Резултати CTP NV за прву половину 2025. године

СНАЖНА АКТИВНОСТ ИЗНАЈМЉИВАЊА У ПРВОЈ ПОЛОВИНИ 2025. ГОДИНЕ СА ВИШЕ ОД 111 ТП5Т КВАДРАТНИХ МЕТАРA ПОТПИСАНИХ УГОВОРА О ЗАКУПУ, РАСТОМ ЗАКУПНИНЕ ОД 4,91 ТП5Т У СРЕДЊЕМ ПОДХОДУ И ПОРАСТОМ ЕПРА НТА ПО АКЦИЈИ ЗА 13,51 ТП5Т У ОДНОСУ НА ИСТУ ГОДИШЊУ ГОДИНУ НА 19,36 ЕВРА

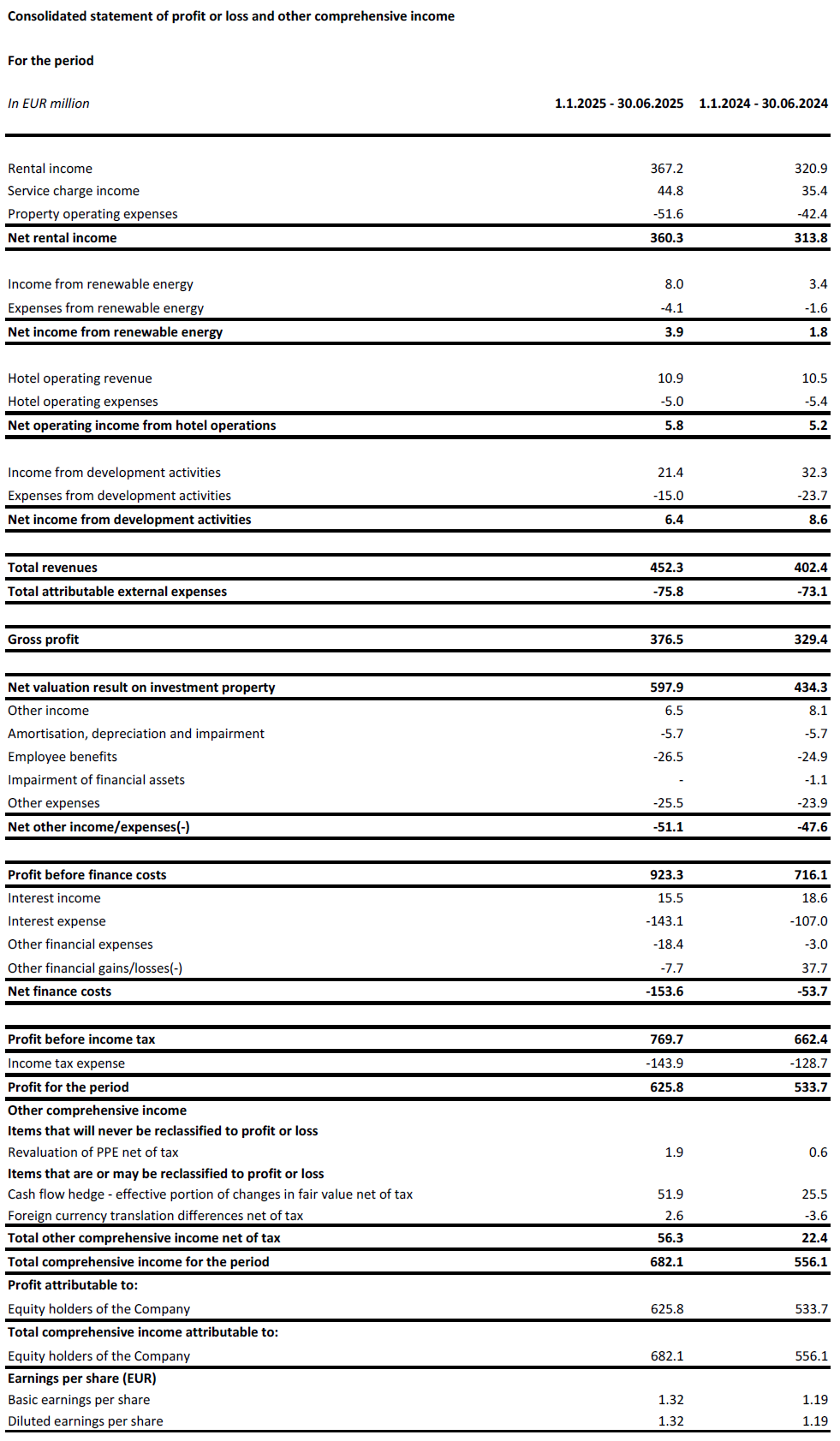

АМСТЕРДАМ, 7. август 2025. – CTP NV (CTPNV.AS), („CTP“, „Група“ или „Компанија“) забележила је у првој половини 2025. године бруто приход од закупнине од 367,2 милиона евра, што је повећање од 14,41 билиона пензија за пет хиљада евра у односу на исти период прошле године, и раст закупнине од 4,91 билиона пензија за пет хиљада евра у односу на исти период прошле године, углавном захваљујући индексацији и поновном преговарању и истеку закупа. Закуп је остао јак у првој половини године, са 111 билиона пензија за закуп више потписаних уговора о закупу у односу на исти период прошле године. Просечна месечна закупнина по новопотписаним закупима повећана је за 51 билион пензија за пет хиљада евра у односу на исти период прошле године.[1].

