CTP N.V. Rezultatele T3-2025

VENITURI NETE DIN CHIRIERI ÎN CREȘTERE DE 15,41 TP7 TRIMESTRII FAȚĂ DE LA ANUL PRELIMINAR, CREȘTERE A CHIRIERILOR ÎN PERIOADĂ SIMPLĂ DE 4,51 TP7 TRIMESTRII ȘI EPRA NTA PE ACȚIUNE ÎN CREȘTERE DE 14,01 TP7 TRIMESTRII FAȚĂ DE LA ANUL PRELIMINAR, LA 19,98 €

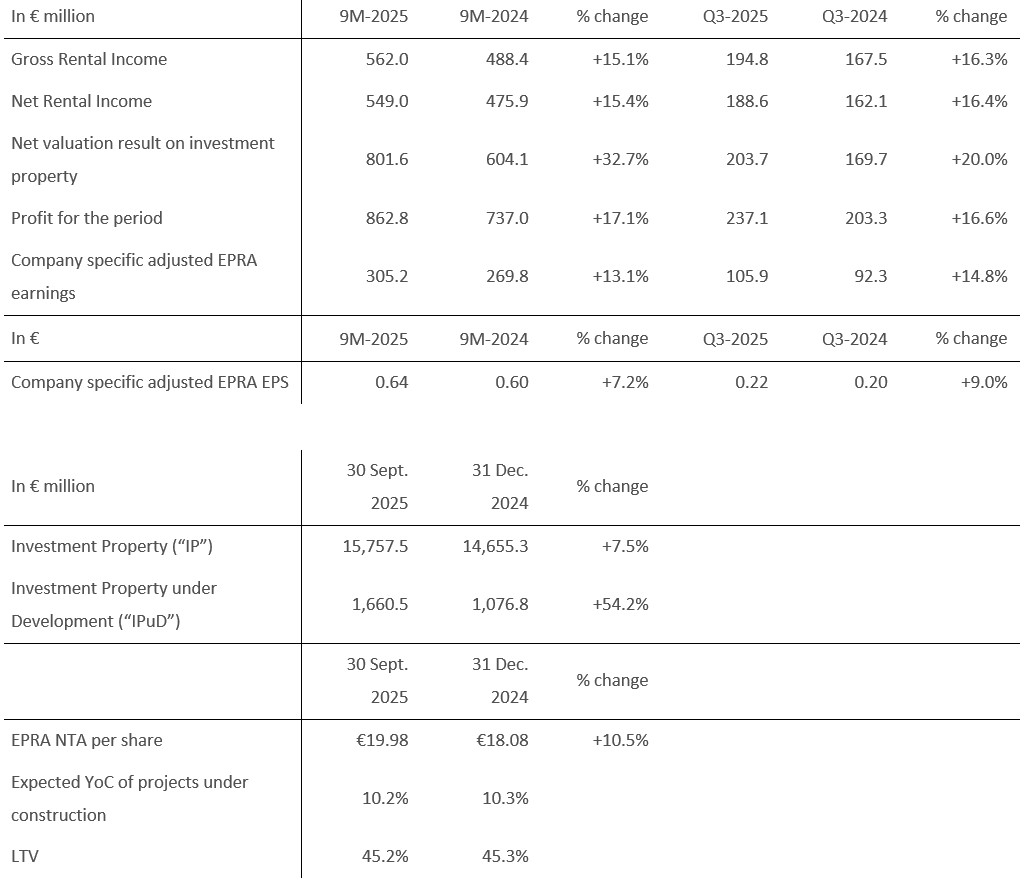

AMSTERDAM, 6 noiembrie 2025 – CTP NV (CTPNV.AS), (“CTP”, “Grupul” sau “Compania”), în primele nouă luni ale anului și-a majorat veniturile brute din chirii cu 15,11 TP7 trilioane de euro față de anul precedent, ajungând la 562 de milioane de euro și a înregistrat o creștere a chiriilor de 4,51 TP7 trilioane de euro față de anul precedent, determinată în principal de indexare și reversarea renegociilor și a contractelor de închiriere care expiră. La 30 septembrie 2025, veniturile anualizate din chirii au crescut la 778 de milioane de euro, în timp ce gradul de ocupare s-a menținut la 931 TP7 trilioane, iar rata de colectare a chiriilor s-a situat la 99,81 TP7 trilioane de euro.

Până în primele nouă luni ale anului 2025, CTP a livrat 553.000 mp la un randament al costului (“YoC”) de 10,3%, care au fost închiriate în total 100% la finalizare, aducând portofoliul actual al Grupului la 13,8 milioane mp de suprafață închiriabilă (GLA). Valoarea brută a activelor (“GAV”) a crescut cu 10,6%, ajungând la 17,7 miliarde EUR și cu 16,0% față de anul precedent. EPRA NTA per acțiune a crescut cu 10,5% în primele nouă luni ale anului 2025, ajungând la 19,98 EUR și cu 14,0% față de anul precedent.

