inflation protection. Since end-2019, all the Group’s new lease agreements include a double indexation clause, which calculates annual rental increases as the higher of:

- a fixed increase of 1.5%–2.5% a year; or

- the Consumer Price Index[1].

As at 31 March 2024, 68% of income generated by the Group’s portfolio includes this double indexation clause, and the Group expects this to increase further.

The reversionary potential stands at 14.5%[2]. New leases have been signed continuously above ERV’s, illustrating continued strong market rental growth and supporting valuations.

The contracted revenues for the next 12 months stood at €742 million as at 31 March 2024, increasing 18.2% y-o-y, showcasing the strong cash flow growth of CTP’s investment portfolio.

Q1-2024 developments delivered with a 10.7% YoC and 95% let at delivery

CTP continued its disciplined investment in its highly profitable pipeline.

In Q1-2024, the Group completed 169,000 sqm of GLA (Q1-2023: 223,000 sqm), slightly below last year when several projects came online that were postponed during the year 2022 due to the higher construction costs. The developments were delivered at a YoC of 10.7%, 95% let and will generate contracted annual rental income of €9.8 million, with another €0.6 million to come when these reach full occupancy.

Some of the main deliveries during Q1-2024 were: 39,000 sqm in CTPark Zabrze, 34,000 sqm in CTPark Novi Sad East; 24,000 sqm in CTPark Bucharest West and 23,000 sqm in CTPark Katowice.

While average construction costs in 2022 were around €550 per sqm, in 2023 and Q1-2024 they came to €500 per sqm. CTP expects them to stay around this level through 2024. This allows the Group to continue to deliver its industry-leading YoC above 10%, which is also supported by CTP’s unique park model and in-house construction and procurement expertise.

As at 31 March 2024, the Group had 2.0 million sqm of buildings under construction with a potential rental income of €146 million and an expected YoC of 10.3%. CTP has a long track record of delivering sustainable growth through its tenant-led development in its existing parks. 77% of the Group’s projects under construction are in existing parks, while 15% are in new parks which have the potential to be developed to more than 100,000 sqm of GLA. Planned 2024 deliveries are 43% pre-let and CTP expects to reach 80%-90% pre-letting at delivery, in line with historical performance. As CTP acts in most markets as general contractor, it is fully in control of the process and timing of deliveries, allowing the Company to speed-up or slow-down depending on tenant demand, while also offering tenants flexibility in terms of building requirements.

In 2024 the Group is targeting to deliver between 1 – 1.5 million sqm, depending on tenant demand. The 57,000 sqm of leases that are currently signed for future projects, construction of which haven’t started yet, are a further illustration of continued occupier demand.

CTP’s landbank amounted to 23.1 million sqm as at 31 March 2024 (31 December 2023: 23.4 million sqm), which allows the Company to reach its target of 20 million sqm GLA by the end of the decade. The Group is focusing on mobilizing the existing landbank to maximize returns, while maintaining disciplined capital allocation in landbank replenishment. 58% of the landbank is located within CTP’s existing parks, while 33% is in or is adjacent to new parks which have the potential to grow to more than 100,000 sqm. 24% of the landbank was secured by options, while the remaining 76% was owned and accordingly reflected in the balance sheet.

Monetization of the energy business

CTP is on track with its expansion plan for the roll-out of photovoltaic systems. With an average cost of ~€750,000 per MWp, the Group targets a YoC of 15% for these investments.

During Q1-2024, the Group installed an additional 8 MWp on the roof, which are currently being connected to the grid. The total installed capacity now stands at 108 MWp.

CTP’s sustainability ambition goes hand in hand with more and more tenants requesting photovoltaic systems, as they provide them with i) improved energy security, ii) a lower cost of occupancy, iii) compliance with increased regulation iv) compliance with their clients requirements and v) the ability to fulfil their own ESG ambitions.

Pipeline drives valuation results

Investment Property (“IP”) valuation increased from €12.0 billion as at 31 December 2023 to €12.2 billion as at 31 March 2024, driven mainly by the transfer of completed projects from Investment Property under Development (“IPuD”) to IP.

IPuD increased by 12.1% to €1.5 billion as at 31 March 2024, driven by progress on developments with most of the projects as usual to be delivered in the second half of the year.

GAV increased to €14.0 billion as at 31 March 2024, up 2.8% compared to 31 December 2023.

The revaluation in Q1-2024 came to €166.7 million, driven by a revaluation of IPuD projects, slightly below the €208.3 million of Q1-2023.

The Group’s portfolio has conservative valuation yields, with a reversionary yield that increased 80bps between 30 June 2022 and 31 December 2023, bringing it to 7.2%. With the larger yield movements in Western European markets, the yield differential between CEE and Western European logistics is back to the long-term average. CTP expects the yield differential to decrease further, driven by the higher growth expectations for the CEE region.

CTP expects further positive ERV growth on the back of continued tenant demand, which is positively impacted by the secular growth drivers in the CEE region. CEE rental levels remain affordable; despite the strong growth seen, they have started from significantly lower absolute levels than in Western European countries. In real terms, rents in many CEE markets are still below 2010 levels.

