Výsledky CTP NV za 1. polrok 2025

STRONG LEASING ACTIVITY IN H1-2025 WITH 11% MORE SQM OF LEASES SIGNED, LIKE-FOR-LIKE RENTAL GROWTH OF 4.9%, AND EPRA NTA PER SHARE UP 13.5% YOY TO €19.36

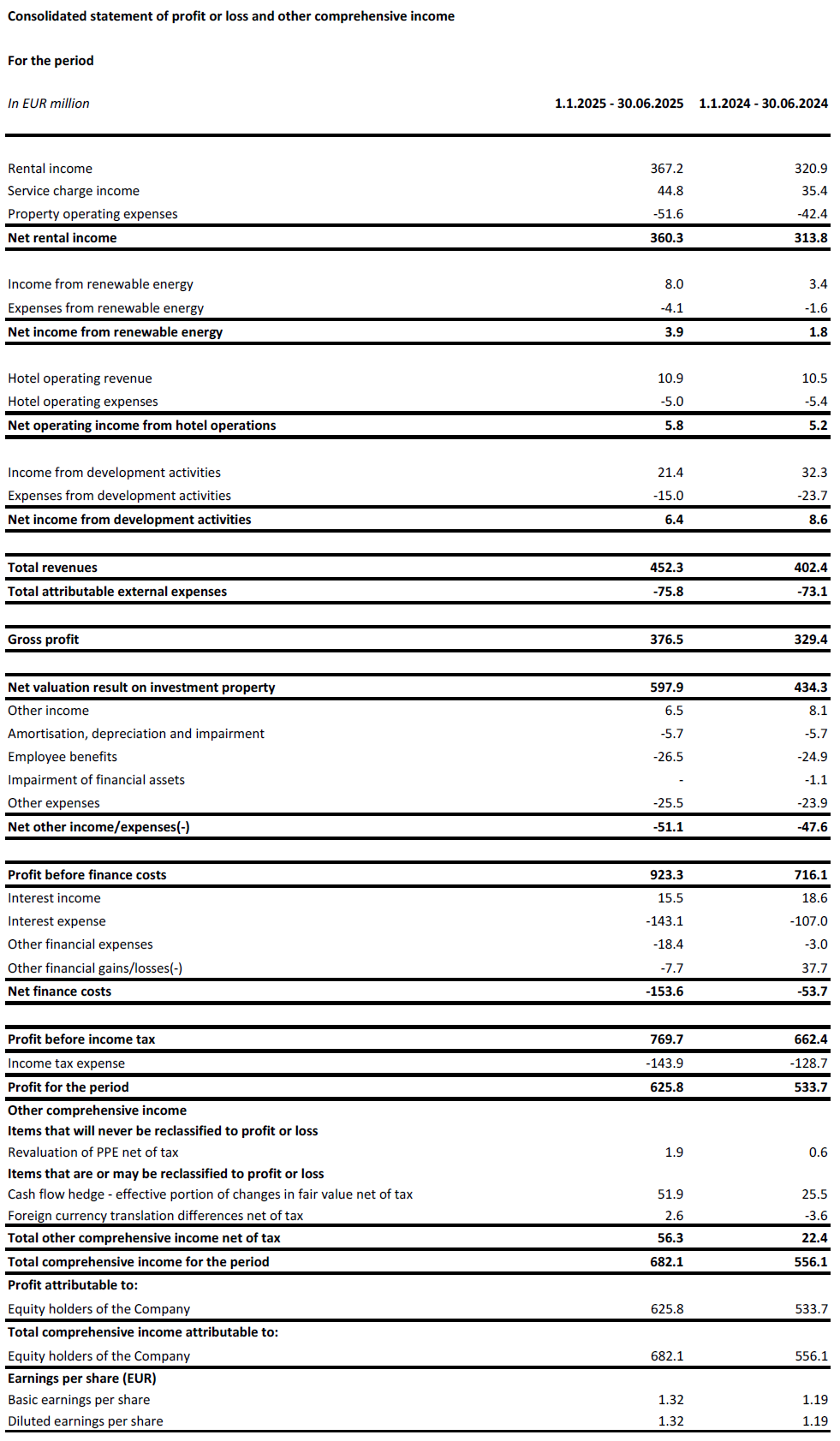

AMSTERDAM, 7 August 2025 – CTP N.V. (CTPNV.AS), (“CTP”, the “Group” or the “Company”) recorded in H1-2025 Gross Rental Income of €367.2 million, up 14.4% y-o-y, and like-for-like y-o-y rental growth of 4.9%, mainly driven by indexation and reversion on renegotiations and expiring leases. Leasing remained strong in the first half of the year with 11% more leases signed y-o-y. The average monthly rent on the new leases signed increased by 5% y-o-y[1].

