Резултати CTP NV за трећи квартал 2025.

NET RENTAL INCOME UP 15.4% YOY, LIKE-FOR-LIKE RENTAL GROWTH OF 4.5% AND EPRA NTA PER SHARE UP 14.0% YOY TO €19.98

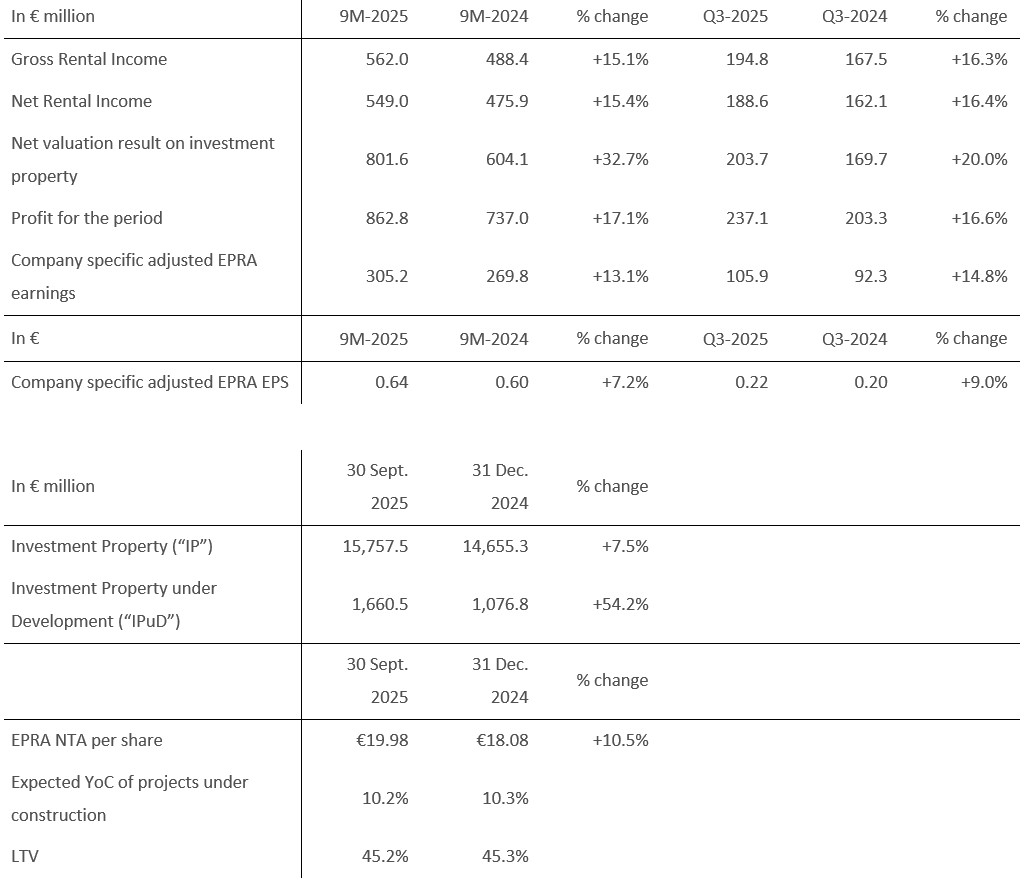

AMSTERDAM, 6 November 2025 – CTP N.V. (CTPNV.AS), (“CTP”, the “Group” or the “Company”), in the first nine months of the year increased Gross Rental Income by 15.1% y-o-y to €562 million and recorded a like-for-like y-o-y rental growth of 4.5%, mainly driven by indexation and reversion on renegotiations and expiring leases. As at 30 September 2025, the annualised rental income increased to €778 million, while occupancy remained at 93% and the rent collection rate stood at 99.8%.

Through 9M-2025, CTP delivered 553,000 sqm at a Yield on Cost (“YoC”) of 10.3%, and which were 100% let at completion, bringing the Group’s standing portfolio to 13.8 million sqm of GLA. The Gross Asset Value (“GAV”) increased by 10.6% to €17.7 billion, and 16.0% y-o-y. EPRA NTA per share increased by 10.5% in 9M-2025 to €19.98 and 14.0% y-o-y.