Câștigurile EPRA ajustate specifice companiei au crescut cu 13,11 TP7 trilioane de euro față de anul precedent, ajungând la 305,2 milioane de euro. EPRA EPS ajustat specific companiei al CTP s-a ridicat la 0,64 euro, o creștere de 7,21 TP7 trilioane. Având în vedere că livrările și venitul net din dezvoltare sunt amânate pentru a doua jumătate a anului, Grupul rămâne pe drumul cel bun pentru a atinge previziunile de 0,86 – 0,88 euro pentru 2025, ceea ce reprezintă o creștere de 81 TP7 trilioane – 101 TP7 trilioane de euro față de 2024.

La 30 septembrie 2025, proiectele în construcție totalizau 2,0 milioane mp, cu o rentabilitate anuală estimată de 10,21 milioane de mp, 7 milioane de mp, și un venit potențial din chirii de 165 de milioane de euro după finalizarea închirierii. O parte substanțială a acestor proiecte va fi finalizată în 2025, iar CTP continuă să prevadă o suprafață cuprinsă între 1,3 milioane de mp și 1,6 milioane de mp în acest an.

Rezerva de terenuri a Grupului se ridică la 25,7 milioane mp, din care 22,0 milioane mp sunt deținuți și bilanțiați. Această rezervă de terenuri asigură un potențial substanțial de creștere viitoare pentru CTP, cu 90% situate în jurul parcurilor de afaceri existente (57% în parcuri existente, 33% în parcuri noi cu un potențial de peste 100.000 mp GLA). Combinată cu suprafața sa brută închiriabilă (Your Cost-Contract) de top în industrie, CTP se așteaptă să continue să genereze o creștere de două cifre a veniturilor nete (NTA) în anii următori.

Puterea platformei CTP a fost subliniată în septembrie de upgrade-ul ratingului de credit al S&P de la BBB- la BBB cu o perspectivă stabilă. Upgrade-ul vine după acțiunea Moody's din trimestrul 2 din 2025, prin care perspectiva CTP a fost îmbunătățită de la Stabilă la Pozitivă.

Deținem o suprafață imobiliară de 25,7 milioane mp, cu un profit potențial de dezvoltare de peste 5 miliarde de euro, oferind un potențial semnificativ pentru crearea continuă de valoare. Modelul nostru integrat unic, ca operator, dezvoltator și platformă de creștere, ne oferă capacitatea și flexibilitatea de a capta oportunități, atât pe piețele noastre existente, cât și pe piețele noi potențiale.

”Tendințe structurale precum nearshoring-ul se accelerează, ilustrate de creșterea continuă a chiriașilor din industria prelucrătoare asiatică din portofoliul nostru. În regiunea CEE continuăm să observăm o creștere puternică a consumului intern, în timp ce în Germania beneficiem de modernizarea economiei. Datorită amplorii, calității portofoliului și portofoliului nostru de dezvoltare, CTP este bine poziționată pentru a beneficia de aceste tendințe și a ne atinge ambiția de 30 de milioane de metri pătrați de suprafață închiriabilă în anul 2030.”

Puncte cheie

Cererea continuă și puternică a chiriașilor conduce la creșterea chiriilor

În primele nouă luni ale anului 2025, CTP a semnat contracte de închiriere pentru 1.577.000 mp, o creștere de 61 de mii de trilioane de euro față de aceeași perioadă din 2024, cu o chirie medie lunară pe mp de 5,86 EUR (în primele nouă luni ale anului 2024: 5,63 EUR). Ajustând diferențele dintre mixul de proprietăți din diferite țări, chiriile au crescut în medie cu 61 de mii de trilioane de euro.

| Contracte de închiriere semnate pe mp | Q1 | Q2 | Q3 | YTD | Î4 | FY |

| 2023 | 297,000 | 552,000 | 585,000 | 1,435,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 577,000 | 1,495,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 562,000 | 1,577,000 |

| Chirie medie lunară a contractelor de închiriere semnate pe mp (€) | Q1 | Q2 | Q3 | YTD | Î4 | FY |

| 2023 | 5.31 | 5.56 | 5.77 | 5.60 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.69 | 5.63 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.64 | 5.86 |

În total, 73% contracte de închiriere au fost semnate cu chiriași existenți, în conformitate cu modelul de afaceri al CTP de creștere alături de chiriașii existenți în parcurile existente.

Generarea fluxului de numerar prin portofoliu permanent și achiziții

Cota medie de piață a CTP în Republica Cehă, România, Ungaria și Slovacia a fost de 28,3% la 30 septembrie 2025 și rămâne cel mai mare proprietar și dezvoltator de active imobiliare industriale și logistice pe aceste piețe. Grupul este, de asemenea, lider de piață în Serbia și Bulgaria.

Cu peste 1.500 de clienți, CTP are o bază internațională largă și diversificată de chiriași, formată din companii de top cu ratinguri de credit solide. Chiriașii CTP reprezintă o gamă largă de industrii, inclusiv producție, tehnologie înaltă/IT, industria auto, comerț electronic, comerț cu amănuntul, comerț cu ridicata și companii terțe (3PL). Baza de chiriași este extrem de diversificată, niciun chiriaș nereprezentând mai mult de 2,5% din chiriile anuale ale companiei, ceea ce duce la un flux de venituri stabil. Primii 50 de chiriași ai CTP reprezintă doar 32,7% din chiriile sale, iar marea majoritate a clienților închiriază spații în mai multe CTParks.