EPRA NTA per share increased from €15.92 as at 31 December 2023 to €16.50 as at 31 March 2024, representing an increase of 3.7%. The increase is mainly driven by the revaluation (+€0.37), Company specific adjusted EPRA EPS (+€0.20) and others (+€0.01).

Robust balance sheet and strong liquidity position

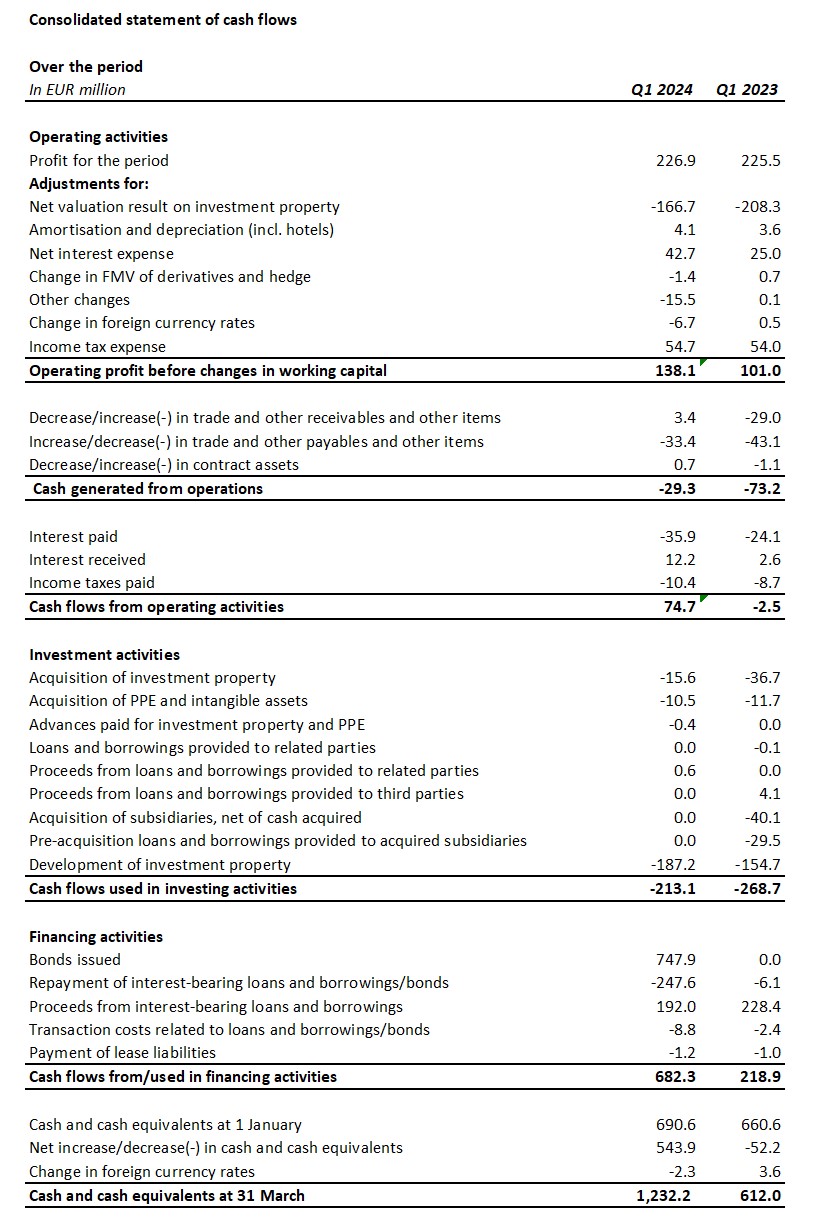

In line with its proactive and prudent approach, the Group benefits from a solid liquidity position to fund its growth ambitions, with a fixed cost of debt and conservative repayment profile.

During Q1-2024, the Group raised €940 million:

- A €100 million six-year secured loan facility with a syndicate of an Italian and Czech bank at a fixed all-in cost of 4.9%;

- A €750 million six-year green bond at MS +220bps at a coupon of 4.75%; and

- A €90 million seven-year secured loan facility with an Austrian bank at a fixed all-in cost of 4.9%.

In May, the Group also signed €168 million seven-year secured loan facility with a syndicate of Slovakian and Austrian banks.

Together with the bond issuance, CTP also completed a concurrent €250 million tender offer for short-dated maturities, proactively managing and extending its maturity profile.

As pricing in the bond market rationalized, the conditions are now competitive with the pricing in the bank lending market.

The Group’s liquidity position pro-forma for the facility signed in May stood at €2.0 billion, comprised of €1.4 billion of pro-forma cash and cash equivalents, and an undrawn RCF of €550 million.

CTP’s average cost of debt stood at 2.13% (31 December 2023: 1.95%), with 99.6% of the debt fixed or hedged until maturity. The average debt maturity came to 5.2 years (31 December 2023: 5.3 years).

The Group’s first material upcoming maturity is a €425 million[3] bond due in June 2025, which will be repaid from available cash reserves.