Company-specific adjusted EPRA earnings increased by 13.1% y-o-y to €305.2 million. CTP’s Company-specific adjusted EPRA EPS amounted to €0.64, an increase of 7.2%. With deliveries and net development income backloaded toward the second half of the year, the Group remains on track to reach its guidance of €0.86 – €0.88 for 2025, which represents 8% – 10% growth compared to 2024.

As at 30 September 2025, projects under construction totalled 2.0 million sqm with an expected YoC of 10.2%, and a potential rental income of €165 million when fully leased. A substantial portion of these projects will be delivered in 2025, and CTP continues to expect to deliver between 1.3 million sqm – 1.6 million sqm this year.

The Group’s landbank amounted 25.7 million sqm, of which 22.0 million sqm is owned and on-balance sheet. This landbank secures substantial future growth potential for CTP, with 90% located around existing business parks (57% in existing parks, 33% in new parks with a potential of over 100,000 sqm GLA). Combined with its industry-leading YoC, CTP expects to continue to generate double-digit NTA growth in the years to come.

The strength of CTP’s platform has been underlined in September by S&P’s credit rating upgrade from BBB- to BBB with a stable outlook. The upgrade follows the Q2-2025 action of Moody’s, upgrading CTP’s outlook from Stable to Positive.

We have a landbank of 25.7 million sqm with an embedded potential development profit of over €5 billion, providing significant upside for continued value creation. Our unique integrated model as an operator, developer, and a growth platform gives us the capacity and flexibility to capture opportunities, both in our existing markets and potential new markets.

Structural trends such as nearshoring are accelerating, illustrated by the continuous growth of Asian manufacturing tenants in our portfolio. In the CEE region we continue to see strong growth in domestic consumption, while in Germany we benefit from the modernisation of the economy. With our scale, portfolio quality, and development pipeline, CTP is well positioned to benefit from these trends and reach our ambition of 30 million sqm of GLA in year 2030.”

Кеи Хигхлигхтс

Континуирана снажна потражња закупаца подстиче раст закупнина

In 9M-2025, CTP signed leases for 1,577,000 sqm, an increase of 6% compared to the same period in 2024, with an average monthly rent per sqm of €5.86 (9M-2024: €5.63). Adjusting for the differences among the country mix, rents increased on average by 6%.

| Закупни уговори потписани по кв | К1 | К2 | К3 | ИТД | К4 | ФИ |

| 2023 | 297,000 | 552,000 | 585,000 | 1,435,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 577,000 | 1,495,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 562,000 | 1,577,000 |

| Просечан месечни закуп потписан по квадратном метру (€) | К1 | К2 | К3 | ИТД | К4 | ФИ |

| 2023 | 5.31 | 5.56 | 5.77 | 5.60 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.69 | 5.63 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.64 | 5.86 |

In total, 73% of leases signed were with existing tenants, in line with CTP’s business model of growing with existing tenants at existing parks.

Генерисање готовинског тока кроз стални портфолио и аквизиције

CTP’s average market share in the Czech Republic, Romania, Hungary, and Slovakia came to 28.3% as at 30 September 2025 and it remains the largest owner and developer of industrial and logistics real estate assets in those markets. The Group is also the market leader in Serbia and Bulgaria.

With more than 1,500 clients, CTP has a wide and diversified international tenant base, consisting of blue-chip companies with strong credit ratings. CTP’s tenants represent a broad range of industries, including manufacturing, high-tech/IT, automotive, e-commerce, retail, wholesale, and 3PLs. The tenant base is highly diversified, with no single tenant accounting for more than 2.5% of the Company’s annual rent roll, which leads to a stable income stream. CTP’s top 50 tenants only account for 32.7% of its rent roll and the vast majority of clients rent space at multiple CTParks.

The Company’s occupancy remains at 93% (FY-2024: 93%). The Group’s client retention rate remains strong at 82% (FY-2024: 87%) and demonstrates CTP’s ability to leverage long-standing client relationships. The portfolio WAULT stood at 6.1 years (FY-2024: 6.4 years), in line with the Company’s target of >6 years.

Rent collection level stood at 99.8% in 9M-2025 (FY-2024: 99.8%), with no deterioration in the payment profile of tenants.