Закључно са 30. јуном 2025. године, годишњи приход од закупнине повећан је на 757 милиона евра, док је попуњеност остала на 93%, а стопа наплате закупнине била је 99,7%.

У првој половини године, CTP је испоручио 224.000 квадратних метара уз принос у односу на трошкове („YoC“) од 10,3%, са 100% изнајмљеним по завршетку, чиме је постојећи портфолио Групе достигао 13,5 милиона квадратних метара GLA. Ревалорација у поређењу са сличним некретнинама износила је 4,0%, вођена растом ERV-а од 2,5%, са просечном компресијом реверзијског приноса од 11 базних поена, док је бруто вредност имовине („GAV“) порасла за 7,2% на 17,1 милијарду евра, односно 15,9% у односу на исти период прошле године. Нето трошкови по акцији по EPRA-и повећани су за 7,1% у првој половини године на 19,36 евра, односно 13,5% у односу на исти период прошле године, чему је допринео и напредак у развоју.

Прилагођена зарада по основу ЕПРА, специфична за компанију, повећана је за 12,21 ТП5Т у односу на исти период прошле године и достигла је 199,3 милиона евра. Прилагођена зарада по ЕПРА, специфична за компанију, компаније ЦТП, износила је 0,42 евра, што је повећање од 6,21 ТП5Т. На међугодишње повећање прилагођене зараде по ЕПРА, специфичне за компанију, негативно је утицао повећани број акција услед повећања капитала у другој половини 2024. године. Захваљујући нашим одложеним испорукама и нето приходима од развоја у другу половину године, Група је на добром путу да достигне смернице од 0,86 до 0,88 евра за 2025. годину, што представља раст од 8 до 101 ТП5Т у поређењу са 2024. годином.

На дан 30. јуна 2025. године, пројекти у изградњи износили су укупно 2,0 милиона квадратних метара са очекиваним годишњим приходом од 10,3% и потенцијалним приходом од закупнине од 160 милиона евра када се у потпуности издају у закуп.

Површина земљишног фонда Групе износила је 26,1 милион квадратних метара, од чега је 22,2 милиона квадратних метара у власништву и билансу стања. Овај земљишни фонд обезбеђује значајан потенцијал за будући раст за CTP, са 90% лоцираним око постојећих пословних паркова (58% у постојећим парковима, 31% у новим парковима са потенцијалом од преко 100.000 GLA). У комбинацији са својим водећим годишњим износом потрошачког капитала (YoC), CTP очекује да ће наставити да генерише двоцифрени раст нето вредних аквизиција (NTA) у наредним годинама.

Посебно имамо користи од тренда „ниршоринга“, што показује наш раст са азијским закупцима производње, који су чинили око 20% наше укупне активности закупа у последњих 18 месеци, у поређењу са преко 10% удела у нашем укупном портфолију.

Годишњи приход од закупнине повећан је на 757 милиона евра. Наша следећа фаза раста је већ закључана кроз наших 2,0 милиона квадратних метара продајне површине у изградњи и земљишни фонд од 26,1 милиона квадратних метара, што значи да можемо да наставимо да генеришемо двоцифрени раст некретнина у непокретностима (NTA) у наредним годинама. Уверени смо да можемо остварити наше амбициозне циљеве и достићи милијарду годишњих прихода од закупнине у 2027. години.

Кеи Хигхлигхтс

| У милионима евра | Прва половина 2025. | Х1-2024 | 1ТП3Т промена |

| Бруто приход од најма | 367.2 | 320.9 | +14.4% |

| Нето приход од најма | 360.3 | 313.8 | +14.8% |

| Нето резултат процене инвестиционих некретнина | 597.9 | 434.3 | +37.7% |

| Добит за период | 625.8 | 533.7 | +17.2% |

| Прилагођена ЕПРА зарада за одређену компанију | 199.3 | 177.6 | +12.2% |

| У € | Прва половина 2025. | Х1-2024 | 1ТП3Т промена |

| ЕПРА ЕПС прилагођен специфичној компанији | 0.42 | 0.40 | +6.2% |

| У милионима евра | 30. јун 2025. | 31. децембар 2024 | 1ТП3Т промена |

| Инвестициона некретнина („ИП“) | 15,463.5 | 14,655.3 | +5.5% |

| Инвестициона некретнина у развоју („ИПуД“) | 1,416.4 | 1,076.8 | +31.5% |

| 30. јун 2025. | 31. децембар 2024 | 1ТП3Т промена | |

| ЕПРА НТА по акцији | €19.36 | €18.08 | +7.1% |

| Очекивани годишњи рок за пројекте у изградњи | 10.3% | 10.3% | |

| ЛТВ | 44.9% | 45.3% |

Континуирана снажна потражња закупаца подстиче раст закупнина

У првој половини 2025. године, CTP је потписао уговоре о закупу за 1.015.000 квадратних метара, што је повећање од 11% у поређењу са истим периодом 2024. године, са просечном месечном закупнином по квадратном метру од 5,98 евра (прва половина 2024: 5,59 евра). Прилагођавајући се разликама међу земљама, закупнине су у просеку порасле за 5%.