As at 30 June 2025, the annualised rental income increased to €757 million, while occupancy remained at 93% and the rent collection rate was 99.7%.

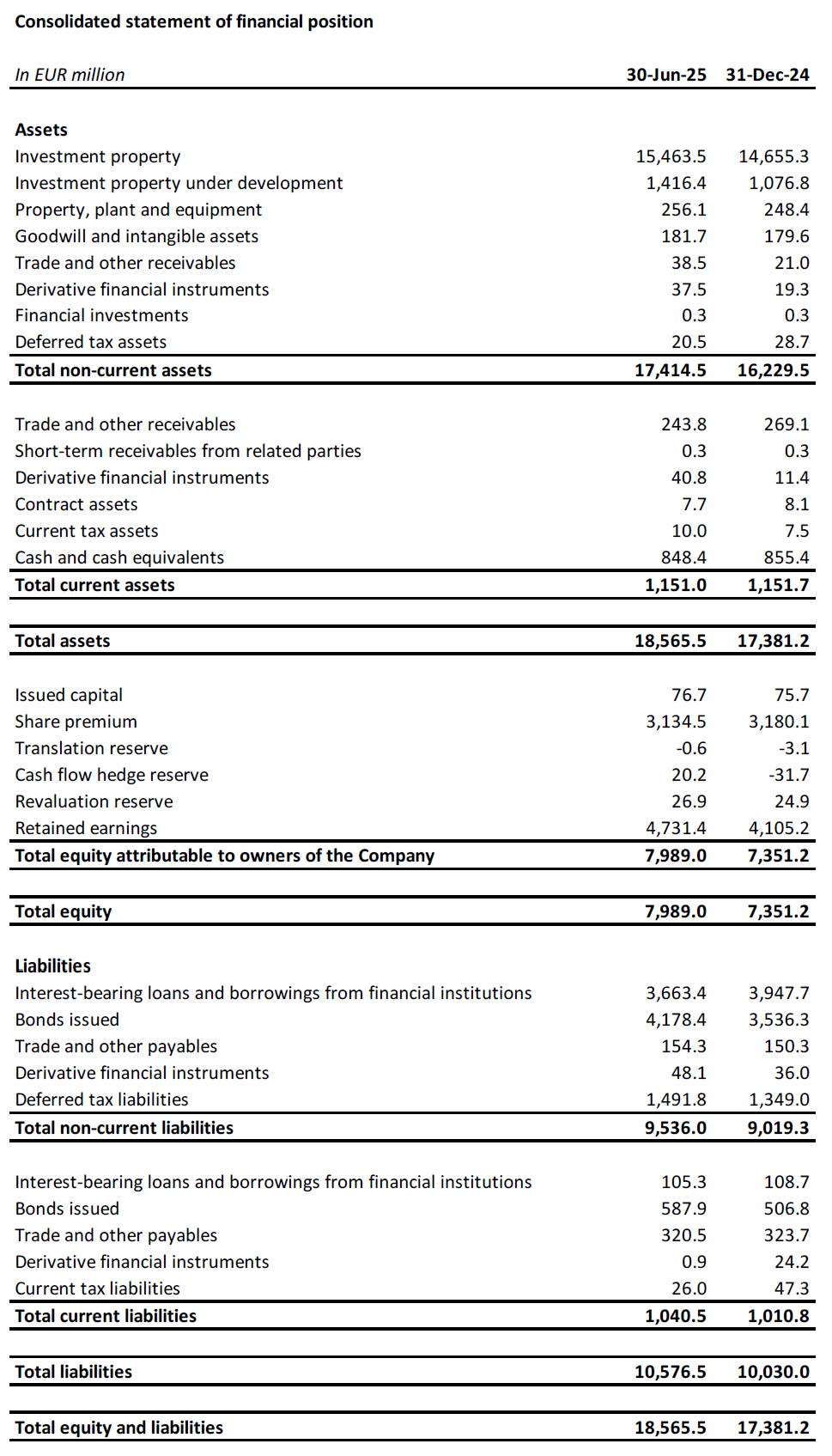

In the first half of the year, CTP delivered 224,000 sqm at a Yield on Cost (“YoC”) of 10.3% with 100% let at completion, bringing the Group’s standing portfolio to 13.5 million sqm of GLA. The like-for-like revaluation came to 4.0%, driven by ERV growth of 2.5%, with an average 11bps reversionary yield compression, while the Gross Asset Value (“GAV”) increased by 7.2% to €17.1 billion, and 15.9% y-o-y. EPRA NTA per share increased by 7.1% in H1 to €19.36 and 13.5% y-o-y, supported also by progress in the development pipeline.