Rata de ocupare a companiei rămâne la 93% (anul fiscal 2024: 93%). Rata de retenție a clienților Grupului rămâne puternică la 82% (anul fiscal 2024: 87%) și demonstrează capacitatea CTP de a valorifica relațiile de lungă durată cu clienții. Portofoliul WAULT s-a situat la 6,1 ani (anul fiscal 2024: 6,4 ani), în conformitate cu obiectivul companiei de >6 ani.

Nivelul încasării chiriilor a fost de 99,8% în primele nouă luni ale anului 2025 (anul fiscal 2024: 99,8%), fără o deteriorare a profilului de plată al chiriașilor.

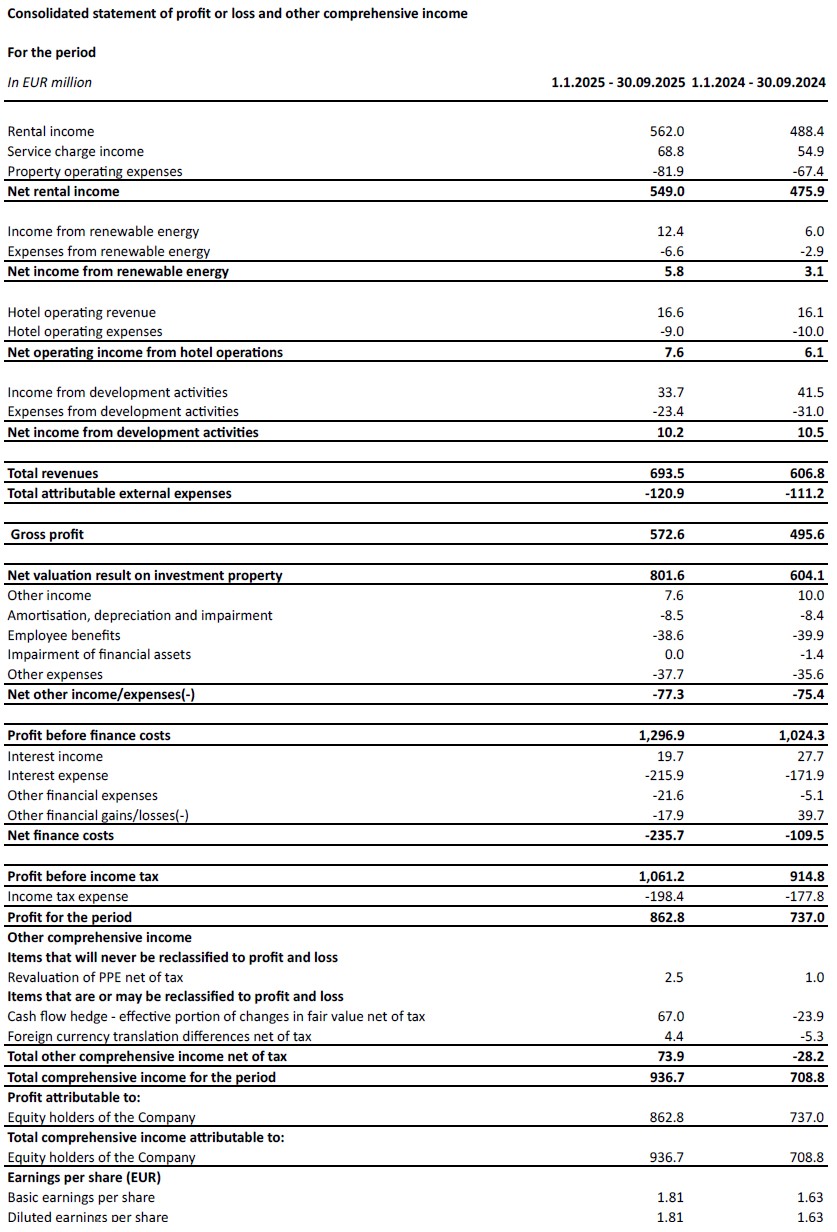

Veniturile din chirii în primele nouă luni ale anului 2025 s-au ridicat la 562 de milioane de euro, în creștere cu 15,11 TP7 trilioane de euro față de anul precedent în termeni absoluți, determinate în principal de livrări și de creșterea pe bază comparabilă. Pe bază comparabilă, veniturile din chirii au crescut cu 4,51 TP7 trilioane de euro, datorită indexării și reversiunii la renegocieri și la expirarea contractelor de închiriere.

Grupul a implementat măsuri pentru a limita pierderile de taxe de serviciu, ceea ce a dus la îmbunătățirea raportului Venituri nete din chirii/Venituri din chirii de la 97,4% în primele nouă luni ale anului 2024 la 97,7% în primele nouă luni ale anului 2025. În consecință, veniturile nete din chirii au crescut cu 15,4% de la an la an.

O proporție tot mai mare din veniturile din chirii generate de portofoliul de investiții al CTP beneficiază de protecție împotriva inflației. De la sfârșitul anului 2019, noile contracte de leasing ale Grupului includ o clauză de indexare în funcție de IPC, care calculează creșterile anuale ale chiriei ca fiind cea mai mare dintre:

- o creștere fixă de 1,5%-2,5% pe an; sau

- indicele prețurilor de consum[1].

