CTP NV 2025. első féléves eredményei

STRONG LEASING ACTIVITY IN H1-2025 WITH 11% MORE SQM OF LEASES SIGNED, LIKE-FOR-LIKE RENTAL GROWTH OF 4.9%, AND EPRA NTA PER SHARE UP 13.5% YOY TO €19.36

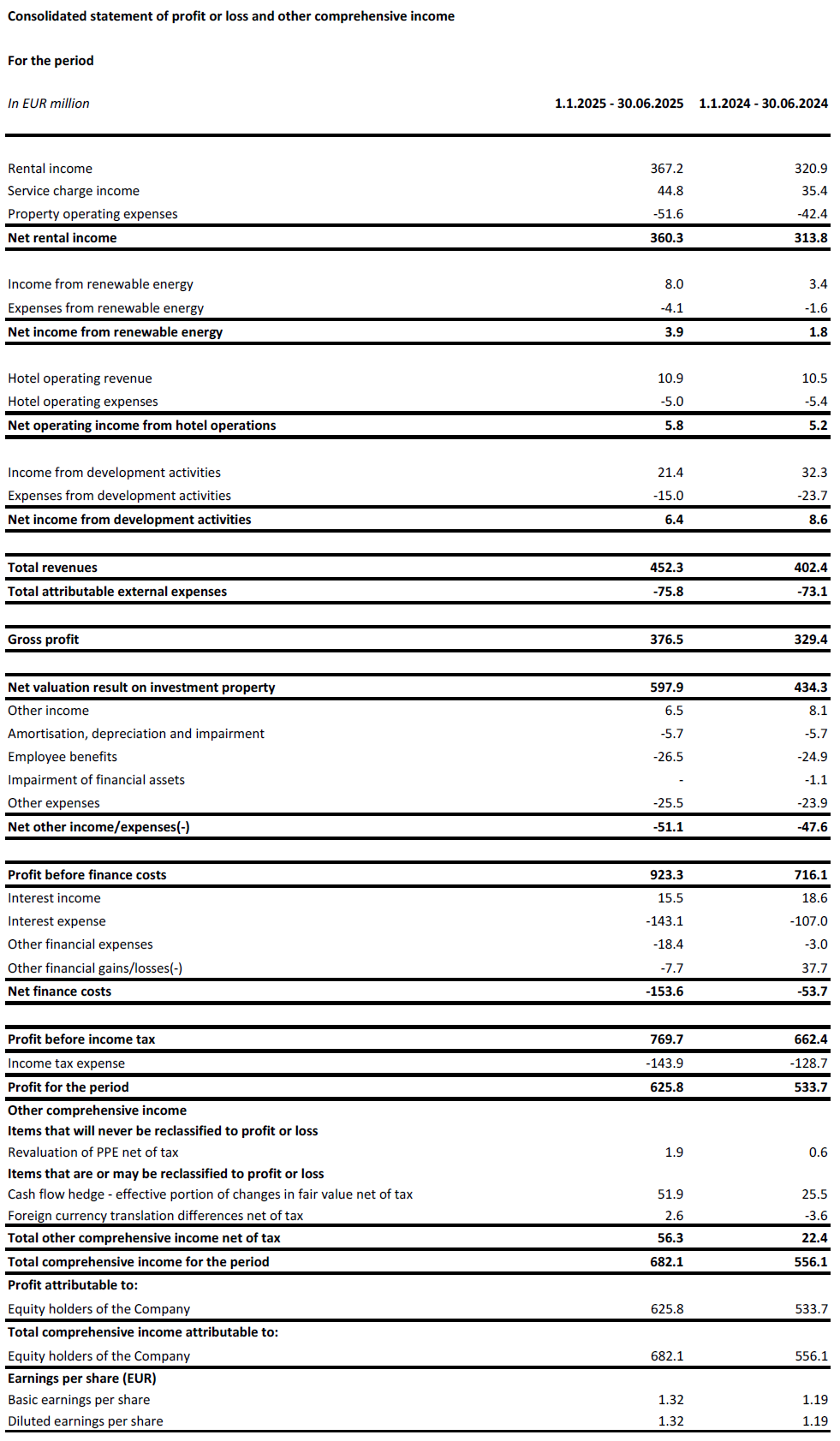

AMSTERDAM, 7 August 2025 – CTP N.V. (CTPNV.AS), (“CTP”, the “Group” or the “Company”) recorded in H1-2025 Gross Rental Income of €367.2 million, up 14.4% y-o-y, and like-for-like y-o-y rental growth of 4.9%, mainly driven by indexation and reversion on renegotiations and expiring leases. Leasing remained strong in the first half of the year with 11% more leases signed y-o-y. The average monthly rent on the new leases signed increased by 5% y-o-y[1].