Company specific adjusted EPRA earnings increased by 12.2% y-o-y to €199.3 million. CTP’s Company-specific adjusted EPRA EPS amounted to €0.42, an increase of 6.2%. The y-o-y increase in Company-specific adjusted EPRA EPS was negatively affected by the increased number of shares resulting from the equity raise in H2-2024. Thanks to our backloaded deliveries and net development income to the second half of the year, the Group is on track to reach the guidance of €0.86 – €0.88 for 2025, which represents 8 – 10% growth compared to 2024.

As at 30 June 2025, projects under construction totalled 2.0 million sqm with an expected YoC of 10.3%, and a potential rental income of €160 million when fully leased.

The Group’s landbank amounted to 26.1 million sqm, of which 22.2 million sqm is owned and on-balance sheet. This landbank secures substantial future growth potential for CTP, with 90% located around the existing business parks (58% in existing parks, 31% in new parks with a potential of over 100,000 GLA). Combined with its industry-leading YoC, CTP expects to continue to generate double-digit NTA growth in the years to come.

We are benefiting particularly from the nearshoring trend, shown by our growth with Asian manufacturing tenants, who made up around 20% of our overall leasing activity in the last 18 months, compared to an over 10% share of our overall portfolio.

The annualised rental income increased to €757 million. Our next phase of growth is already locked in through our 2.0 million sqm of GLA under construction and landbank of 26.1 million sqm, meaning we can continue generating double-digit NTA growth over the coming years. We are confident that we can achieve our ambitious goals and reach 1 billion annualized rental income in 2027.”

Kľúčové informácie

| V miliónoch EUR | H1-2025 | H1-2024 | Zmena % |

| Hrubý príjem z prenájmu | 367.2 | 320.9 | +14.4% |

| Čistý príjem z prenájmu | 360.3 | 313.8 | +14.8% |

| Čistý výsledok ocenenia investícií do nehnuteľností | 597.9 | 434.3 | +37.7% |

| Zisk za obdobie | 625.8 | 533.7 | +17.2% |

| Upravený zisk EPRA podľa spoločnosti | 199.3 | 177.6 | +12.2% |

| V € | H1-2025 | H1-2024 | Zmena % |

| Upravený zisk na akciu EPRA špecifický pre spoločnosť | 0.42 | 0.40 | +6.2% |

| V miliónoch EUR | 30 June 2025 | 31. decembra 2024 | Zmena % |

| Investície do nehnuteľností ("IP") | 15,463.5 | 14,655.3 | +5.5% |

| Investície do nehnuteľností vo výstavbe ("IPuD") | 1,416.4 | 1,076.8 | +31.5% |

| 30 June 2025 | 31. decembra 2024 | Zmena % | |

| EPRA NTA na akciu | €19.36 | €18.08 | +7.1% |

| Očakávaná ročná hodnota projektov vo výstavbe | 10.3% | 10.3% | |

| LTV | 44.9% | 45.3% |

Pokračujúci silný dopyt nájomcov poháňa rast nájomného

In H1-2025, CTP signed leases for 1,015,000 sqm, an increase of 11% compared to the same period in 2024, with an average monthly rent per sqm of €5.98 (H1-2024: €5.59). Adjusting for the differences among the country mix, rents increased on average by 5%.

| Podpísané nájomné zmluvy podľa m2 | Q1 | Q2 | YTD | Q3 | Q4 | FY |

| 2023 | 297,000 | 552,000 | 849,000 | 585,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 919,000 | 577,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 1,015,000 | |||

| medziročný rast | +24% | +3% | +11% |

| Priemerný mesačný nájom podpísaných zmlúv na m2 (€) | Q1 | Q2 | YTD | Q3 | Q4 | FY |

| 2023 | 5.31 | 5.56 | 5.47 | 5.77 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.59 | 5.69 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.98 |

Približne dve tretiny nájomných zmlúv boli podpísané s existujúcimi nájomníkmi, čo je v súlade s obchodným modelom CTP, ktorý spočíva v raste s existujúcimi nájomníkmi v existujúcich parkoch.