La 30 septembrie 2025, 72% din veniturile generate de portofoliul Grupului includ această clauză de dublă indexare, iar Grupul se așteaptă ca aceasta să crească în continuare.

Potențialul de reversie a ajuns la 13,7%. Noi contracte de închiriere au fost semnate în mod constant peste Valoarea de Închiriere Estimată (“VΔ), ilustrând o creștere puternică continuă a chiriilor pe piață și susținând evaluările.

Veniturile anualizate din chirii au ajuns la 778 de milioane de euro la 30 septembrie 2025, o creștere de 10,81 milioane de euro față de anul precedent, demonstrând creșterea puternică a fluxului de numerar al portofoliului de investiții al CTP.

Dezvoltări livrate în perioada 9 luni-2025 cu un contract de închiriere de 10,3% YoC și 100% la livrare

CTP și-a continuat investițiile disciplinate în portofoliul său foarte profitabil.

În primele nouă luni ale anului 2025, Grupul a finalizat o suprafață închiriabilă de 553.000 mp (în primele nouă luni ale anului 2024: 545.000 mp). Dezvoltările au fost livrate la o suprafață închiriabilă anuală de 10,3%, cu o închiriere de 100% și vor genera venituri anuale din chirii contractate de 35,5 milioane de euro. Ca de obicei, livrările din 2025 sunt programate pentru trimestrul al patrulea.

În timp ce costurile medii de construcție în 2022 au fost de aproximativ 550 EUR pe metru pătrat, în 2023 și 2024 acestea au ajuns la 500 EUR pe metru pătrat și au rămas stabile în perioada 9M-2025. Acest lucru permite Grupului să continue să își atingă cifra de afaceri anuală de peste 10%, lider în industrie, susținută și de modelul unic de parc al CTP și de expertiza internă în construcții și achiziții.

La 30 septembrie 2025, Grupul avea în construcție 2,0 milioane mp de clădiri, cu un venit potențial din chirii de 165 milioane EUR și o rată de achiziție imobiliară estimată de 10,2%. CTP are o lungă experiență în generarea unei creșteri durabile prin dezvoltarea condusă de chiriași în parcurile sale existente. 78% dintre proiectele Grupului aflate în construcție se află în parcuri existente, în timp ce 10% sunt în parcuri noi, care au potențialul de a fi dezvoltate până la o suprafață închiriată de peste 100.000 mp. Livrările planificate pentru 2025 reprezintă 63% pre-închiriate, în creștere față de 35% la nivelul anului fiscal 2024. Rata de pre-închiriere în parcurile existente a fost de 58%, în timp ce în parcurile noi cifra pre-închiriatelor a fost de 76%, demonstrând riscul scăzut integrat în proiectele în curs de dezvoltare. CTP se așteaptă să ajungă la o pre-închiriere de 80%-90% la livrare, în conformitate cu performanța istorică. Întrucât CTP acționează ca antreprenor general pe majoritatea piețelor, aceasta deține controlul deplin asupra procesului și a calendarului livrărilor, permițând companiei să accelereze sau să încetinească în funcție de cererea chiriașilor, oferind în același timp chiriașilor flexibilitate în ceea ce privește cerințele lor privind clădirile.

În 2025, Grupul se așteaptă să livreze între 1,3 milioane mp și 1,6 milioane mp, în funcție de cererea chiriașilor. Cei 151.000 mp de contracte de închiriere deja semnate pentru proiecte viitoare — a căror construcție nu a început încă — reprezintă o ilustrare suplimentară a cererii continue din partea ocupanților.

Rezerva funciară a CTP se ridica la 25,7 milioane mp la 30 septembrie 2025 (31 decembrie 2024: 26,4 milioane mp), ceea ce va contribui în mare măsură la atingerea ambiției sale de 30 de milioane mp de suprafață închiriabilă (GLA) până în anul 2030. Grupul se concentrează pe mobilizarea rezervei sale funciare existente, menținând în același timp o alocare disciplinată a capitalului în reaprovizionarea acesteia. 57% din rezerva funciară sunt situate în parcurile existente ale CTP, în timp ce 33% se află în parcuri noi sau sunt adiacente unor parcuri noi, care au potențialul de a crește la peste 100.000 mp. 15% din rezerva funciară au fost garantate prin opțiuni, în timp ce restul de 85% era deținut și reflectat în mod corespunzător în bilanț.

Presupunând un raport de construcție de 2 mp de teren la 1 mp de suprafață închiriabilă (GLA), CTP poate construi aproximativ 13 milioane de mp de GLA pe terenul său securizat. Terenul CTP este deținut în bilanț la aproximativ 60 EUR pe metru pătrat, iar costurile de construcție se ridică în medie la aproximativ 500 EUR pe metru pătrat, ceea ce aduce costurile totale de investiție la aproximativ 620 EUR pe metru pătrat. Portofoliul permanent al Grupului este evaluat la aproximativ 1.040 EUR pe metru pătrat, rezultând un potențial de reevaluare de aproximativ 400 EUR pe metru pătrat construit.

Monetizarea afacerii energetice

CTP își continuă planul de extindere pentru lansarea sistemelor fotovoltaice. Cu un cost mediu de ~750.000 EUR per MWp, Grupul vizează un YoC de 15% pentru aceste investiții.