As at 30 June 2025, the annualised rental income increased to €757 million, while occupancy remained at 93% and the rent collection rate was 99.7%.

In the first half of the year, CTP delivered 224,000 sqm at a Yield on Cost (“YoC”) of 10.3% with 100% let at completion, bringing the Group’s standing portfolio to 13.5 million sqm of GLA. The like-for-like revaluation came to 4.0%, driven by ERV growth of 2.5%, with an average 11bps reversionary yield compression, while the Gross Asset Value (“GAV”) increased by 7.2% to €17.1 billion, and 15.9% y-o-y. EPRA NTA per share increased by 7.1% in H1 to €19.36 and 13.5% y-o-y, supported also by progress in the development pipeline.

Company specific adjusted EPRA earnings increased by 12.2% y-o-y to €199.3 million. CTP’s Company-specific adjusted EPRA EPS amounted to €0.42, an increase of 6.2%. The y-o-y increase in Company-specific adjusted EPRA EPS was negatively affected by the increased number of shares resulting from the equity raise in H2-2024. Thanks to our backloaded deliveries and net development income to the second half of the year, the Group is on track to reach the guidance of €0.86 – €0.88 for 2025, which represents 8 – 10% growth compared to 2024.

As at 30 June 2025, projects under construction totalled 2.0 million sqm with an expected YoC of 10.3%, and a potential rental income of €160 million when fully leased.

The Group’s landbank amounted to 26.1 million sqm, of which 22.2 million sqm is owned and on-balance sheet. This landbank secures substantial future growth potential for CTP, with 90% located around the existing business parks (58% in existing parks, 31% in new parks with a potential of over 100,000 GLA). Combined with its industry-leading YoC, CTP expects to continue to generate double-digit NTA growth in the years to come.

We are benefiting particularly from the nearshoring trend, shown by our growth with Asian manufacturing tenants, who made up around 20% of our overall leasing activity in the last 18 months, compared to an over 10% share of our overall portfolio.

The annualised rental income increased to €757 million. Our next phase of growth is already locked in through our 2.0 million sqm of GLA under construction and landbank of 26.1 million sqm, meaning we can continue generating double-digit NTA growth over the coming years. We are confident that we can achieve our ambitious goals and reach 1 billion annualized rental income in 2027.”

Főbb jellemzők

| Millió euróban | H1-2025 | H1-2024 | % változás |

| bérbeadásból származó bruttó bevétel | 367.2 | 320.9 | +14.4% |

| Nettó bérleti bevétel | 360.3 | 313.8 | +14.8% |

| Befektetési célú ingatlanok nettó értékelési eredménye | 597.9 | 434.3 | +37.7% |

| Az időszak nyeresége | 625.8 | 533.7 | +17.2% |

| Vállalatspecifikus korrigált EPRA eredmény | 199.3 | 177.6 | +12.2% |

| €-ban | H1-2025 | H1-2024 | % változás |

| Vállalatspecifikus korrigált EPRA EPS | 0.42 | 0.40 | +6.2% |

| Millió euróban | 30 June 2025 | 2024. december 31. | % változás |

| Befektetési célú ingatlanok ("IP") | 15,463.5 | 14,655.3 | +5.5% |

| Fejlesztés alatt álló befektetési célú ingatlanok ("IPuD") | 1,416.4 | 1,076.8 | +31.5% |

| 30 June 2025 | 2024. december 31. | % változás | |

| EPRA NTA részvényenként | €19.36 | €18.08 | +7.1% |

| Az építés alatt álló projektek várható teljesítési ideje | 10.3% | 10.3% | |

| LTV | 44.9% | 45.3% |

A továbbra is erős bérlői kereslet ösztönzi a bérleti díjak növekedését

In H1-2025, CTP signed leases for 1,015,000 sqm, an increase of 11% compared to the same period in 2024, with an average monthly rent per sqm of €5.98 (H1-2024: €5.59). Adjusting for the differences among the country mix, rents increased on average by 5%.