Generovanie cashflow prostredníctvom stáleho portfólia a akvizícií

CTP’s average market share in the Czech Republic, Romania, Hungary, and Slovakia came to 28.2% as at 30 June 2025 and it remains the largest owner and developer of industrial and logistics real estate assets in those markets. The Group is also the market leader in Serbia and Bulgaria.

With more than 1,500 clients, CTP has a wide and diversified international tenant base, consisting of blue-chip companies with strong credit ratings. CTP’s tenants represent a broad range of industries, including manufacturing, high-tech/IT, automotive, e-commerce, retail, wholesale, and 3PLs. The tenant base is highly diversified, with no single tenant accounting for more than 2.5% of the Company’s annual rent roll, which leads to a stable income stream. CTP’s top 50 tenants only account for 36.0% of its rent roll and the vast majority of clients rent space in multiple CTParks.

The Company’s occupancy came to 93% (FY-2024: 93%). The Group’s client retention rate remains strong at 85% (FY-2024: 87%) and demonstrates CTP’s ability to leverage long-standing client relationships. The portfolio WAULT stood at 6.2 years (FY-2024: 6.4 years), in line with the Company’s target of >6 years.

Rent collection level stood at 99.7% in H1-2025 (FY-2024: 99.8%), with no deterioration in the payment profile of tenants.

Rental income in H1-2025 amounted to €367.2 million, up 14.4% y-o-y on an absolute basis, mainly driven by deliveries and like-for-like growth. On a like-for-like basis, rental income grew 4.9%, thanks to indexation and reversion on renegotiations and expiring leases.

The Group has put measures in place to limit service charge leakage, which resulted in the improvement of the Net Rental Income to Rental Income ratio from 97.8% in H1-2024 to 98.1% in H1-2025. Consequently, the Net Rental Income increased 14.8% y-o-y.

Rastúca časť príjmov z prenájmu generovaných investičným portfóliom CTP profituje z ochrany pred infláciou. Od konca roka 2019 všetky nové nájomné zmluvy skupiny obsahujú klauzulu o indexácii viazanej na index spotrebiteľských cien, ktorá vypočítava ročné zvýšenie nájomného ako vyššiu z týchto hodnôt:

- fixné zvýšenie o 1,5%-2,5% ročne alebo

- index spotrebiteľských cien[2].

As at 30 June 2025, 72% of income generated by the Group’s portfolio includes this double indexation clause, and the Group expects this to increase further.

The reversionary potential came to 14.9%. New leases have been signed continuously above the Estimated Rental Value („ERV“), čo ilustruje pokračujúci silný rast nájomného na trhu a podporuje ocenenia.

The annualised rental income came to €757 million as at 30 June 2025, an increase of 11.5% y-o-y, showcasing the strong cash flow growth of CTP’s investment portfolio.

H1 developments delivered with a 10.3% YoC and 100% let at delivery

Spoločnosť CTP pokračovala v disciplinovaných investíciách do svojich vysoko ziskových produktov.

In H1-2025, the Group completed 224,000 sqm of GLA (H1-2024: 328,000 sqm). The developments were delivered at a YoC of 10.3%, 100% let and will generate contracted annual rental income of €12.1 million. As usual, the deliveries in 2025 are skewed to the fourth quarter.

While average construction costs in 2022 were around €550 per sqm, in 2023 and 2024 they came to €500 per sqm and remained stable in H1-2025. This allows the Group to continue to deliver its industry-leading YoC above 10%, which is also supported by CTP’s unique park model and in-house construction and procurement expertise.

As at 30 June 2025, the Group had 2.0 million sqm of buildings under construction with a potential rental income of €160 million and an expected YoC of 10.3%. CTP has a long track record of delivering sustainable growth through its tenant-led development in its existing parks. 79% of the Group’s projects under construction are in existing parks, while 9% are in new parks which have the potential to be developed to more than 100,000 sqm of GLA. Planned 2025 deliveries are 53% pre-let, up from 35% as at FY-2024. Pre-let in existing parks stood at 47%, while the new parks pre-let was at 80%, showcasing the low risk embedded in the pipeline. CTP expects to reach 80%-90% pre-letting at delivery, in line with historical performance. As CTP acts as general contractor in most markets, it is fully in control of the process and timing of deliveries, allowing the Company to speed-up or slow-down depending on tenant demand, while also offering tenants flexibility in terms of their building requirements.