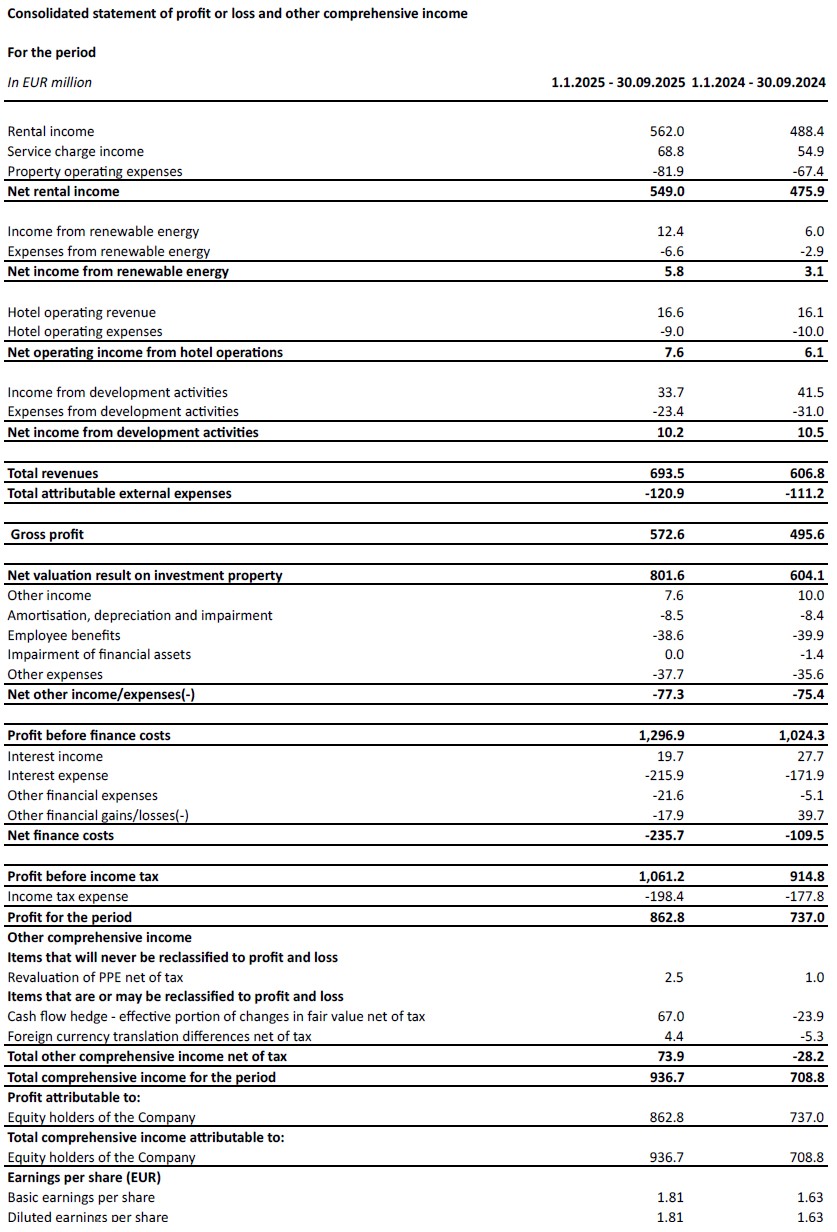

Rental income in 9M-2025 amounted to €562 million, up 15.1% y-o-y on an absolute basis, mainly driven by deliveries and like-for-like growth. On a like-for-like basis, rental income grew 4.5%, thanks to indexation and reversion on renegotiations and expiring leases.

The Group has put measures in place to limit service charge leakage, which resulted in improvement of the Net Rental Income to Rental Income ratio from 97.4% in 9M-2024 to 97.7% in 9M-2025. Consequently, the Net Rental Income increased 15.4% y-o-y.

An increasing proportion of the rental income generated by CTP’s investment portfolio benefits from inflation protection. Since end-2019, the Group’s new lease agreements include a CPI-linked indexation clause, which calculates annual rental increases as the higher of:

- фиксно повећање од 1,51ТП3Т–2,51ТП3Т годишње; или

- индекс потрошачких цена[1].