CTP are o capacitate fotovoltaică instalată de 149 MWp, din care 123,5 MWp sunt complet operaționale.

În primele nouă luni ale anului 2025, veniturile din energia regenerabilă au fost de 12,4 milioane de euro, în creștere cu 1.081 milioane de euro și 7 milioane de euro față de anul precedent, determinată în principal de creșterea capacității instalate pe parcursul anului 2024.

Ambițiile de sustenabilitate ale CTP merg mână în mână cu un număr tot mai mare de chiriași care solicită energie verde din sistemele fotovoltaice, deoarece acestea le oferă i) o securitate energetică îmbunătățită, ii) un cost de ocupare mai mic, iii) respectarea reglementărilor sporite, iv) respectarea cerințelor clienților lor și v) capacitatea de a-și îndeplini propriile ambiții ESG.

Rezultatele evaluării sunt determinate de pipeline și de reevaluarea pozitivă a portofoliului actual

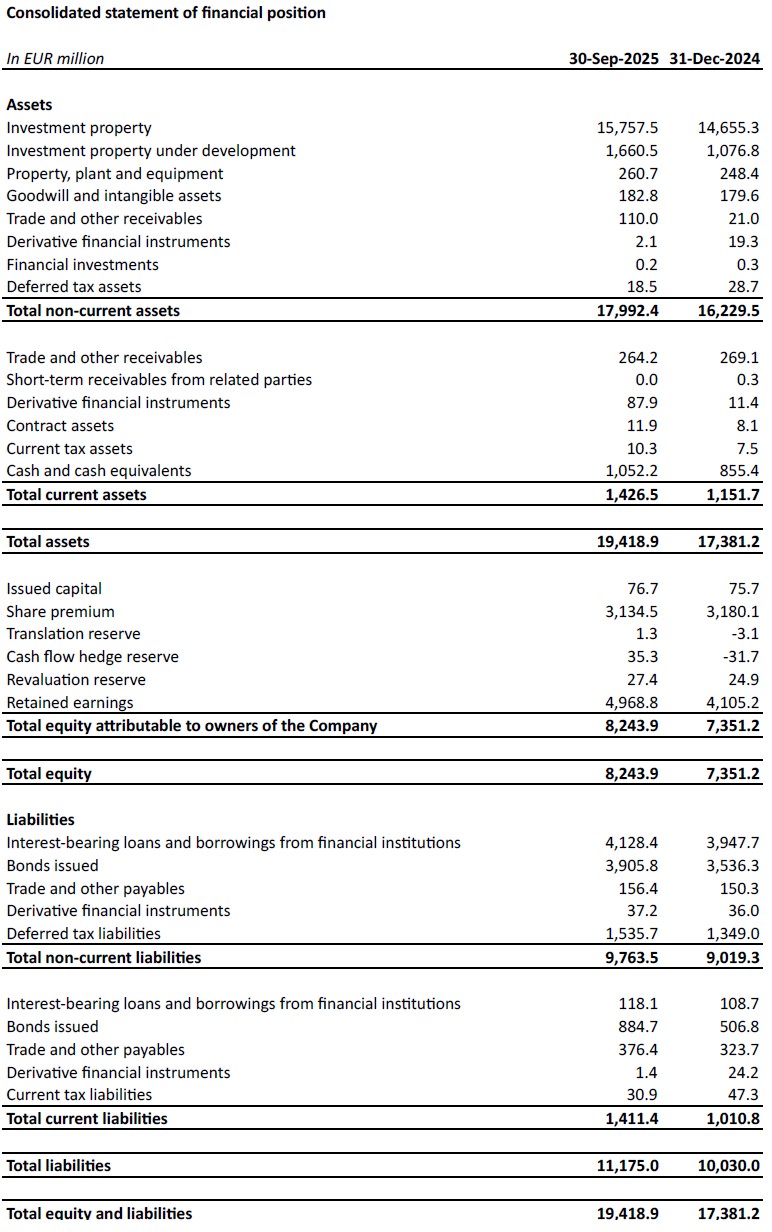

Evaluarea proprietăților imobiliare în curs de dezvoltare (“IP”) a crescut de la 14,7 miliarde EUR la 31 decembrie 2024 la 15,8 miliarde EUR la 30 septembrie 2025, determinată de transferul proiectelor finalizate de la proprietăți imobiliare în curs de dezvoltare (“IPuD”) la IP și de reevaluarea pozitivă a portofoliului în curs de dezvoltare.

Cheltuielile de capital (IPuD) au crescut cu 54,2% față de 31 decembrie 2024, ajungând la 1,7 miliarde EUR la 30 septembrie 2025, determinate de cheltuielile de capital, reevaluarea datorată creșterii pre-închirierilor și progresului în construcții și începerea de noi proiecte de construcții în perioada 9M-2025.

VAB-ul a crescut la 17,7 miliarde de euro la 30 septembrie 2025, în creștere cu 10,61 miliarde de euro și 7 miliarde de euro față de 31 decembrie 2024.