| Aláírt bérleti szerződések négyzetméterenként | Q1 | Q2 | YTD | Q3 | Q4 | FY |

| 2023 | 297,000 | 552,000 | 849,000 | 585,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 919,000 | 577,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 1,015,000 | |||

| Éves növekedés | +24% | +3% | +11% |

| Átlagos havi bérleti díjak négyzetméterenként (€) | Q1 | Q2 | YTD | Q3 | Q4 | FY |

| 2023 | 5.31 | 5.56 | 5.47 | 5.77 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.59 | 5.69 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.98 |

A bérleti szerződések körülbelül kétharmadát meglévő bérlőkkel kötötték, összhangban a CTP üzleti modelljével, amely a meglévő parkokban a meglévő bérlőkkel együtt növekszik.

Cashflow generálás állandó portfólión és felvásárlásokon keresztül

CTP’s average market share in the Czech Republic, Romania, Hungary, and Slovakia came to 28.2% as at 30 June 2025 and it remains the largest owner and developer of industrial and logistics real estate assets in those markets. The Group is also the market leader in Serbia and Bulgaria.

With more than 1,500 clients, CTP has a wide and diversified international tenant base, consisting of blue-chip companies with strong credit ratings. CTP’s tenants represent a broad range of industries, including manufacturing, high-tech/IT, automotive, e-commerce, retail, wholesale, and 3PLs. The tenant base is highly diversified, with no single tenant accounting for more than 2.5% of the Company’s annual rent roll, which leads to a stable income stream. CTP’s top 50 tenants only account for 36.0% of its rent roll and the vast majority of clients rent space in multiple CTParks.

The Company’s occupancy came to 93% (FY-2024: 93%). The Group’s client retention rate remains strong at 85% (FY-2024: 87%) and demonstrates CTP’s ability to leverage long-standing client relationships. The portfolio WAULT stood at 6.2 years (FY-2024: 6.4 years), in line with the Company’s target of >6 years.

Rent collection level stood at 99.7% in H1-2025 (FY-2024: 99.8%), with no deterioration in the payment profile of tenants.

Rental income in H1-2025 amounted to €367.2 million, up 14.4% y-o-y on an absolute basis, mainly driven by deliveries and like-for-like growth. On a like-for-like basis, rental income grew 4.9%, thanks to indexation and reversion on renegotiations and expiring leases.

The Group has put measures in place to limit service charge leakage, which resulted in the improvement of the Net Rental Income to Rental Income ratio from 97.8% in H1-2024 to 98.1% in H1-2025. Consequently, the Net Rental Income increased 14.8% y-o-y.

An increasing proportion of the rental income generated by CTP’s investment portfolio benefits from inflation protection. Since end-2019, all the Group’s new lease agreements include a CPI linked indexation clause, which calculates annual rental increases as the higher of:

- évi 1,5%-2,5% fix emelés; vagy

- a fogyasztói árindex[2].

As at 30 June 2025, 72% of income generated by the Group’s portfolio includes this double indexation clause, and the Group expects this to increase further.

The reversionary potential came to 14.9%. New leases have been signed continuously above the Estimated Rental Value (“ERV”), illustrating continued strong market rental growth and supporting valuations.

The annualised rental income came to €757 million as at 30 June 2025, an increase of 11.5% y-o-y, showcasing the strong cash flow growth of CTP’s investment portfolio.

H1 developments delivered with a 10.3% YoC and 100% let at delivery

A CTP folytatta fegyelmezett beruházásait a rendkívül jövedelmező csővezetékébe.

In H1-2025, the Group completed 224,000 sqm of GLA (H1-2024: 328,000 sqm). The developments were delivered at a YoC of 10.3%, 100% let and will generate contracted annual rental income of €12.1 million. As usual, the deliveries in 2025 are skewed to the fourth quarter.

While average construction costs in 2022 were around €550 per sqm, in 2023 and 2024 they came to €500 per sqm and remained stable in H1-2025. This allows the Group to continue to deliver its industry-leading YoC above 10%, which is also supported by CTP’s unique park model and in-house construction and procurement expertise.