| Закупни уговори потписани по кв | К1 | К2 | ИТД | К3 | К4 | ФИ |

| 2023 | 297,000 | 552,000 | 849,000 | 585,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 919,000 | 577,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 1,015,000 | |||

| Годишњи раст | +24% | +3% | +11% |

| Просечан месечни закуп потписан по квадратном метру (€) | К1 | К2 | ИТД | К3 | К4 | ФИ |

| 2023 | 5.31 | 5.56 | 5.47 | 5.77 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.59 | 5.69 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.98 |

Отприлике две трећине уговора о закупу потписано је са постојећим закупцима, у складу са пословним моделом ЦТП-а да расте са постојећим закупцима у постојећим парковима.

Генерисање готовинског тока кроз стални портфолио и аквизиције

Просечан тржишни удео CTP-а у Чешкој Републици, Румунији, Мађарској и Словачкој износио је 28,2% на дан 30. јуна 2025. године и остаје највећи власник и инвеститор индустријских и логистичких некретнина на тим тржиштима. Група је такође лидер на тржишту у Србији и Бугарској.

Са више од 1.500 клијената, CTP има широку и диверзификовану међународну базу закупаца, коју чине водеће компаније са јаким кредитним рејтингом. Закупци CTP-а представљају широк спектар индустрија, укључујући производњу, високу технологију/ИТ, аутомобилску индустрију, електронску трговину, малопродају, велепродају и 3PL компаније. База закупаца је веома диверзификована, при чему ниједан закупац не отпада више од 2,5% годишњег прихода од закупнине компаније, што доводи до стабилног тока прихода. 50 највећих закупаца CTP-а отпада само 36,0% његовог прихода од закупнине, а велика већина клијената изнајмљује простор у више CTP паркова.

Попуњеност смештајних јединица Компаније достигла је 93% (фискална 2024: 93%). Стопа задржавања клијената Групе остаје снажна на 85% (фискална 2024: 87%) и показује способност CTP-а да искористи дугорочне односе са клијентима. Просечан животни век портфолија (WAULT) износио је 6,2 године (фискална 2024: 6,4 године), што је у складу са циљем Компаније од >6 година.

Ниво наплате закупнине износио је 99,7% у првој половини 2025. године (фискална 2024. година: 99,8%), без погоршања профила плаћања закупаца.

Приход од закупнине у првој половини 2025. године износио је 367,2 милиона евра, што је повећање од 14,41 билиона терета (TP5T) у односу на исти период прошле године на апсолутном нивоу, углавном захваљујући испорукама и расту у поређењу са уговорима о закупнини. На упоредном нивоу, приход од закупнине порастао је за 4,91 билиона терета (TP5T), захваљујући индексацији и реверзији поновних преговора и истеку закупа.

Група је предузела мере за ограничавање цурења накнада за услуге, што је резултирало побољшањем односа нето прихода од закупнине и прихода од закупнине са 97,8% у првој половини 2024. на 98,1% у првој половини 2025. године. Сходно томе, нето приход од закупнине је порастао за 14,8% у односу на исти период прошле године.

Све већи део прихода од закупнине који генерише инвестициони портфолио CTP-а има користи од заштите од инфлације. Од краја 2019. године, сви нови уговори о закупу Групе укључују клаузулу о индексирању повезану са индексом потрошачких цена, која израчунава годишње повећање закупнине као већи износ од:

- фиксно повећање од 1,51ТП3Т–2,51ТП3Т годишње; или

- индекс потрошачких цена[2].

На дан 30. јуна 2025. године, 72% прихода генерисаног портфолијом Групе укључује ову клаузулу о двострукој индексацији, а Група очекује да ће се то даље повећати.

Потенцијал поврата је достигао 14,9%. Нови уговори о закупу су континуирано потписивани изнад процењене вредности закупнине. („ERV“), што илуструје континуирани снажан раст тржишних цена закупнине и подржава процене вредности.

Годишњи приход од закупнине износио је 757 милиона евра на дан 30. јуна 2025. године, што је повећање од 11,51 трилијане рупија (TP5T) у односу на исти период прошле године, што показује снажан раст новчаног тока инвестиционог портфолија CTP-а.

H1 развој испоручен са 10.3% YoC и 100% изнајмљивањем при испоруци

ЦТП је наставио са својим дисциплинованим улагањем у свој високо профитабилан цевовод.