Pentru rezultatele din T1 și T3, doar proiectele IPuD sunt reevaluate. Reevaluarea în primele nouă luni ale anului 2025 a fost de 801,6 milioane EUR, determinată de reevaluarea pozitivă a proiectelor IPuD (+385,2 milioane EUR), a activelor imobiliare (+43,3 milioane EUR) și a activelor imobiliare (+373,0 milioane EUR).

CTP anticipează o creștere pozitivă în continuare a ERV-ului pe fondul cererii continue din partea chiriașilor, care este influențată pozitiv de factorii de creștere seculară din regiunea CEE. Nivelurile chiriilor din CEE rămân accesibile, în ciuda creșterii puternice observate, deoarece acestea au pornit de la niveluri absolute semnificativ mai mici decât în țările din Europa de Vest. În termeni reali, chiriile pe multe piețe din Europa Centrală și de Est (“CEE”) sunt încă sub nivelurile din 2010.

Portofoliul Grupului are randamente conservatoare de evaluare de 7,0%. Se preconizează că diferența de randament dintre logistica din Europa Centrală și de Est (ECE) și cea din Europa de Vest va scădea în timp, determinată de așteptările de creștere mai mari pentru regiunea ECE și de activitatea tot mai intensă pe piețele de investiții.

EPRA NTA per acțiune a crescut de la 18,08 EUR la 31 decembrie 2024 la 19,98 EUR la 30 septembrie 2025, reprezentând o creștere de 10,5% până la sfârșitul primelor 9 luni din 2025 și o creștere de 14,0% față de anul precedent. Creșterea este determinată în principal de reevaluare (+1,67 EUR), de EPRA EPS ajustat specific companiei (+0,64 EUR) și compensată de dividendul final din 2024 plătit în mai (-0,30 EUR) și de alte elemente (-0,11 EUR).

Bilanț robust și poziție solidă de lichiditate

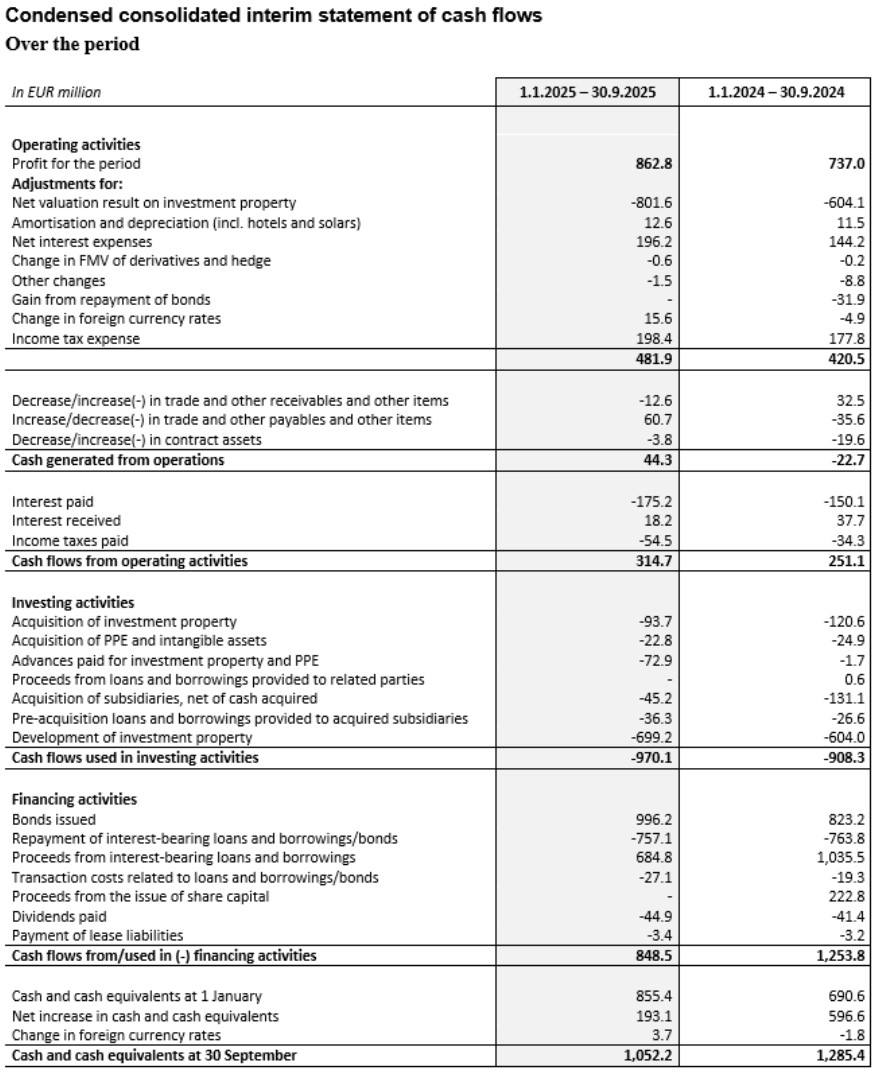

În conformitate cu abordarea sa proactivă și prudentă, Grupul beneficiază de o poziție solidă de lichiditate pentru a-și finanța ambițiile de creștere, cu un cost fix al datoriei și un profil de rambursare conservator.