As at 30 June 2025, the Group had 2.0 million sqm of buildings under construction with a potential rental income of €160 million and an expected YoC of 10.3%. CTP has a long track record of delivering sustainable growth through its tenant-led development in its existing parks. 79% of the Group’s projects under construction are in existing parks, while 9% are in new parks which have the potential to be developed to more than 100,000 sqm of GLA. Planned 2025 deliveries are 53% pre-let, up from 35% as at FY-2024. Pre-let in existing parks stood at 47%, while the new parks pre-let was at 80%, showcasing the low risk embedded in the pipeline. CTP expects to reach 80%-90% pre-letting at delivery, in line with historical performance. As CTP acts as general contractor in most markets, it is fully in control of the process and timing of deliveries, allowing the Company to speed-up or slow-down depending on tenant demand, while also offering tenants flexibility in terms of their building requirements.

In 2025 the Group is expecting to deliver between 1.2 – 1.7 million sqm, depending on tenant demand. The 106,000 sqm of leases that are already signed for future projects — construction of which hasn’t started yet — are a further illustration of continued occupier demand.

CTP’s landbank amounted to 26.1 million sqm as at 30 June 2025 (31 December 2024: 26.4 million sqm), which allows the Company to reach its target of 20 million sqm GLA by the end of the decade. The Group is focusing on mobilising the existing landbank, while maintaining disciplined capital allocation in landbank replenishment. 58% of the landbank is located within CTP’s existing parks, while 31% is in, or is adjacent to, new parks which have the potential to grow to more than 100,000 sqm. 15% of the landbank was secured by options, while the remaining 85% was owned and accordingly reflected in the balance sheet.

Assuming a build-up ratio of 2 sqm of land to 1 sqm of GLA, CTP can build over 13 million sqm of GLA on its secured landbank. CTP’s land is held on balance sheet at around €60 per sqm and construction costs amount on average to approximately €500 per sqm, bringing total investment costs to approximately €620 per sqm. The Group’s standing portfolio is valued around €1,040 per sqm, resulting in a revaluation potential of around €400 per sqm built.

Az energiaüzlet monetizálása

A CTP folytatja a fotovoltaikus rendszerek kiépítésére vonatkozó bővítési tervét. A csoport átlagosan ~750 000 €/MWp költséggel 15% YoC-t céloz meg ezekre a beruházásokra.

CTP has an installed PV capacity of 138 MWp, of which 108 MWp is fully operational.

In H1-2025 the revenues from renewable energy came to €8.0 million, up 136% y-o-y mainly driven by the increase in capacity installed throughout 2024.

A CTP fenntarthatósági törekvései együtt járnak azzal, hogy egyre több bérlő kéri a fotovoltaikus rendszereket, mivel azok i) nagyobb energiabiztonságot, ii) alacsonyabb lakhatási költségeket, iii) a fokozott szabályozásnak való megfelelést, iv) az ügyfelek követelményeinek való megfelelést és v) saját ESG ambícióik teljesítésének lehetőségét biztosítják számukra.

Az értékelési eredményeket a folyamatban lévő portfólió pozitív átértékelése és a folyamatban lévő értékesítési folyamat vezérelte