У првој половини 2025. године, Група је завршила изградњу 224.000 квадратних метара продајне површине (прва половина 2024. године: 328.000 квадратних метара). Објекти су завршени по стопи коришћења (YO) од 10,3%, изнајмљивања 100% и генерисаће уговорени годишњи приход од закупнине од 12,1 милион евра. Као и обично, испоруке у 2025. години су померене за четврти квартал.

Док су просечни трошкови изградње у 2022. години износили око 550 евра по квадратном метру, у 2023. и 2024. години достигли су 500 евра по квадратном метру и остали су стабилни у првој половини 2025. године. Ово омогућава Групи да настави да испоручује свој водећи у индустрији стопу производње изнад 10%, што је такође подржано јединственим моделом парка компаније CTP и интерном стручношћу у изградњи и набавци.

На дан 30. јуна 2025. године, Група је имала 2,0 милиона квадратних метара зграда у изградњи са потенцијалним приходом од закупнине од 160 милиона евра и очекиваним приходом од 10,3%. CTP има дугогодишње искуство у остваривању одрживог раста кроз развој вођен закупцима у својим постојећим парковима. 79% пројеката Групе у изградњи налази се у постојећим парковима, док се 9% налази у новим парковима који имају потенцијал да се развију на више од 100.000 квадратних метара површине за куповину. Планиране испоруке за 2025. годину су 53% у претходном закупу, у односу на 35% у фискалној 2024. години. Претходни закуп у постојећим парковима износио је 47%, док је претходни закуп нових паркова био на 80%, што показује низак ризик који је уграђен у процес изградње. CTP очекује да ће достићи 80%-90% у претходном закупу приликом испоруке, у складу са историјским резултатима. Пошто CTP делује као генерални извођач радова на већини тржишта, он у потпуности контролише процес и време испоруке, што омогућава компанији да убрза или успори у зависности од потражње закупца, а истовремено нуди закупцима флексибилност у погледу њихових грађевинских захтева.

Група очекује да ће 2025. године испоручити између 1,2 и 1,7 милиона квадратних метара, у зависности од потражње закупаца. 106.000 квадратних метара закупних уговора који су већ потписани за будуће пројекте — чија изградња још није почела — додатно илуструју континуирану потражњу закупаца.

Површина земљишног фонда CTP-а износила је 26,1 милион квадратних метара на дан 30. јуна 2025. године (31. децембра 2024: 26,4 милиона квадратних метара), што омогућава Компанији да достигне свој циљ од 20 милиона квадратних метара продајне површине до краја деценије. Група се фокусира на мобилизацију постојећег земљишног фонда, уз одржавање дисциплиноване расподеле капитала у обнављању земљишног фонда. 58% земљишног фонда налази се у постојећим парковима CTP-а, док се 31% налази у, или је поред, нових паркова који имају потенцијал да нарасту на више од 100.000 квадратних метара. 15% земљишног фонда је обезбеђено опцијама, док је преосталих 85% било у власништву и сходно томе је одражено у билансу стања.

Под претпоставком односа изграђености од 2 квадратна метра земљишта према 1 квадратном метру купопродајне површине (GLA), CTP може да изгради преко 13 милиона квадратних метара купопродајне површине (GLA) на свом обезбеђеном земљишту. Земљиште CTP-а се у билансу стања држи по цени од око 60 евра по квадратном метру, а трошкови изградње у просеку износе приближно 500 евра по квадратном метру, што укупне инвестиционе трошкове доводи до приближно 620 евра по квадратном метру. Тренутни портфолио Групе процењује се на око 1.040 евра по квадратном метру, што резултира потенцијалом ревалоризације од око 400 евра по изграђеном квадратном метру.

Монетизација енергетског пословања

ЦТП наставља са својим планом проширења за увођење фотонапонских система. Са просечном ценом од ~€750,000 по МВп, Група циља ИоЦ од 151ТП3Т за ове инвестиције.

CTP има инсталирани фотонапонски капацитет од 138 MWp, од чега је 108 MWp у потпуности оперативно.

У првој половини 2025. године приходи од обновљивих извора енергије износили су 8,0 милиона евра, што је повећање од 1361 трилијане пензије и 5 хиљада динара у односу на исти период прошле године, углавном захваљујући повећању инсталираних капацитета током 2024. године.

ЦТП-ова амбиција одрживости иде руку под руку са све више и више закупаца који траже фотонапонске системе, јер им они пружају и) побољшану енергетску сигурност, ии) ниже трошкове становања, иии) усклађеност са повећаном регулативом и/или захтјевима њихових клијената и ив) способност да испуне сопствене ЕСГ амбиције.