În perioada dintre primele nouă luni ale anului 2025, Grupul a obținut 1,7 miliarde de euro pentru a-și finanța creșterea organică:

- O obligațiune verde de 1,0 miliard de euro, cu tranșe duble, cu o tranșă de 500 de milioane de euro pe șase ani la MS +145 puncte de bază și un cupon de 3,625% și o tranșă de 500 de milioane de euro pe zece ani la MS +188 puncte de bază și un cupon de 4,25%;

- O facilitate de credit negarantată pe cinci ani în valoare de 30 de miliarde JPY (echivalentul a 185 de milioane EUR) cu un sindicat de bănci asiatice, la TONAR +130 puncte de bază și un cost fix total de 4,1%; și

- O facilitate de credit negarantată, legată de sustenabilitate, în valoare de 500 de milioane de euro, pe cinci ani, cu un sindicat de 13 bănci europene și asiatice, la un cost fix total de 3,71 TP7T.

În plus, pe 13 octombrie 2025, CTP a emis o nouă obligațiune verde de 600 de milioane de euro, pe 6,5 ani, la un MS +118 puncte de bază și un cupon de 3,625%.

CTP a continuat să își gestioneze activ portofoliul de credite bancare în perioada 19-2025. A fost negociată o reducere a marjei pentru încă 193 de milioane de euro reprezentând credite bancare garantate, iar un credit pe termen negarantat în valoare de 441 de milioane de euro, semnat în 2023, a fost rambursat în avans și refinanțat prin noul credit negarantat de 500 de milioane de euro. Ambele aspecte au permis CTP să realizeze economii semnificative la rata dobânzii, reducând costul total al datoriei pe viitor.

Poziția de lichiditate a Grupului s-a ridicat la 2,4 miliarde de euro, compusă din 1,1 miliarde de euro în numerar și echivalente de numerar și un RCF neutilizat de 1,3 miliarde de euro.

Costul mediu al datoriei CTP a fost de 3,2% (anul fiscal 2024: 3,1%), în ușoară creștere față de sfârșitul anului 2024, datorită finanțării noi. 99,9% din datorie este cu rată fixă sau acoperită împotriva dobânzii până la scadență.

Grupul nu capitalizează dobânzile aferente dezvoltărilor, prin urmare, toate cheltuielile cu dobânzile sunt incluse în contul de profit și pierdere. Maturitatea medie a datoriei a fost de 4,8 ani (anul fiscal 2024: 5,0 ani).

Grupul a rambursat o obligațiune în valoare de 272 de milioane de euro în iunie 2025 din rezervele sale de numerar disponibile. O altă obligațiune în valoare de 185 de milioane de euro era scadentă în octombrie 2025, de asemenea rambursată din rezervele de numerar.

Valoarea LTV a CTP a fost de 45,2% la 30 septembrie 2025, influențată pozitiv de reevaluarea puternică a proprietăților de investiții în curs de dezvoltare.

Activele cu randament mai mare ale Grupului, datorită randamentului brut al portofoliului de 6,6%, conduc la un nivel sănătos al efectului de levier al fluxului de numerar, care se reflectă și în raportul datorie netă normalizată/EBITDA de 9,2x (anul fiscal 2024: 9,1x), pe care Grupul își propune să îl mențină sub 10x.

Datoria Grupului era formată din 68% datorii negarantate și 32% datorii garantate la 30 septembrie 2025, cu o marjă de manevră amplă în temeiul clauzelor privind Testul Datoriilor Garantate și Testul Activelor Negarantate.

Pe măsură ce prețurile de pe piața obligațiunilor s-au raționalizat, condițiile sunt acum mai competitive decât prețurile de pe piața de creditare bancară, ceea ce va permite Grupului să se reechilibreze mai mult față de creditarea negarantată.

| 30 septembrie 2025 | Pact | |

| Testul privind datoriile garantate | 14.9% | 40% |

| Testul activelor libere de sarcini | 190.6% | 125% |

| Rata de acoperire a dobânzii | 2,5x | 1.5x |

În trimestrul 3 din 2025, S&P a îmbunătățit ratingul de credit al CTP de la BBB- la BBB cu perspectivă stabilă. În ianuarie 2025, agenția japoneză de rating JCR a acordat CTP un rating de credit A- cu perspectivă stabilă. În trimestrul 2 din 2025, Moody's a îmbunătățit perspectiva ratingului de credit Baa3 de la stabilă la pozitivă.

Îndrumare

Dinamica închirierilor rămâne puternică, cu o cerere robustă din partea ocupanților și o ofertă nouă în scădere, ceea ce duce la o creștere continuă a chiriilor. CTP este bine poziționată pentru a beneficia de aceste tendințe. Portofoliul Grupului este extrem de profitabil și condus de chiriași. Valoarea anuală a costurilor (Your Cost) pentru portofoliul actual al CTP se menține la un nivel lider în industrie de 10,21 milioane de mp, 7 milioane de mp. Următoarea etapă de creștere este construită și finanțată, cu 2,0 milioane de mp în construcție la 30 septembrie 2025, cu o țintă de a livra între 1,3 milioane de mp și 1,6 milioane de mp în 2025 și încă 1,4 milioane de mp și 1,7 milioane de mp în 2026.