CTP’s LTV came to 45.9% as at 31 March 2024, down 10bps from 46.0% as at 31 December 2023. CTP expects the LTV to trend lower, as the revaluations of the Group’s developments are fully booked.

The LTV is slightly above the Company’s target of an LTV between 40%-45%, which the Groups deems to be an appropriate level, given its higher gross portfolio yield, which stands at 6.7%. The higher yielding assets lead to a healthy level of cash flow leverage that is also reflected in the normalized Net Debt to EBITDA of 9.1x (31 December 2023: 9.2x), which the Group targets to keep below 10x.

The Group had 62% unsecured debt and 38% secured debt as at 31 March 2024, with ample headroom under its Secured Debt Test and Unencumbered Asset Test covenants.

| 31 March 2024 | Covenant | |

| Secured Debt Test | 18.7% | 40% |

| Unencumbered Asset Test | 180.7% | 125% |

| Interest Cover Ratio | 3.4x | 1.5x |

In Q3-2023, Moody’s and S&P confirmed CTP’s Baa3 and BBB- credit rating, respectively, both with a stable outlook.

Guidance confirmed

Leasing dynamics remain strong, with robust occupier demand, and decreasing new supply leading to continued rental growth.

CTP is well positioned to benefit from these trends. The Group’s pipeline is highly profitable and tenant led. The YoC for CTP’s pipeline increased to 10.3%, while the target for new projects across the core CEE markets is 11%, thanks to decreasing construction costs and rental growth. The next stage of growth is built in and financed, with 2.0 million sqm under construction as at 31 March 2024 and the target to deliver between 1 – 1.5 million sqm in 2024.

CTP’s robust capital structure, disciplined financial policy, strong credit market access, industry-leading landbank, in-house construction expertise and deep tenant relations allow CTP to deliver on its targets. CTP expects to reach €1.0 billion rental income in 2027, driven by development completions, indexation and reversion, and is on track to reach 20 million sqm of GLA and €1.2 billion rental income before the end of the decade.

The Group confirms its €0.80 – €0.82 Company specific adjusted EPRA EPS guidance for 2024.

CTP’s dividend policy is to pay-out 70% – 80% of the Company specific adjusted EPRA EPS. The default dividend is scrip, but shareholders can opt for payment of the dividend in cash.

WEBCAST AND CONFERENCE CALL FOR ANALYSTS AND INVESTORS

Today at 9am (GMT) and 10am (CET), the Company will host a video presentation and Q&A session for analysts and investors, via a live webcast and audio conference call.

To view the live webcast, please register ahead at:

https://www.investis-live.com/ctp/661965f072fa7d130062b65a/nwok

To join the presentation by telephone, please dial one of the following numbers and enter the participant access code 235265.

Germany +49 32 22109 8334

France +33 9 70 73 39 58

The Netherlands +31 85 888 7233

United Kingdom +44 20 3936 2999

United States +1 646 787 9445

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance.

A recording will be available on CTP’s website within 24 hours after the presentation: https://www.ctp.eu/investors/financial-reports/

CTP FINANCIAL CALENDAR

| Action | Date |

| Payment date – 2023 final dividend | 20 May 2024 |

| H1-2024 results | 8 August 2024 |

| Capital Markets Day (Bucharest, Romania) | 25/26 September 2024 |

| Q3-2024 results | 6 November 2024 |

| FY-2024 results | 27 February 2025 |

CONTACT DETAILS FOR ANALYST AND INVESTOR ENQUIRIES:

Maarten Otte, Head of Investor Relations

Mobile: +420 730 197 500

Email: [email protected]

CONTACT DETAILS FOR MEDIA ENQUIRIES:

Patryk Statkiewicz, Group Head of Marketing & PR

Mobile: +31 (0) 629 596 119

Email: [email protected]

About CTP

CTP is Europe’s largest listed owner, developer, and manager of logistics and industrial real estate by gross lettable area, owning 12.0 million sqm of GLA across 10 countries as at 31 March 2024. CTP certifies all new buildings to BREEAM Very good or better and earned a low-risk ESG rating by Sustainalytics, underlining its commitment to being a sustainable business. For more information, visit CTP’s corporate website: www.ctp.eu

Disclaimer

This announcement contains certain forward-looking statements with respect to the financial condition, results of operations and business of CTP. These forward-looking statements may be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “plans”, “projects”, “anticipates”, “expects”, “intends”, “targets”, “may”, “aims”, “likely”, “would”, “could”, “can have”, “will” or “should” or, in each case, their negative or other variations or comparable terminology. Forward-looking statements may and often do differ materially from actual results. As a result, undue influence should not be placed on any forward-looking statement. This press release contains inside information as defined in article 7(1) of Regulation (EU) 596/2014 of 16 April 2014 (the Market Abuse Regulation).

[1] With a mix of local and EU-27 / Eurozone CPI, only limited number of caps.

[2] As at 31 December 2023

[3] Outstanding amount after the settlement of the tender offer on 7 February 2024.

Sign up to our newsletter

Get the latest insights from the industrial real estate market leader delivered into your inbox.