In 2025 the Group is expecting to deliver between 1.2 – 1.7 million sqm, depending on tenant demand. The 106,000 sqm of leases that are already signed for future projects — construction of which hasn’t started yet — are a further illustration of continued occupier demand.

CTP’s landbank amounted to 26.1 million sqm as at 30 June 2025 (31 December 2024: 26.4 million sqm), which allows the Company to reach its target of 20 million sqm GLA by the end of the decade. The Group is focusing on mobilising the existing landbank, while maintaining disciplined capital allocation in landbank replenishment. 58% of the landbank is located within CTP’s existing parks, while 31% is in, or is adjacent to, new parks which have the potential to grow to more than 100,000 sqm. 15% of the landbank was secured by options, while the remaining 85% was owned and accordingly reflected in the balance sheet.

Assuming a build-up ratio of 2 sqm of land to 1 sqm of GLA, CTP can build over 13 million sqm of GLA on its secured landbank. CTP’s land is held on balance sheet at around €60 per sqm and construction costs amount on average to approximately €500 per sqm, bringing total investment costs to approximately €620 per sqm. The Group’s standing portfolio is valued around €1,040 per sqm, resulting in a revaluation potential of around €400 per sqm built.

Monetizácia energetického biznisu

CTP pokračuje v pláne expanzie v oblasti zavádzania fotovoltaických systémov. S priemernými nákladmi ~ 750 000 EUR na MWp sa Skupina pri týchto investíciách zameriava na YoC 151 TP3T.

CTP has an installed PV capacity of 138 MWp, of which 108 MWp is fully operational.

In H1-2025 the revenues from renewable energy came to €8.0 million, up 136% y-o-y mainly driven by the increase in capacity installed throughout 2024.

Ambície spoločnosti CTP v oblasti udržateľnosti idú ruka v ruke so stále väčším počtom nájomcov, ktorí požadujú fotovoltaické systémy, pretože im poskytujú i) lepšiu energetickú bezpečnosť, ii) nižšie náklady na užívanie, iii) súlad so zvýšenou reguláciou, iv) súlad s požiadavkami ich klientov a v) možnosť naplniť ich vlastné ambície v oblasti ESG.

Výsledky oceňovania poháňané potrubím a pozitívnym precenením stáleho portfólia

Investment Property (“IP”) valuation increased from €14.7 billion as at 31 December 2024 to €15.5 billion as at 30 June 2025, driven by the transfer of completed projects from Investment Property under Development (“IPuD”) to IP and positive revaluation of standing portfolio.

IPuD increased by 31.5% from 31 December 2024 to €1.4 billion as at 30 June 2025, driven by the CAPEX spent, the revaluation due to increase pre-letting and construction progress, and the start of new construction projects in H1-2025.

GAV increased to €17.1 billion as at 30 June 2025, up 7.2% compared to 31 December 2024.

The revaluation in H1-2025 came to €597.9 million, driven by the positive revaluation of IPuD projects (+€181.3 million), landbank (+€43.1 million), and the standings assets (+€373.6 million).

On a like-for-like basis, CTP’s portfolio saw a valuation increase of 4.0% during H1-2025, driven by an ERV growth of 2.5%.

Spoločnosť CTP očakáva ďalší pozitívny rast ERV (Energetickej hodnoty nehnuteľností) vďaka pokračujúcemu dopytu nájomcov, na ktorý pozitívne vplývajú dlhodobé faktory rastu v regióne strednej a východnej Európy. Nájomné v strednej a východnej Európe zostáva dostupné, a to aj napriek silnému rastu, keďže začínalo na výrazne nižších absolútnych úrovniach ako v západoeurópskych krajinách. V reálnom vyjadrení je nájomné na mnohých trhoch strednej a východnej Európy stále pod úrovňou z roku 2010.

The Group’s portfolio has conservative valuation yields of 7.0%. CTP saw further yield compression during the first half of 2025 of 11bps on average across the portfolio and expects further yield compression over second part of 2025. The yield differential between CEE and Western European logistics is expected to decrease over time, driven by the higher growth expectations for the CEE region and increasing activity in the investment markets.

EPRA NTA per share increased from €18.08 as at 31 December 2024 to €19.36 as at 30 June 2025, representing an y-o-y increase of 13.5% and an increase of 7.1% in H1-2025. The increase is mainly driven by the revaluation (+€1.25), Company specific adjusted EPRA EPS (+€0.42) and offset by final 2024 dividend paid out in May (-€0.30) and other items (-€0.09).