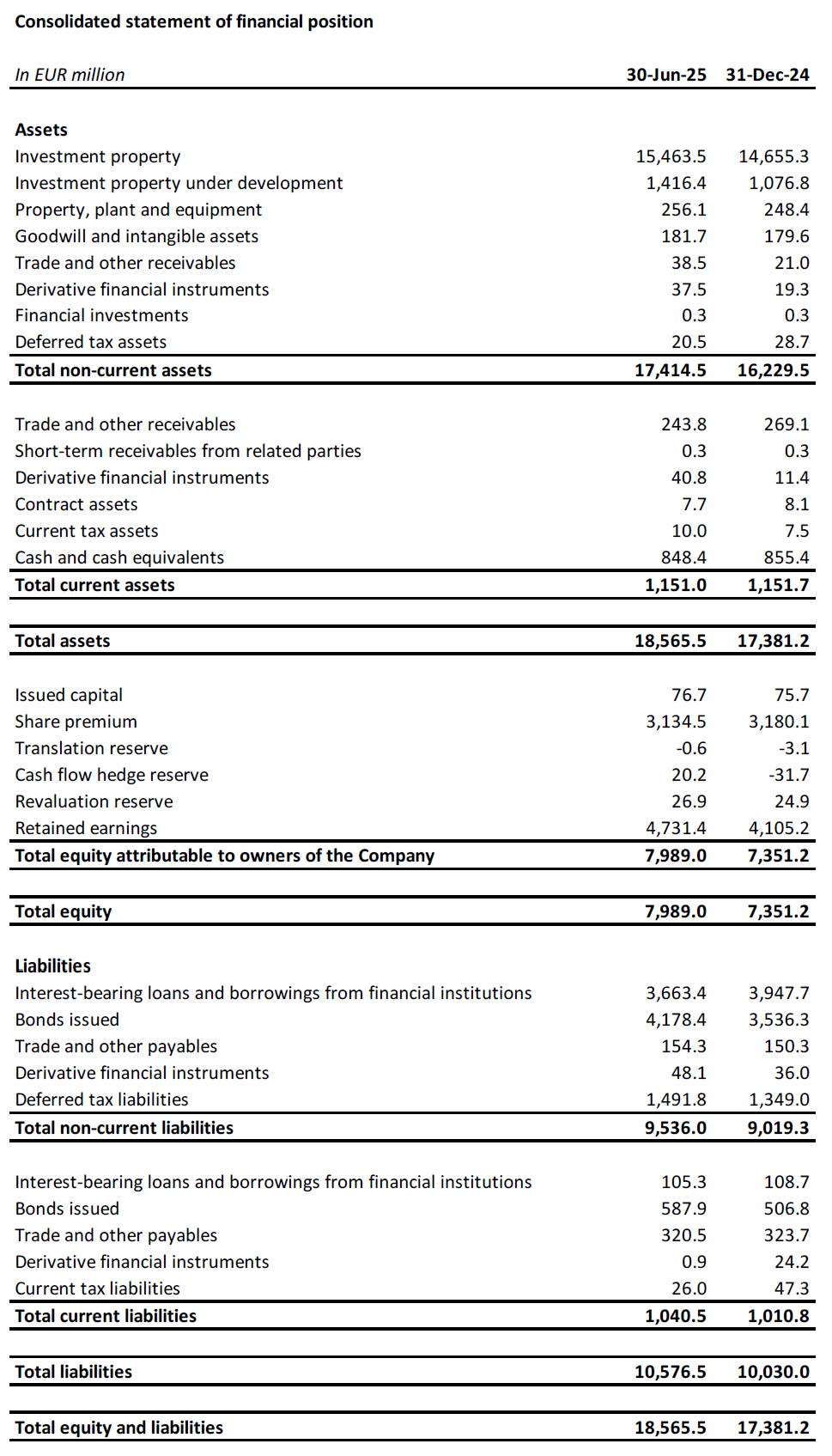

Investment Property (“IP”) valuation increased from €14.7 billion as at 31 December 2024 to €15.5 billion as at 30 June 2025, driven by the transfer of completed projects from Investment Property under Development (“IPuD”) to IP and positive revaluation of standing portfolio.

IPuD increased by 31.5% from 31 December 2024 to €1.4 billion as at 30 June 2025, driven by the CAPEX spent, the revaluation due to increase pre-letting and construction progress, and the start of new construction projects in H1-2025.

GAV increased to €17.1 billion as at 30 June 2025, up 7.2% compared to 31 December 2024.

The revaluation in H1-2025 came to €597.9 million, driven by the positive revaluation of IPuD projects (+€181.3 million), landbank (+€43.1 million), and the standings assets (+€373.6 million).

On a like-for-like basis, CTP’s portfolio saw a valuation increase of 4.0% during H1-2025, driven by an ERV growth of 2.5%.

CTP expects further positive ERV growth on the back of continued tenant demand, which is positively impacted by the secular growth drivers in the CEE region. CEE rental levels remain affordable; despite the strong growth seen as they have started from significantly lower absolute levels than in Western European countries. In real terms, rents in many CEE markets are still below 2010 levels.

The Group’s portfolio has conservative valuation yields of 7.0%. CTP saw further yield compression during the first half of 2025 of 11bps on average across the portfolio and expects further yield compression over second part of 2025. The yield differential between CEE and Western European logistics is expected to decrease over time, driven by the higher growth expectations for the CEE region and increasing activity in the investment markets.

EPRA NTA per share increased from €18.08 as at 31 December 2024 to €19.36 as at 30 June 2025, representing an y-o-y increase of 13.5% and an increase of 7.1% in H1-2025. The increase is mainly driven by the revaluation (+€1.25), Company specific adjusted EPRA EPS (+€0.42) and offset by final 2024 dividend paid out in May (-€0.30) and other items (-€0.09).