Резултати процене вођени цевоводом и позитивном ревалоризацијом сталног портфеља

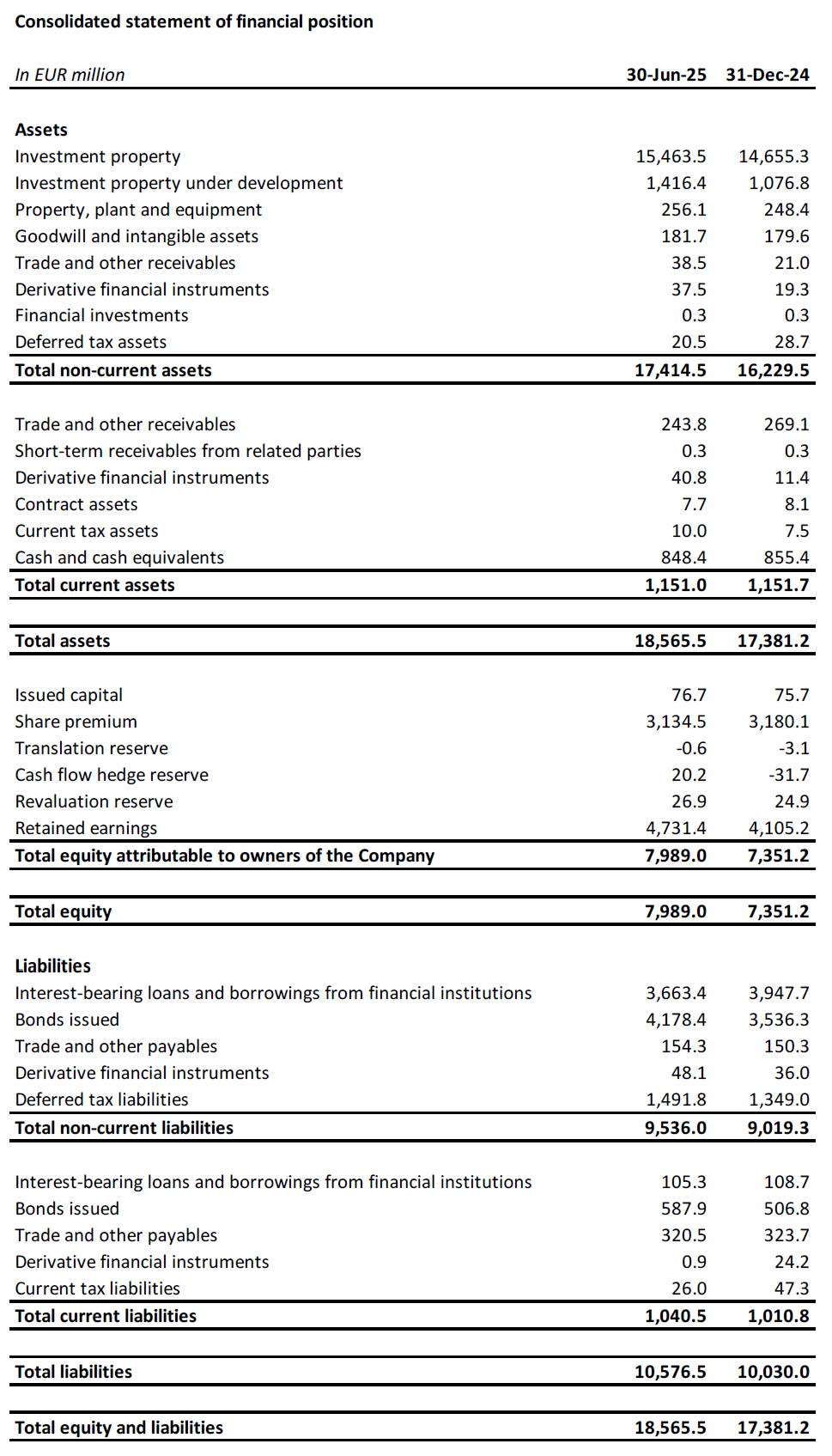

Процена вредности инвестиционих некретнина („ИП“) повећана је са 14,7 милијарди евра на дан 31. децембра 2024. на 15,5 милијарди евра на дан 30. јуна 2025. године, што је резултат преноса завршених пројеката са инвестиционих некретнина у развоју („ИПуД“) на ИП и позитивне ревалоризације постојећег портфолија.

IPuD је повећан за 31,5% од 31. децембра 2024. на 1,4 милијарде евра на дан 30. јуна 2025. године, вођен утрошеним CAPEX-ом, ревалоризацијом због повећања претходног издавања у закуп и напретка изградње, као и почетком нових грађевинских пројеката у првој половини 2025. године.

БДВ је порасла на 17,1 милијарду евра на дан 30. јуна 2025. године, што је повећање од 7,2% у поређењу са 31. децембром 2024. године.

Ревалоризација у првој половини 2025. године износила је 597,9 милиона евра, што је резултат позитивне ревалоризације пројеката IPuD (+181,3 милиона евра), земљишне банке (+43,1 милион евра) и постојеће имовине (+373,6 милиона евра).

На упоредној основи, портфолио CTP-а је забележио повећање вредности од 4,0% током прве половине 2025. године, вођено растом ERV-а од 2,5%.