Pevná súvaha a silná likvidita

V súlade so svojím proaktívnym a obozretným prístupom skupina profituje z pevnej likvidnej pozície na financovanie svojich rastových ambícií, s fixnými nákladmi na dlh a konzervatívnym profilom splácania.

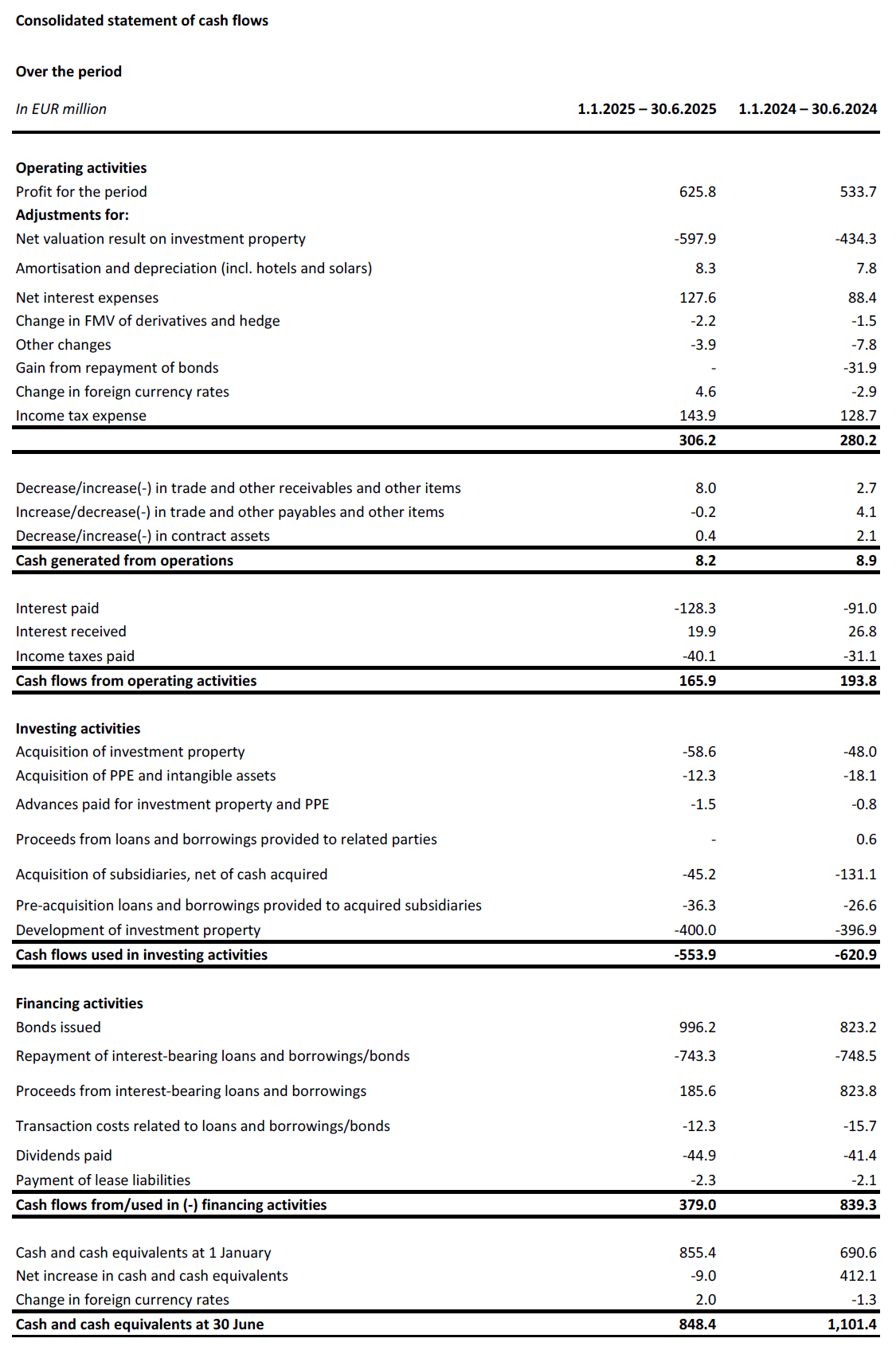

During H1-2025, the Group secured €1.7 billion to fund its organic growth:

- Zelený dlhopis s dvojitou tranžou v hodnote 1,0 miliardy EUR, pričom šesťročná tranža je 500 miliónov EUR pri MS +145 bázických bodov s kupónom 3,625% a desaťročná tranža je 500 miliónov EUR pri MS +188 bázických bodov s kupónom 4,25%;

- Päťročný nezabezpečený úver vo výške 30 miliárd JPY (ekvivalent 185 miliónov EUR) so syndikátom ázijských bánk s úrokovou sadzbou TONAR +130 bázických bodov a fixnými celkovými nákladmi 4,1%; a

- A €500 million five-year unsecured sustainability-linked loan facility with a syndicate of 13 European and Asian banks at fixed all-in cost of 3.7%, undrawn as of 30 June 2025.