As at 30 September 2025, 72% of income generated by the Group’s portfolio includes this double indexation clause, and the Group expects this to increase further.

The reversionary potential came to 13.7%. New leases have been signed continuously above the Estimated Rental Value (“ERV”), illustrating continued strong market rental growth and supporting valuations.

The annualised rental income came to €778 million as at 30 September 2025, an increase of 10.8% y-o-y, showcasing the strong cash flow growth of CTP’s investment portfolio.

9M-2025 developments delivered with a 10.3% YoC and 100% let at delivery

ЦТП је наставио са својим дисциплинованим улагањем у свој високо профитабилан цевовод.

In 9M-2025, the Group completed 553,000 sqm of GLA (9M-2024: 545,000 sqm). The developments were delivered at a YoC of 10.3%, 100% let and will generate contracted annual rental income of €35.5 million. As usual, deliveries in 2025 are skewed to the fourth quarter.

While average construction costs in 2022 were around €550 per sqm, in 2023 and 2024 they came to €500 per sqm and remained stable in 9M-2025. This allows the Group to continue to deliver its industry-leading YoC above 10%, which is also supported by CTP’s unique park model and in-house construction and procurement expertise.

As at 30 September 2025, the Group had 2.0 million sqm of buildings under construction with a potential rental income of €165 million and an expected YoC of 10.2%. CTP has a long track record of delivering sustainable growth through its tenant-led development at its existing parks. 78% of the Group’s projects under construction are at existing parks, while 10% are in new parks which have the potential to be developed to more than 100,000 sqm of GLA. Planned 2025 deliveries are 63% pre-let, up from 35% as at FY-2024. The pre-let rate in existing parks stood at 58%, while at new parks the pre-let figure was at 76%, showcasing the low risk embedded in the pipeline. CTP expects to reach 80%-90% pre-letting at delivery, in line with historical performance. As CTP acts as general contractor in most markets, it is fully in control of the process and timing of deliveries, allowing the Company to speed-up or slow-down depending on tenant demand, while also offering tenants flexibility in terms of their building requirements.

In 2025, the Group is expecting to deliver between 1.3 million sqm – 1.6 million sqm, depending on tenant demand. The 151,000 sqm of leases that are already signed for future projects —construction of which has not started yet—are a further illustration of continued occupier demand.

CTP’s landbank amounted to 25.7 million sqm as at 30 September 2025 (31 December 2024: 26.4 million sqm), which will largely contribute to reach its ambition of 30 million sqm GLA by the year 2030. The Group is focusing on mobilising its existing landbank, while maintaining disciplined capital allocation in landbank replenishment. 57% of the landbank is located at CTP’s existing parks, while 33% is in, or is adjacent to, new parks which have the potential to grow to more than 100,000 sqm. 15% of the landbank was secured by options, while the remaining 85% was owned and accordingly reflected in the balance sheet.

Assuming a build-up ratio of 2 sqm of land to 1 sqm of GLA, CTP can build approximately 13 million sqm of GLA on its secured landbank. CTP’s land is held on balance sheet at around €60 per sqm and construction costs amount on average to approximately €500 per sqm, bringing total investment costs to approximately €620 per sqm. The Group’s standing portfolio is valued around €1,040 per sqm, resulting in a revaluation potential of around €400 per sqm built.

Монетизација енергетског пословања

ЦТП наставља са својим планом проширења за увођење фотонапонских система. Са просечном ценом од ~€750,000 по МВп, Група циља ИоЦ од 151ТП3Т за ове инвестиције.

CTP has an installed PV capacity of 149 MWp, of which 123.5 MWp is fully operational.

In 9M-2025 revenues from renewable energy came to €12.4 million, up 108% y-o-y mainly driven by the increase in capacity installed throughout 2024.

CTP’s sustainability ambitions go hand-in-hand with an increasing number of tenants requesting green energy from photovoltaic systems, as they provide them with i) improved energy security, ii) a lower cost of occupancy, iii) compliance with increased regulation iv) compliance with their clients’ requirements and v) the ability to fulfil their own ESG ambitions.