Structura robustă de capital a CTP, politica financiară disciplinată, accesul solid la piața creditelor, banca funciară lider în industrie, expertiza internă în construcții și relațiile solide cu chiriașii permit CTP să își îndeplinească obiectivele. CTP se așteaptă să atingă venituri din chirii de 1,0 miliard de euro în 2027, impulsionate de finalizările dezvoltărilor, indexare și reversare. De asemenea, este pe cale să își atingă ambiția de 30 de milioane de metri pătrați de suprafață închiriabilă până în anul 2030.

Grupul confirmă previziunile EPRA EPS ajustate specifice companiei, de 0,86 € – 0,88 €, care, din cauza faptului că achiziția preconizată din România nu a avut loc, sunt acum așteptate să se îndrepte spre limita inferioară a intervalului. Creșterea EPRA EPS este determinată de o creștere puternică subiacentă, cu o creștere a chiriilor de aproximativ 4% la performanță comparabilă, compensată parțial de costul mediu mai mare al datoriei, datorat (re)finanțării din 2024 și 2025. Grupul se așteaptă să revină la o creștere de două cifre a EPRA EPS în 2026.

Politica de dividende a CTP este de a plăti între 70% și 80% din EPRA EPS ajustat specific companiei. Implicit, dividendul este un dividend pe acțiuni, dar acționarii pot opta pentru plata dividendului în numerar.

WEBCAST ȘI CONFERINȚĂ TELEFONICĂ PENTRU ANALIȘTI ȘI INVESTITORI

Astăzi, la ora 9.00 (GMT) și 10.00 (CET), compania va găzdui o prezentare video și o sesiune de întrebări și răspunsuri pentru analiști și investitori, prin intermediul unei transmisiuni în direct pe internet și al unei conferințe telefonice audio.

Pentru a viziona transmisiunea în direct pe internet, vă rugăm să vă înregistrați în avans la:

https://www.investis-live.com/ctp/68dce560eefece00147ba94d/vbqpg

Pentru a participa la prezentare prin telefon, vă rugăm să formați unul dintre următoarele numere și să introduceți codul de acces al participantului 128602.

Germania +49 32 22109 8334

Franța +33 9 70 73 39 58

Olanda +31 85 888 7233

Regatul Unit +44 20 3936 2999

Statele Unite +1 646 664 1960

Apăsați *1 pentru a pune o întrebare, *2 pentru a vă retrage întrebarea sau *0 pentru asistență din partea operatorului.

O înregistrare va fi disponibilă pe site-ul CTP în termen de 24 de ore de la prezentare: https://ctp.eu/investors/financial-results/

CALENDARUL FINANCIAR AL CTP

| Acțiune | Data |

| Rezultatele anului fiscal 2025 | 26 februarie 2026 |

| Rezultate T1-2026 | 30 aprilie 2026 |

| Adunarea generală anuală | 20 mai 2026 |

| Rezultate semestrul 1-2026 | 30 iulie 2026 |

| Zilele pieței de capital | Septembrie 2026 |

| Rezultate T3-2026 | 29 octombrie 2026 |

DATE DE CONTACT PENTRU SOLICITĂRI ALE ANALISTILOR ȘI INVESTITORILOR:

Maarten Otte, Șeful Relațiilor cu Investitorii și Piețelor de Capital

Mobil: +420 730 197 500

E-mail: [email protected]

Pavel Švihálek, manager de finanțare și IR

Mobil: +420 724 928 828

Email: [email protected]

CONTACT PENTRU PRESĂ:

Email: [email protected]

Despre CTP

CTP este cel mai mare proprietar, dezvoltator și administrator de proprietăți imobiliare logistice și industriale listate la bursă din Europa, după suprafața brută închiriabilă, deținând 13,8 milioane mp de GLA în 10 țări la 30 septembrie 2025. CTP certifică toate clădirile noi conform BREEAM Foarte bine sau mai bine și a obținut un rating ESG de risc neglijabil din partea Sustainalytics, subliniind angajamentul său de a fi o afacere sustenabilă. Pentru mai multe informații, vizitați site-ul web corporativ al CTP: www.ctp.eu

Disclaimer

Acest anunț conține anumite declarații cu caracter prospectiv cu privire la situația financiară, rezultatele operațiunilor și activitatea CTP. Aceste declarații anticipative pot fi identificate prin utilizarea terminologiei anticipative, inclusiv a termenilor "crede", "estimează", "planifică", "proiectează", "anticipează", "se așteaptă", "intenționează", "țintește", "poate", "urmărește", "probabil", "ar putea", "ar putea", "ar putea avea", "va avea" sau "ar trebui" sau, în fiecare caz, forma negativă a acestora sau alte variante sau terminologie comparabilă. Declarațiile prospective pot să difere și deseori diferă în mod semnificativ de rezultatele reale. Prin urmare, nu trebuie să se acorde o influență nejustificată niciunei declarații prospective. Acest comunicat de presă conține informații privilegiate, astfel cum sunt definite la articolul 7 alineatul (1) din Regulamentul (UE) 596/2014 din 16 aprilie 2014 (Regulamentul privind abuzul de piață).

[1] Cu o combinație de IPC local și UE-27/zona euro, doar un număr limitat de plafoane.

Înscrieți-vă la newsletter-ul nostru

Primește cele mai recente informații de la liderul pieței imobiliare industriale direct în căsuța ta poștală.