Robusztus mérleg és erős likviditási pozíció

A proaktív és prudens megközelítéssel összhangban a Csoport szilárd likviditási pozícióval rendelkezik, amely lehetővé teszi növekedési törekvéseinek finanszírozását, fix adósságköltséggel és konzervatív törlesztési profillal.

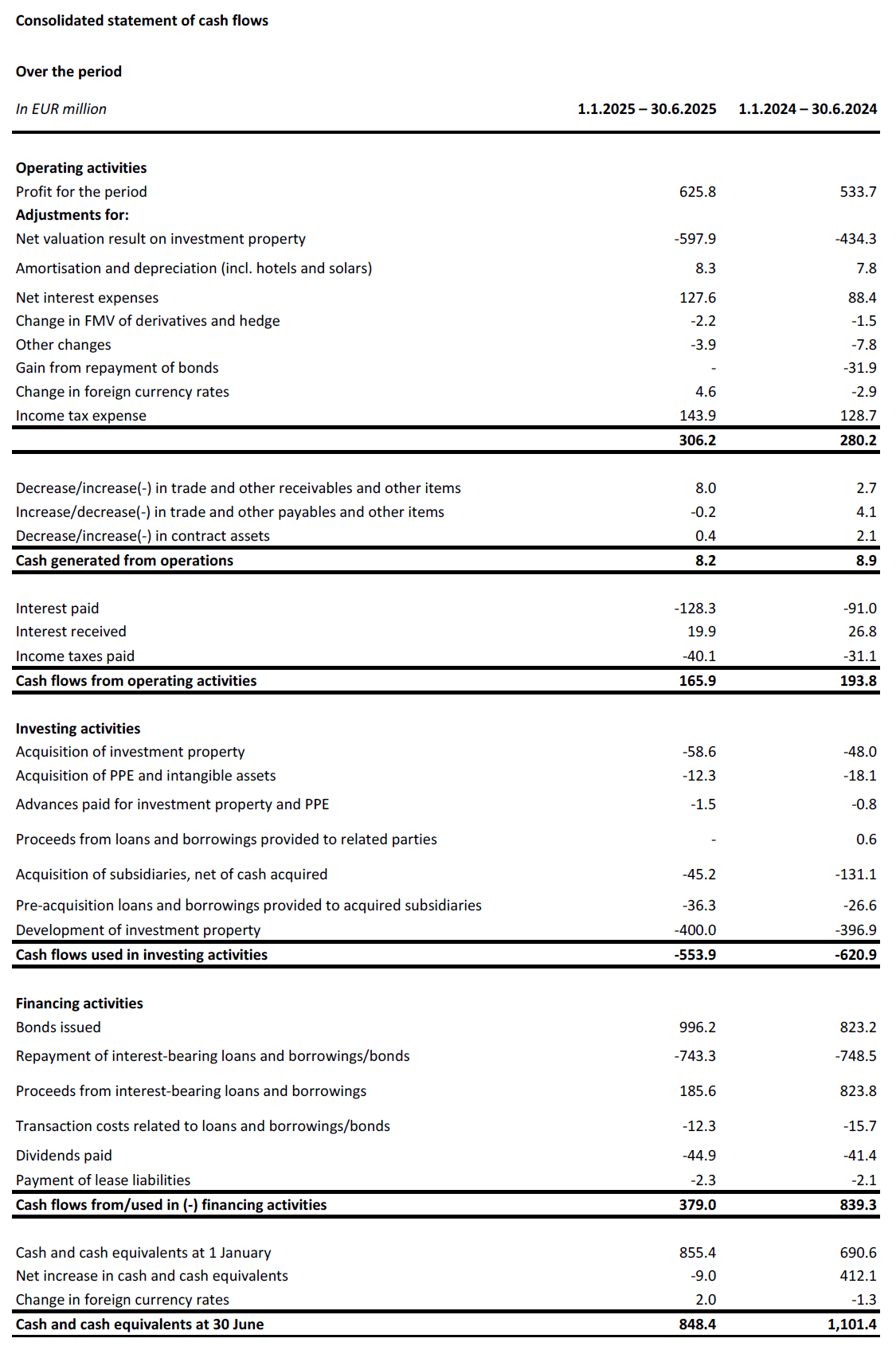

During H1-2025, the Group secured €1.7 billion to fund its organic growth:

- Egy 1,0 milliárd eurós, kettős tranche-s zöld kötvény, amelyből egy 500 millió eurós, hatéves futamidejű tranche MS +145 bázisponttal és 3,625% kamatlábbal, valamint egy 500 millió eurós, tízéves futamidejű tranche MS +188 bázisponttal és 4,25% kamatlábbal rendelkezik;

- Egy 30 milliárd JPY (185 millió eurónak megfelelő) értékű, ötéves, fedezetlen hitelkeret ázsiai bankok szindikátusával, TONAR +130 bázispont kamattal és 4,1% fix összköltséggel; és

- A €500 million five-year unsecured sustainability-linked loan facility with a syndicate of 13 European and Asian banks at fixed all-in cost of 3.7%, undrawn as of 30 June 2025.

CTP continued to actively manage its bank loan portfolio in H1-2025. Margin reduction on a further €159 million of secured bank loans was negotiated and €441 million of unsecured term loan signed in 2023 was prepaid and will be refinanced by the new €500 million unsecured loan. Both allowed CTP to achieve material interest rate savings and reduce the overall cost of debt going forward.

The Group’s liquidity position stood at €2.1 billion, comprised of €0.8 billion of cash and cash equivalents, and an undrawn RCF of €1.3 billion.

A CTP átlagos adósságköltsége 3,21 TP7T volt (2024-es pénzügyi év: 3,11 TP7T), ami kismértékben emelkedett a 2024-es év végéhez képest, az új finanszírozásnak köszönhetően. Az adósság 99,91 TP7T fix kamatozású vagy lejáratig fedezett.

The Group doesn’t capitalise interest on developments, therefore all interest expenses are included in the P&L. The average debt maturity came to 5.1 years (FY-2024: 5.0 years).

The Group repaid €272 million bond in June 2025 from its available cash. Next upcoming maturity is a €185 million bond due in October 2025, which will also be repaid from available cash reserves.

CTP’s LTV decreased to 44.9% as at 30 June 2025 mainly due to the positive revaluation of standing portfolio and investment properties under development.

The Group’s higher yielding assets, thanks to their gross portfolio yield of 6.6%, lead to a healthy level of cash flow leverage that is also reflected in the normalized Net Debt to EBITDA of 9.2x (FY-2024: 9.1x), which the Group targets to keep below 10x.

The Group had 66% unsecured debt and 34% secured debt as at 30 June 2025, with ample headroom under its Secured Debt Test and Unencumbered Asset Test covenants.

A kötvénypiaci árazás racionalizálódásával a feltételek immár versenyképesebbek, mint a banki hitelpiaci árazás, ami lehetővé teszi a Csoport számára, hogy jobban egyensúlyba kerüljön a fedezetlen hitelezés irányába.

| 30 June 2025 | Szövetség | |

| Biztosított adósságteszt | 15.7% | 40% |

| Tehermentes eszköz teszt | 194.9% | 125% |

| kamatfedezeti arány | 2,4x | 1.5x |

In Q3-2024, S&P confirmed CTP’s BBB- credit rating with a stable outlook. In January 2025, CTP was assigned an A- credit rating with a stable outlook by the Japanese rating agency JCR. In Q2-2025, Moody’s upgraded outlook from stable to positive on Baa3 credit rating.

Útmutatás

Leasing dynamics remain strong, with robust occupier demand, and decreasing new supply leading to continued rental growth. CTP is well positioned to benefit from these trends. The Group’s pipeline is highly profitable, and tenant led. The YoC for CTP’s current pipeline remained at industry leading 10.3%. The next stage of growth is built in and financed, with 2.0 million sqm under construction as at 30 June 2025, with a target to deliver between 1.2 – 1.7 million sqm in 2025.

CTP’s robust capital structure, disciplined financial policy, strong credit market access, industry-leading landbank, in-house construction expertise and deep tenant relationships allow CTP to deliver on its targets. CTP expects to reach €1.0 billion rental income in 2027, driven by development completions, indexation and reversion, and is on track to reach 20 million sqm of GLA and €1.2 billion rental income before the end of the decade.

The Group set a guidance of €0.86 – €0.88 Company-specific adjusted EPRA EPS for 2025. This is driven by our strong underlying growth, with around 4% like-for-like growth, partly offset by a higher average cost of debt due to the (re)-financing in 2024 and 2025.