Резултати процене вођени цевоводом и позитивном ревалоризацијом сталног портфеља

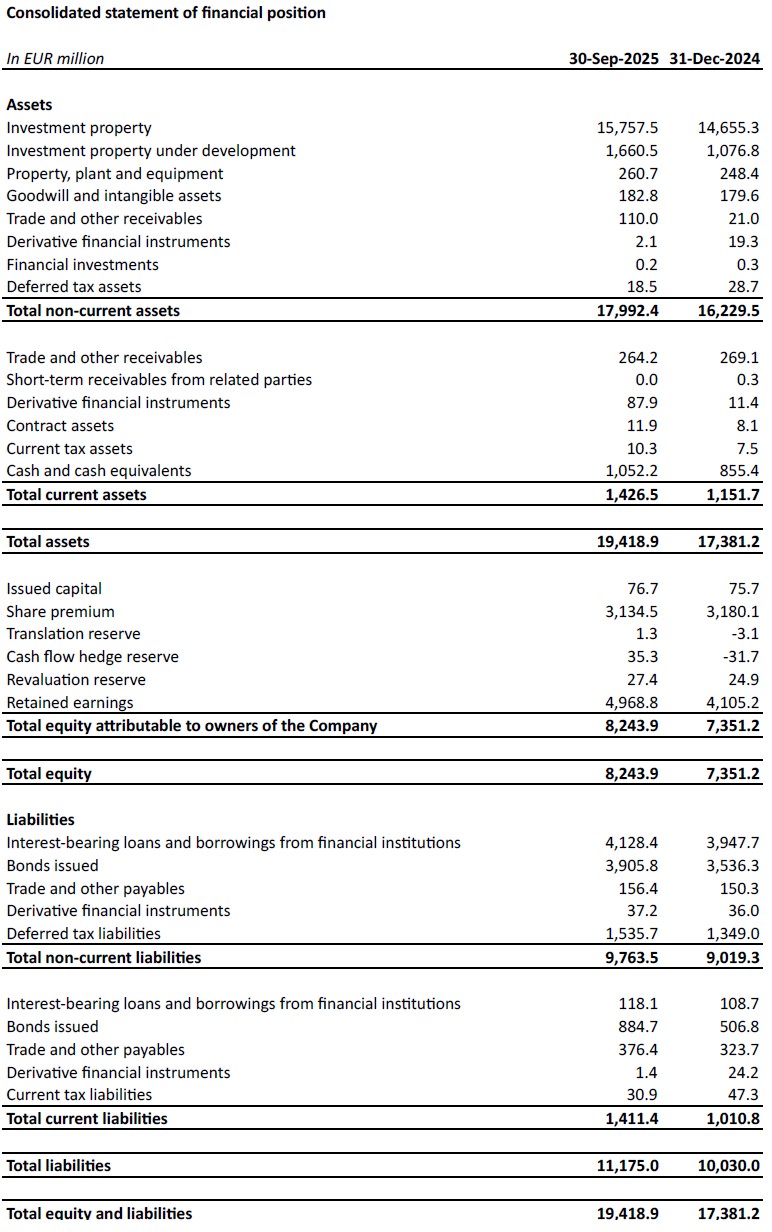

Investment Property (“IP”) valuation increased from €14.7 billion as at 31 December 2024 to €15.8 billion as at 30 September 2025, driven by the transfer of completed projects from Investment Property under Development (“IPuD”) to IP and positive revaluation of standing portfolio.

IPuD increased by 54.2% from 31 December 2024 to €1.7 billion as at 30 September 2025, driven by the CAPEX spent, the revaluation due to increased pre-letting and construction progress, and the start of new construction projects in 9M-2025.

GAV increased to €17.7 billion as at 30 September 2025, up 10.6% compared to 31 December 2024.

For the Q1 and Q3 results, only the IPuD projects are revalued. The revaluation in 9M-2025 came to €801.6 million, driven by the positive revaluation of IPuD projects (+€385.2 million), landbank (+€43.3 million), and the standings assets (+€373.0 million).

CTP expects further positive ERV growth on the back of continued tenant demand, which is positively impacted by the secular growth drivers in the CEE region. CEE rental levels remain affordable; despite the strong growth seen as they have started from significantly lower absolute levels than in Western European countries. In real terms, rents in many Central and Eastern European (“CEE”) markets are still below 2010 levels.