CTP очекује даљи позитиван раст ERV-а захваљујући континуираној потражњи закупаца, на коју позитивно утичу дугорочни покретачи раста у региону централне и источне Европе. Нивои закупнина у централној и источној Европи остају приступачни; упркос снажном расту који се види, с обзиром на то да су кренули са знатно нижих апсолутних нивоа него у земљама западне Европе. У реалном смислу, закупнине на многим тржиштима централне и источне Европе су и даље испод нивоа из 2010. године.

Портфолио Групе има конзервативне приносе од 7,0%. CTP је забележио даљу компресију приноса током прве половине 2025. године од 11 базних поена у просеку у целом портфолију и очекује даљу компресију приноса током друге половине 2025. године. Очекује се да ће се разлика у приносима између логистике у Централној и Источној Европи (ЦИЕ) и Западној Европи смањивати током времена, вођена већим очекивањима раста за регион ЦИЕ и растућом активношћу на инвестиционим тржиштима.

Нето добит по акцији по основу ЕПРА-е повећана је са 18,08 евра на дан 31. децембра 2024. на 19,36 евра на дан 30. јуна 2025. године, што представља међугодишње повећање од 13,51 ТП5Т и повећање од 7,11 ТП5Т у првој половини 2025. године. Повећање је углавном резултат ревалоризације (+1,25 евра), прилагођене зараде по акцији по основу ЕПРА-е специфичне за компанију (+0,42 евра) и компензоване је коначном дивидендом за 2024. годину исплаћеном у мају (-0,30 евра) и другим ставкама (-0,09 евра).

Робустан биланс стања и јака позиција ликвидности

У складу са својим проактивним и опрезним приступом, Група има користи од солидне позиције ликвидности за финансирање својих амбиција раста, са фиксним трошковима дуга и конзервативним профилом отплате.

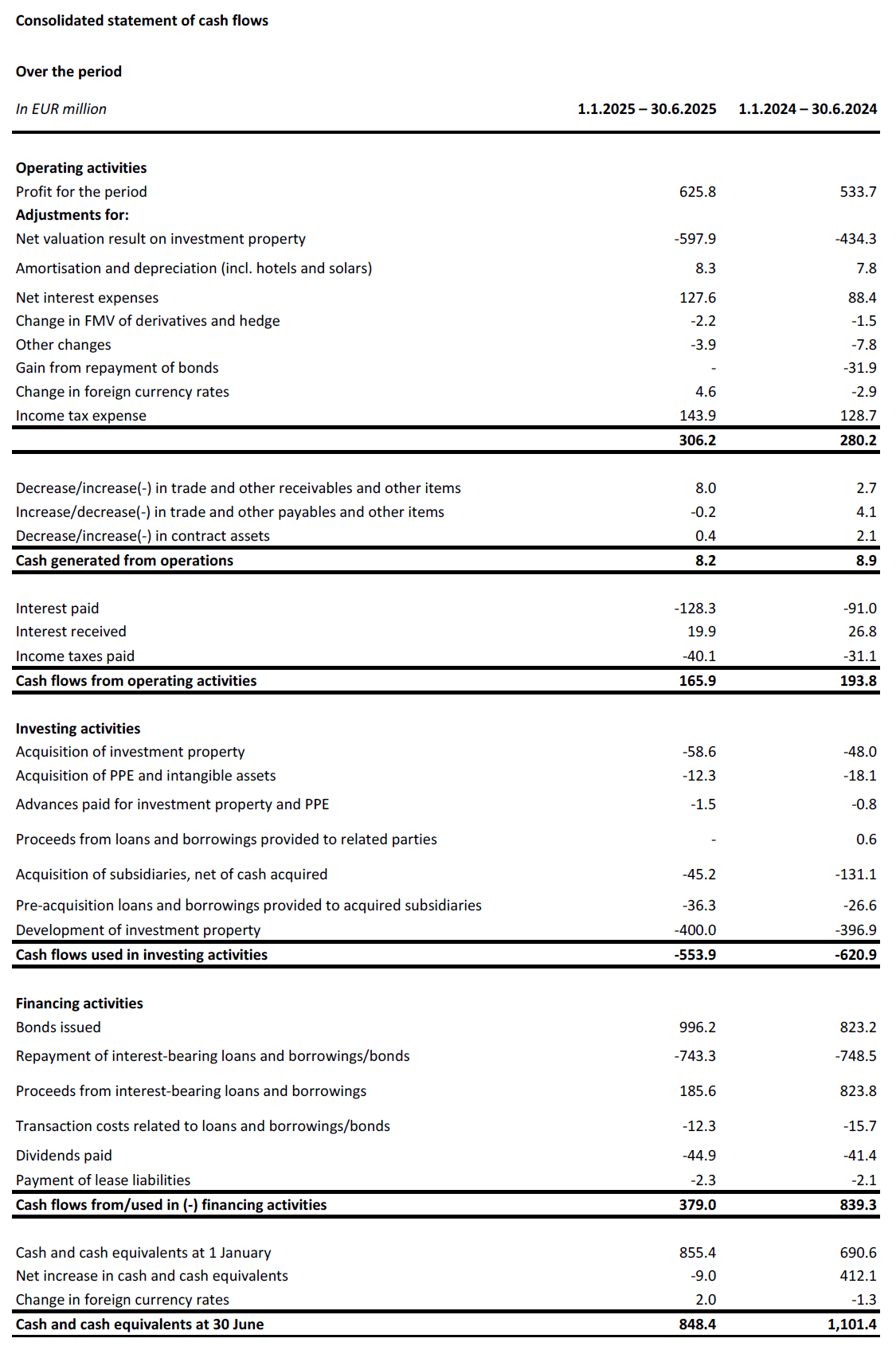

Током прве половине 2025. године, Група је обезбедила 1,7 милијарди евра за финансирање свог органског раста:

- Зелена обвезница од 1,0 милијарду евра са две транше, са шестогодишњом траншом од 500 милиона евра са каматном стопом MS +145 базних поена и купоном од 3,625% и десетогодишњом траншом од 500 милиона евра са каматном стопом MS +188 базних поена и купоном од 4,25%;

- Петогодишњи необезбеђени кредитни аранжман од 30 милијарди јена (еквивалентно 185 милиона евра) са синдикaтом азијских банака по каматној стопи од TONAR +130 базних поена и фиксним укупним трошковима од 4,1%; и

- Петогодишњи необезбеђени кредитни аранжман повезан са одрживошћу у вредности од 500 милиона евра са синдикатом 13 европских и азијских банака по фиксној укупној цени од 3,7%, неповучен на дан 30. јуна 2025. године.

CTP је наставио активно да управља својим портфолијом банкарских кредита у првој половини 2025. године. Преговарано је смањење марже на додатних 159 милиона евра обезбеђених банкарских кредита, а 441 милион евра необезбеђеног рочног кредита потписаног 2023. године је превремено отплаћено и биће рефинансирано новим необезбеђеним кредитом од 500 милиона евра. Оба су омогућила CTP-у да оствари значајне уштеде на каматним стопама и смањи укупне трошкове дуга у будућности.

Ликвидност Групе износила је 2,1 милијарду евра, што се састојало од 0,8 милијарди евра готовине и готовинских еквивалената и неискоришћеног револуционарног кредита од 1,3 милијарде евра.

Просечна цена дуга за CTP износила је 3,2% (фискална 2024: 3,1%), што је незнатно више у односу на крај 2024. године, због новог финансирања. 99,9% дуга има фиксну каматну стопу или је хеџиран до доспећа.

Група не капитализује камату на развојне пројекте, стога су сви трошкови камата укључени у биланс успеха. Просечан рок доспећа дуга износио је 5,1 годину (фискална 2024. година: 5,0 година).

Група је отплатила обвезницу од 272 милиона евра у јуну 2025. године из расположивих новчаних резерви. Следећи рок доспећа је обвезница од 185 милиона евра која доспева у октобру 2025. године, а која ће такође бити отплаћена из расположивих новчаних резерви.

LTV компаније CTP је смањен на 44,9% на дан 30. јуна 2025. године, углавном због позитивне ревалоризације постојећег портфолија и инвестиционих некретнина у развоју.

Имовина Групе са вишим приносом, захваљујући бруто приносу портфолија од 6,6%, доводи до здравог нивоа левериџа новчаног тока који се такође огледа у нормализованом односу нето дуга и EBITDA од 9,2x (фискална 2024. година: 9,1x), који Група циља да одржи испод 10x.

Група је имала 66% необезбеђеног дуга и 34% обезбеђеног дуга на дан 30. јуна 2025. године, са довољним простором за покривање услова у складу са својим условима за тест обезбеђеног дуга и тест неоптерећене имовине.

Како су цене на тржишту обвезница рационализоване, услови су сада конкурентнији од цена на тржишту банкарских кредита, што ће омогућити Групи да више балансира у правцу необезбеђеног кредитирања.

| 30. јун 2025. | Завет | |

| Тест обезбеђеног дуга | 15.7% | 40% |

| Тест неоптерећене имовине | 194.9% | 125% |

| Однос покрића камата | 2,4 пута | 1,5к |

У трећем кварталу 2024. године, S&P је потврдио кредитни рејтинг CTP-а BBB- са стабилним изгледима. У јануару 2025. године, јапанска агенција за рејтинг JCR је доделила CTP-у кредитни рејтинг A- са стабилним изгледима. У другом кварталу 2025. године, Moody's је побољшао изгледе са стабилних на позитивне за кредитни рејтинг Baa3.

Гуиданце

Динамика закупа остаје снажна, са снажном потражњом закупаца и смањењем понуде нових простора, што доводи до континуираног раста закупнина. CTP је у доброј позицији да искористи ове трендове. Групин програм је веома профитабилан и вођен закупцима. Стопа производа за тренутни програм CTP-а остала је на водећих 10,3% у индустрији. Следећа фаза раста је изграђена и финансирана, са 2,0 милиона квадратних метара у изградњи закључно са 30. јуном 2025. године, са циљем да се испоручи између 1,2 и 1,7 милиона квадратних метара у 2025. години.