Osztalék

CTP announces an interim dividend of €0.31 per ordinary share, an increase of 6.9% compared to interim dividend 2024, and which represents a pay-out of 74% of the Company specific adjusted EPRA EPS, in line with the Group’s 70% – 80% dividend policy pay-out ratio. The default is a scrip dividend, but shareholders can opt for payment of the dividend in cash.

WEBCAST ÉS KONFERENCIAHÍVÁS ELEMZŐK ÉS BEFEKTETŐK SZÁMÁRA

Ma 9 órakor (GMT) és 10 órakor (CET) a vállalat élő internetes közvetítés és hangos konferenciahívás keretében videóbemutatót és kérdezz-feleleket tart az elemzők és befektetők számára.

Az élő webcast megtekintéséhez kérjük, regisztráljon a következő címen:

https://www.investis-live.com/ctp/6863c5976c0d660016f95b35/kalwt

Ha telefonon szeretne csatlakozni az előadáshoz, kérjük, tárcsázza az alábbi számok egyikét, és adja meg a résztvevői hozzáférési kódot 893972.

Hollandia +31 85 888 7233

Egyesült Királyság +44 20 3936 2999

United States +1 646 664 1960

Nyomja meg a *1-et a kérdés feltevéséhez, a *2-t a kérdés visszavonásához, vagy a *0-t a kezelői segítséghez.

Az előadásról készült felvétel az előadást követő 24 órán belül elérhető lesz a CTP honlapján: https://ctp.eu/investors/financial-results/

CTP PÉNZÜGYI NAPTÁR

| Akció | Dátum |

| Tőkepiaci Napok (Wuppertal, Németország) | 2025. szeptember 24-25 |

| Q3-2025 eredmények | 2025. november 6 |

| 2025-ös pénzügyi év eredményei | 2026. február 26. |

AZ ELEMZŐI ÉS BEFEKTETŐI MEGKERESÉSEK ELÉRHETŐSÉGEI:

Maarten Otte, Head of Investor Relations and Capital Markets

Mobil: +420 730 197 500

E-mail: [email protected]

ELÉRHETŐSÉGEK A MÉDIA MEGKERESÉSÉRE:

E-mail: [email protected]

A CTP-ről

A CTP Európa legnagyobb tőzsdén jegyzett logisztikai és ipari ingatlan tulajdonosa, fejlesztője és kezelője bruttó bérbeadható terület alapján, 2025. június 30-án 13,5 millió négyzetméter bérbeadható területet birtokolva 10 országban. A CTP minden új épületet BREEAM Very good vagy jobb minősítéssel lát el, és a Sustainalytics elhanyagolható kockázatú ESG minősítést kapott, kiemelve elkötelezettségét a fenntartható vállalkozás iránt. További információkért látogasson el a CTP vállalati weboldalára: www.ctp.eu

Felelősségi nyilatkozat

Ez a közlemény bizonyos, a jövőre vonatkozó kijelentéseket tartalmaz a CTP pénzügyi helyzetével, működési eredményeivel és üzleti tevékenységével kapcsolatban. Ezek a jövőre vonatkozó kijelentések azonosíthatók a jövőre vonatkozó terminológia használatával, beleértve a "úgy véli", "becslések", "tervez", "tervez", "tervez", "előrevetít", "várakozik", "szándékozik", "céloz", "lehet", "céloz", "valószínű", "lenne", "lehetne", "lehet", "lehet", "lesz" vagy "kellene" kifejezéseket, illetve minden esetben ezek negatív vagy más változatait vagy hasonló terminológiát. A jövőre vonatkozó kijelentések jelentősen eltérhetnek a tényleges eredményektől, és ez gyakran így is van. Ennek eredményeképpen nem szabad túlzott befolyást gyakorolni egyetlen jövőre vonatkozó kijelentésre sem. Ez a sajtóközlemény a 2014. április 16-i 596/2014/EU rendelet (a piaci visszaélésekről szóló rendelet) 7. cikkének (1) bekezdésében meghatározott bennfentes információkat tartalmaz.

[1] Adjusted for a country mix.

[2] Helyi és EU-27 / eurózóna fogyasztói árindex keverékével, csak korlátozott számú felső határ.

Iratkozz fel a hírlevelünkre

Iratkozz fel hírlevelünkre, hogy megkapd az ipariingatlan-piac vezetőjének legfrissebb elemzéseit.