The Group’s portfolio has conservative valuation yields of 7.0%. The yield differential between CEE and Western European logistics is expected to decrease over time, driven by the higher growth expectations for the CEE region and increasing activity in the investment markets.

EPRA NTA per share increased from €18.08 as at 31 December 2024 to €19.98 as at 30 September 2025, representing an increase of 10.5% through 9M-2025, and an increase of 14.0% Y-o-Y. The increase is mainly driven by the revaluation (+€1.67), Company specific adjusted EPRA EPS (+€0.64) and offset by the final 2024 dividend paid out in May (-€0.30) and other items (-€0.11).

Робустан биланс стања и јака позиција ликвидности

У складу са својим проактивним и опрезним приступом, Група има користи од солидне позиције ликвидности за финансирање својих амбиција раста, са фиксним трошковима дуга и конзервативним профилом отплате.

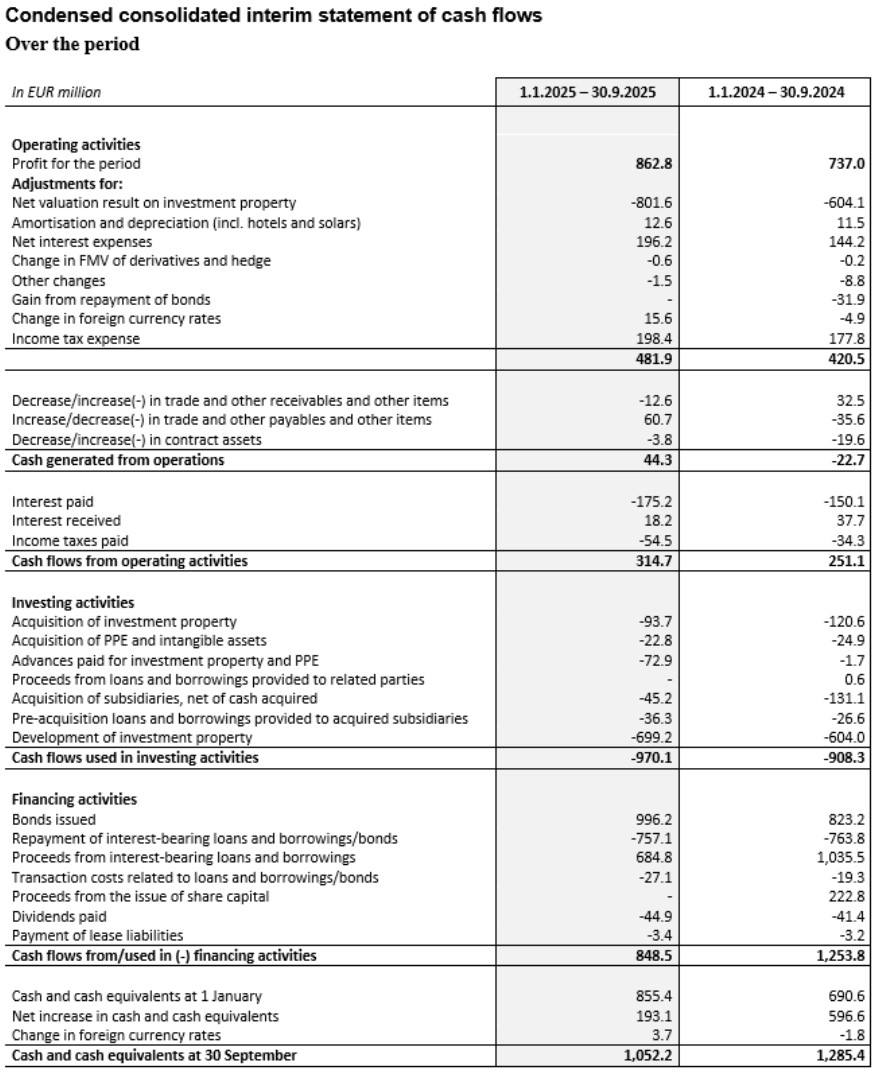

During 9M-2025, the Group secured €1.7 billion to fund its organic growth:

- Зелена обвезница од 1,0 милијарду евра са две транше, са шестогодишњом траншом од 500 милиона евра са каматном стопом MS +145 базних поена и купоном од 3,625% и десетогодишњом траншом од 500 милиона евра са каматном стопом MS +188 базних поена и купоном од 4,25%;

- Петогодишњи необезбеђени кредитни аранжман од 30 милијарди јена (еквивалентно 185 милиона евра) са синдикaтом азијских банака по каматној стопи од TONAR +130 базних поена и фиксним укупним трошковима од 4,1%; и

- A €500 million five-year unsecured sustainability-linked loan facility with a syndicate of 13 European and Asian banks at fixed all-in cost of 3.7%.

In addition, on 13 October 2025, CTP issued a new €600 million 6.5-year green bond at a MS +118bps and a coupon of 3.625%.

CTP continued to actively manage its bank loan portfolio in 9M-2025. Margin reduction on a further €193 million of secured bank loans was negotiated, and a €441 million unsecured term loan signed in 2023 was prepaid and refinanced by the new €500 million unsecured loan. Both allowed CTP to achieve material interest rate savings, reducing its overall cost of debt going forward.

The Group’s liquidity position stood at €2.4 billion, comprised of €1.1 billion in cash and cash equivalents, and an undrawn RCF of €1.3 billion.

Просечна цена дуга за CTP износила је 3,2% (фискална 2024: 3,1%), што је незнатно више у односу на крај 2024. године, због новог финансирања. 99,9% дуга има фиксну каматну стопу или је хеџиран до доспећа.

The Group doesn’t capitalise interest on developments, therefore all interest expenses are included in the P&L. The average debt maturity came to 4.8 years (FY-2024: 5.0 years).

The Group repaid a €272 million bond in June 2025 from its available cash reserves. There was another €185 million bond due in October 2025, also repaid from cash reserves.

CTP’s LTV came to 45.2% as at 30 September 2025, positively influenced by the strong revaluation of investment properties under development.

The Group’s higher yielding assets, thanks to their gross portfolio yield of 6.6%, lead to a healthy level of cash flow leverage that is also reflected in the normalised Net Debt to EBITDA of 9.2x (FY-2024: 9.1x), which the Group targets to keep below 10x.

The Group’s debt comprised of 68% unsecured debt and 32% secured as at 30 September 2025, with ample headroom under its Secured Debt Test and Unencumbered Asset Test covenants.

Како су цене на тржишту обвезница рационализоване, услови су сада конкурентнији од цена на тржишту банкарских кредита, што ће омогућити Групи да више балансира у правцу необезбеђеног кредитирања.

| 30 September 2025 | Завет | |

| Тест обезбеђеног дуга | 14.9% | 40% |

| Тест неоптерећене имовине | 190.6% | 125% |

| Однос покрића камата | 2,5 пута | 1,5к |

In Q3-2025, S&P upgraded CTP’s credit rating from BBB- to BBB with a stable outlook. In January 2025, CTP was assigned an A- credit rating with a stable outlook by the Japanese rating agency JCR. In Q2-2025, Moody’s upgraded outlook from stable to positive on its Baa3 credit rating.

Гуиданце

Leasing dynamics remain strong, with robust occupier demand, and decreasing new supply leading to continued rental growth. CTP is well positioned to benefit from these trends. The Group’s pipeline is highly profitable, and tenant led. The YoC for CTP’s current pipeline remains at an industry leading 10.2%. The next stage of growth is built in and financed, with 2.0 million sqm under construction as at 30 September 2025, with a target to deliver between 1.3 million sqm – 1.6 million sqm in 2025 and an additional 1.4 million sqm – 1.7 million sqm in 2026.

CTP’s robust capital structure, disciplined financial policy, strong credit market access, industry-leading landbank, in-house construction expertise and deep tenant relationships allow CTP to deliver on its targets. CTP expects to reach €1.0 billion rental income in 2027, driven by development completions, indexation and reversion. It is also on track to meet the ambition of 30 million sqm of GLA by the year 2030.