CTP continued to actively manage its bank loan portfolio in H1-2025. Margin reduction on a further €159 million of secured bank loans was negotiated and €441 million of unsecured term loan signed in 2023 was prepaid and will be refinanced by the new €500 million unsecured loan. Both allowed CTP to achieve material interest rate savings and reduce the overall cost of debt going forward.

The Group’s liquidity position stood at €2.1 billion, comprised of €0.8 billion of cash and cash equivalents, and an undrawn RCF of €1.3 billion.

Priemerné náklady na dlh spoločnosti CTP dosiahli 3,21 TP7 týždňa (fiškálny rok 2024: 3,11 TP7 týždňa), čo je mierny nárast v porovnaní s koncom roka 2024 v dôsledku nového financovania. 99,91 TP7 týždňa dlhu má fixnú úrokovú sadzbu alebo je zaistený do splatnosti.

Skupina nekapitalizuje úroky z developerských projektov, preto sú všetky úrokové náklady zahrnuté vo výkaze ziskov a strát. Priemerná splatnosť dlhu bola 5,1 roka (fiškálny rok 2024: 5,0 roka).

The Group repaid €272 million bond in June 2025 from its available cash. Next upcoming maturity is a €185 million bond due in October 2025, which will also be repaid from available cash reserves.

CTP’s LTV decreased to 44.9% as at 30 June 2025 mainly due to the positive revaluation of standing portfolio and investment properties under development.

The Group’s higher yielding assets, thanks to their gross portfolio yield of 6.6%, lead to a healthy level of cash flow leverage that is also reflected in the normalized Net Debt to EBITDA of 9.2x (FY-2024: 9.1x), which the Group targets to keep below 10x.

The Group had 66% unsecured debt and 34% secured debt as at 30 June 2025, with ample headroom under its Secured Debt Test and Unencumbered Asset Test covenants.

S racionalizáciou oceňovania na trhu s dlhopismi sú teraz podmienky konkurencieschopnejšie ako ceny na trhu bankových úverov, čo umožní Skupine prehodnotiť rovnováhu smerom k nezabezpečeným úverom.

| 30 June 2025 | Covenant | |

| Test zabezpečeného dlhu | 15.7% | 40% |

| Test nezaťažených aktív | 194.9% | 125% |

| Pomer úrokového krytia | 2,4x | 1.5x |

In Q3-2024, S&P confirmed CTP’s BBB- credit rating with a stable outlook. In January 2025, CTP was assigned an A- credit rating with a stable outlook by the Japanese rating agency JCR. In Q2-2025, Moody’s upgraded outlook from stable to positive on Baa3 credit rating.

Usmernenie

Leasing dynamics remain strong, with robust occupier demand, and decreasing new supply leading to continued rental growth. CTP is well positioned to benefit from these trends. The Group’s pipeline is highly profitable, and tenant led. The YoC for CTP’s current pipeline remained at industry leading 10.3%. The next stage of growth is built in and financed, with 2.0 million sqm under construction as at 30 June 2025, with a target to deliver between 1.2 – 1.7 million sqm in 2025.

Robustná kapitálová štruktúra spoločnosti CTP, disciplinovaná finančná politika, silný prístup na úverový trh, popredná pozemková banka v odvetví, interné odborné znalosti v oblasti výstavby a hlboké vzťahy s nájomníkmi umožňujú spoločnosti CTP plniť svoje ciele. CTP očakáva, že v roku 2027 dosiahne príjmy z prenájmu vo výške 1,0 miliardy EUR, ktoré budú poháňané dokončením developerských projektov, indexáciou a reverziou, a je na dobrej ceste dosiahnuť 20 miliónov m² GLA a príjmy z prenájmu vo výške 1,2 miliardy EUR do konca desaťročia.

The Group set a guidance of €0.86 – €0.88 Company-specific adjusted EPRA EPS for 2025. This is driven by our strong underlying growth, with around 4% like-for-like growth, partly offset by a higher average cost of debt due to the (re)-financing in 2024 and 2025.