Робусна капитална структура CTP-а, дисциплинована финансијска политика, снажан приступ тржишту кредита, водећа банка земљишта у индустрији, сопствена стручност у грађевинарству и дубоки односи са закупцима омогућавају CTP-у да оствари своје циљеве. CTP очекује да ће достићи 1,0 милијарду евра прихода од закупнине у 2027. години, вођеног завршетком развојних пројеката, индексацијом и реверзијом, и на добром је путу да достигне 20 милиона квадратних метара GLA и 1,2 милијарде евра прихода од закупнине пре краја деценије.

Група је поставила смерницу од 0,86 до 0,88 евра за прилагођену зараду по акцији (EPRA) специфичну за компанију за 2025. годину. Ово је вођено нашим снажним основним растом, са растом од око 4% у поређењу са сличним пореским ценама, делимично надокнађеним вишим просечним трошковима дуга због (ре)финансирања у 2024. и 2025. години.

Дивиденда

CTP објављује привремену дивиденду од 0,31 евра по обичној акцији, што је повећање од 6,9% у поређењу са привременом дивидендом за 2024. годину, и што представља исплату од 74% специфичне за Компанију прилагођене EPRA зараде по акцији, у складу са односом исплате дивиденде Групе од 70% до 80%. Подразумевана дивиденда је у облику акције, али акционари се могу одлучити за исплату дивиденде у готовини.

ВЕБЦАСТ И КОНФЕРЕНЦИЈСКИ ПОЗИВ ЗА АНАЛИТИЧАРЕ И ИНВЕСТИТОРЕ

Данас у 9:00 (ГМТ) и 10:00 (ЦЕТ), Компанија ће бити домаћин видео презентације и сесије питања и одговора за аналитичаре и инвеститоре, путем веб преноса уживо и аудио конференцијског позива.

Да бисте погледали веб пренос уживо, региструјте се унапред на:

https://www.investis-live.com/ctp/6863c5976c0d660016f95b35/kalwt

Да бисте се придружили презентацији телефоном, позовите један од следећих бројева и унесите приступни код учесника 893972.

Холандија +31 85 888 7233

Велика Британија +44 20 3936 2999

Сједињене Америчке Државе +1 646 664 1960

Притисните *1 да поставите питање, *2 да повучете своје питање или *0 за помоћ оператера.

Снимак ће бити доступан на веб страници ЦТП-а у року од 24 сата након презентације: https://ctp.eu/investors/financial-results/

ЦТП ФИНАНСИЈСКИ КАЛЕНДАР

| поступак | Датум |

| Дани тржишта капитала (Вупертал, Немачка) | 24-25. септембар 2025 |

| Резултати К3-2025 | 6. новембар 2025 |

| Резултати за фискалну 2025. годину | 26. фебруар 2026. |

КОНТАКТ ДЕТАЉИ ЗА УПИТАЊА АНАЛИТИЧАРА И ИНВЕСТИТОРА:

Мартен Оте, шеф односа са инвеститорима и тржишта капитала

Мобилни: +420 730 197 500

Емаил: [email protected]

КОНТАКТ ЗА МЕДИЈА УПИТАЊА:

Емаил: [email protected]

О ЦТП-у

CTP је највећи европски власник, инвеститор и менаџер логистичких и индустријских некретнина по бруто површини за издавање, са 13,5 милиона квадратних метара GLA у 10 земаља на дан 30. јуна 2025. CTP сертификује све нове зграде по BREEAM стандарду „Веома добро“ или „боље“ и добио је ESG оцену занемарљивог ризика од стране Sustainalytics-а, чиме истиче своју посвећеност одрживом пословању. За више информација посетите корпоративну веб страницу CTP-а: ввв.цтп.еу

Одрицање од одговорности

Ово саопштење садржи одређене изјаве о будућности у погледу финансијског стања, резултата пословања и пословања ЦТП-а. Ове изјаве о будућности могу се идентификовати употребом терминологије која се односи на будућност, укључујући изразе „верује“, „процене“, „планови“, „пројекти“, „очекује“, „намерава“, „циљеви ”, „може”, „циљ”, „вероватно”, „би”, „могао”, „може имати”, „хоће” или „треба” или, у сваком случају, њихове негативне или друге варијације или упоредиву терминологију. Изјаве које се односе на будућност могу и често се разликују материјално од стварних резултата. Као резултат тога, не би требало да се врши неприкладан утицај на било коју изјаву која се односи на будућност. Ово саопштење за јавност садржи инсајдерске информације како је дефинисано у члану 7(1) Уредбе (ЕУ) 596/2014 од 16. априла 2014. (Уредба о злоупотреби тржишта).

[1] Прилагођено за кантри микс.

[2] Са мешавином локалног и ЦПИ ЕУ-27 / еврозоне, само ограничен број ограничења.

Пријавите се на наш билтен

Примајте најновије информације од лидера на тржишту индустријских некретнина директно у пријемно сандуче.