The Group confirms its €0.86 – €0.88 Company specific adjusted EPRA EPS guidance for 2025, which due to the intended acquisition in Romania not taking place, is now expected towards the lower end of the range. The EPRA EPS growth is driven by strong underlying growth, with around 4% like-for-like rental growth, partly off-set by the higher average cost of debt due to the (re-)financing in 2024 and 2025. The Group expects to return to double digit EPRA EPS growth in 2026.

CTP’s dividend policy is to pay-out 70% – 80% of the Company specific adjusted EPRA EPS. The default is a scrip dividend, but shareholders can opt for payment of the dividend in cash.

ВЕБЦАСТ И КОНФЕРЕНЦИЈСКИ ПОЗИВ ЗА АНАЛИТИЧАРЕ И ИНВЕСТИТОРЕ

Данас у 9:00 (ГМТ) и 10:00 (ЦЕТ), Компанија ће бити домаћин видео презентације и сесије питања и одговора за аналитичаре и инвеститоре, путем веб преноса уживо и аудио конференцијског позива.

Да бисте погледали веб пренос уживо, региструјте се унапред на:

https://www.investis-live.com/ctp/68dce560eefece00147ba94d/vbqpg

Да бисте се придружили презентацији телефоном, позовите један од следећих бројева и унесите приступни код учесника 128602.

Germany +49 32 22109 8334

France +33 9 70 73 39 58

The Netherlands +31 85 888 7233

United Kingdom +44 20 3936 2999

United States +1 646 664 1960

Притисните *1 да поставите питање, *2 да повучете своје питање или *0 за помоћ оператера.

Снимак ће бити доступан на веб страници ЦТП-а у року од 24 сата након презентације: https://ctp.eu/investors/financial-results/

ЦТП ФИНАНСИЈСКИ КАЛЕНДАР

| поступак | Датум |

| Резултати за фискалну 2025. годину | 26. фебруар 2026. |

| Q1-2026 results | 30 April 2026 |

| Годишње генерално окупљање | 20 May 2026 |

| H1-2026 results | 30 July 2026 |

| Дани тржишта капитала | September 2026 |

| Q3-2026 results | 29 October 2026 |

КОНТАКТ ПОДАЦИ ЗА УПИТЕ АНАЛИТИЧАРА И ИНВЕСТИТОРА:

Мартен Оте, шеф односа са инвеститорима и тржишта капитала

Мобилни: +420 730 197 500

Имејл: [email protected]

Павел Швихалек, менаџер за финансирање и ИР

Мобилни: +420 724 928 828

Емаил: [email protected]

КОНТАКТ ЗА МЕДИЈА УПИТАЊА:

Емаил: [email protected]

О ЦТП-у

CTP је највећи европски власник, инвеститор и менаџер логистичких и индустријских некретнина по бруто површини за издавање, са 13,8 милиона квадратних метара GLA у 10 земаља на дан 30. септембра 2025. CTP сертификује све нове зграде по BREEAM стандарду „Веома добро“ или „боље“ и добио је ESG оцену занемарљивог ризика од стране Sustainalytics-а, чиме истиче своју посвећеност одрживом пословању. За више информација посетите корпоративну веб страницу CTP-а: ввв.цтп.еу

Одрицање од одговорности

Ово саопштење садржи одређене изјаве о будућности у погледу финансијског стања, резултата пословања и пословања ЦТП-а. Ове изјаве о будућности могу се идентификовати употребом терминологије која се односи на будућност, укључујући изразе „верује“, „процене“, „планови“, „пројекти“, „очекује“, „намерава“, „циљеви ”, „може”, „циљ”, „вероватно”, „би”, „могао”, „може имати”, „хоће” или „треба” или, у сваком случају, њихове негативне или друге варијације или упоредиву терминологију. Изјаве које се односе на будућност могу и често се разликују материјално од стварних резултата. Као резултат тога, не би требало да се врши неприкладан утицај на било коју изјаву која се односи на будућност. Ово саопштење за јавност садржи инсајдерске информације како је дефинисано у члану 7(1) Уредбе (ЕУ) 596/2014 од 16. априла 2014. (Уредба о злоупотреби тржишта).

[1] Са мешавином локалног и ЦПИ ЕУ-27 / еврозоне, само ограничен број ограничења.

Пријавите се на наш билтен

Примајте најновије информације од лидера на тржишту индустријских некретнина директно у пријемно сандуче.