Dividenda

CTP announces an interim dividend of €0.31 per ordinary share, an increase of 6.9% compared to interim dividend 2024, and which represents a pay-out of 74% of the Company specific adjusted EPRA EPS, in line with the Group’s 70% – 80% dividend policy pay-out ratio. The default is a scrip dividend, but shareholders can opt for payment of the dividend in cash.

WEBCAST A KONFERENČNÝ HOVOR PRE ANALYTIKOV A INVESTOROV

Dnes o 9:00 (GMT) a 10:00 (CET) bude spoločnosť organizovať videoprezentáciu a zasadnutie s otázkami a odpoveďami pre analytikov a investorov prostredníctvom živého webového vysielania a audiokonferenčného hovoru.

Ak si chcete pozrieť živé webové vysielanie, zaregistrujte sa vopred na adrese:

https://www.investis-live.com/ctp/6863c5976c0d660016f95b35/kalwt

Ak sa chcete k prezentácii pripojiť telefonicky, vytočte jedno z nasledujúcich čísel a zadajte prístupový kód účastníka 893972.

Holandsko +31 85 888 7233

Spojené kráľovstvo +44 20 3936 2999

United States +1 646 664 1960

Stlačením tlačidla *1 položíte otázku, stlačením tlačidla *2 otázku stiahnete alebo stlačením tlačidla *0 získate pomoc operátora.

Záznam bude k dispozícii na webovej stránke CTP do 24 hodín po prezentácii: https://ctp.eu/investors/financial-results/

FINANČNÝ KALENDÁR CTP

| Akcia | Dátum |

| Dni kapitálového trhu (Wuppertal, Nemecko) | 24. – 25. septembra 2025 |

| Výsledky 3. štvrťroka 2025 | 6. novembra 2025 |

| Výsledky za fiškálny rok 2025 | 26. februára 2026 |

KONTAKTNÉ ÚDAJE PRE OTÁZKY ANALYTIKOV A INVESTOROV:

Maarten Otte, vedúci oddelenia vzťahov s investormi a kapitálových trhov

Mobilný telefón: +420 730 197 500

E-mail: [email protected]

KONTAKTNÉ ÚDAJE PRE OTÁZKY MÉDIÍ:

E-mail: [email protected]

O spoločnosti CTP

Spoločnosť CTP je najväčším európskym vlastníkom, developerom a správcom logistických a priemyselných nehnuteľností podľa hrubej prenajímateľnej plochy, pričom k 30. júnu 2025 vlastní 13,5 milióna m² prenajímateľných priestorov v 10 krajinách. Spoločnosť CTP certifikuje všetky nové budovy podľa štandardu BREEAM Very good alebo better a od spoločnosti Sustainalytics získala hodnotenie ESG so zanedbateľným rizikom, čím zdôrazňuje svoj záväzok byť udržateľným podnikom. Viac informácií nájdete na webovej stránke spoločnosti CTP: www.ctp.eu

Zrieknutie sa zodpovednosti

Toto oznámenie obsahuje určité výhľadové vyhlásenia týkajúce sa finančnej situácie, výsledkov činnosti a podnikania spoločnosti CTP. Tieto výhľadové vyhlásenia môžu byť identifikované použitím výhľadovej terminológie, vrátane výrazov "verí", "odhaduje", "plánuje", "projektuje", "očakáva", "predpokladá", "zamýšľa", "ciele", "môže", "ciele", "pravdepodobne", "by", "mohol", "môže mať", "bude" alebo "mal by" alebo v každom prípade ich negatívnych alebo iných variácií alebo porovnateľnej terminológie. Výhľadové vyhlásenia sa môžu podstatne líšiť a často sa aj líšia od skutočných výsledkov. V dôsledku toho by sa na žiadne výhľadové vyhlásenie nemal pripisovať neprimeraný vplyv. Táto tlačová správa obsahuje dôverné informácie v zmysle článku 7 ods. 1 nariadenia (EÚ) č. 596/2014 zo 16. apríla 2014 (nariadenie o zneužívaní trhu).

[1] Upravené pre mix vidieckej hudby.

[2] Pri kombinácii miestneho CPI a CPI EÚ-27 / eurozóny len obmedzený počet stropov.

Prihláste sa na odber nášho newslettera

Získajte najnovšie informácie od lídra na trhu s priemyselnými nehnuteľnosťami priamo do svojej e-mailovej schránky.