Výsledky CTP NV Q3-2024

CTP HLÁSÍ ČISTÝ VÝJEM Z PRONÁJMU 18,21 TP3T MEZIROČNĚ, SPOLEČNOST SPECIFICKÝ UPRAVENÝ EPRA EPS VE VÝŠE 0,60 EUR NA TRATE K DOSAŽENÍ NÁVODU A EPRA NTA NA AKCIU AŽ 10,11 TP3T NA 17,52 EUR

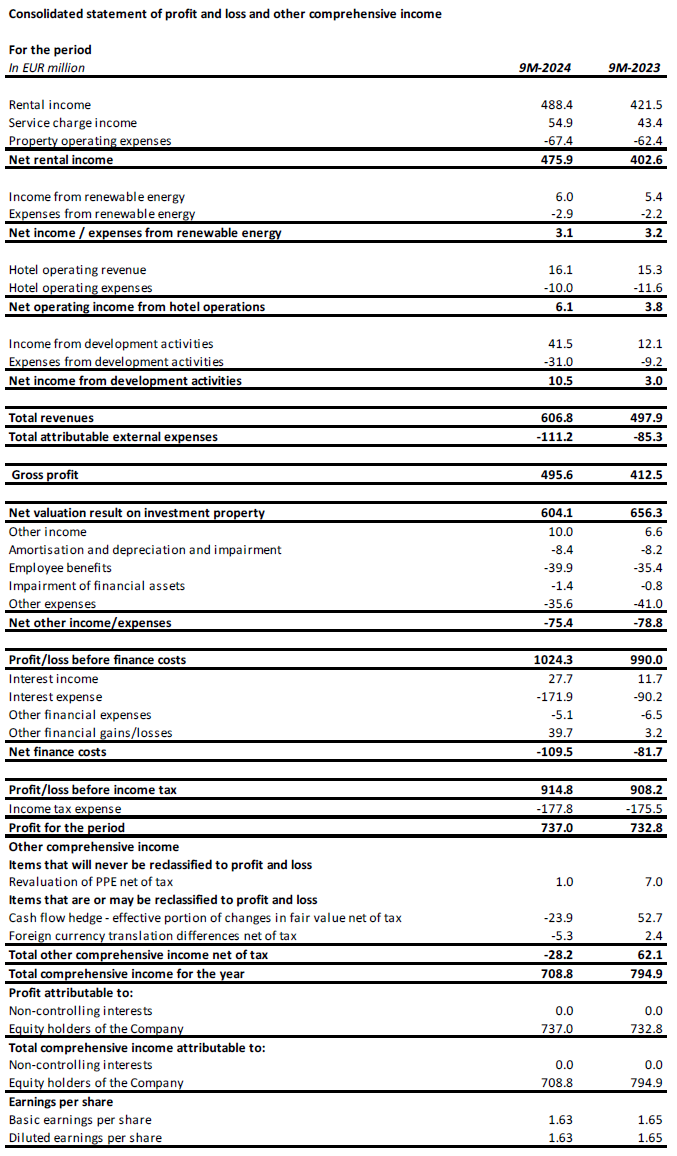

AMSTERDAM, 6. listopadu 2024 – CTP NV (CTPNV.AS), („CTP“, „Skupina“ nebo „Společnost“) zaznamenala v prvních 9 měsících roku příjem z pronájmu ve výši 488,4 milionu EUR, meziročně o 15,91 TP3T více. Stejný meziroční růst nájemného o 4,41 TP3T, zejména díky indexaci a reverzi při renegociacích a končících leasingech. K 30. září 2024 dosáhl roční příjem z pronájmu 702,0 milionů a obsazenost dosáhla 93%.

Za prvních 9 měsíců dodala CTP 545 000 m2 při výnosu z nákladů („YoC“) 10,1% a 95% pronájmu po dokončení, čímž se stálé portfolio skupiny zvýšilo na 12,6 milionu m2 GLA, zatímco hrubá hodnota aktiv („GAV“ ) vzrostl o 11,81 TP3T na 15,2 miliardy EUR. EPRA NTA na akcii se v první polovině roku zvýšil o 10,11 TP3T na 17,52 EUR.

Upravený zisk EPRA pro jednotlivé společnosti se meziročně zvýšil o 13,21 TP3T na 269,8 milionu EUR. Specifický upravený EPRA EPS CTP společnosti CTP činil 0,60 EUR, což je nárůst o 11,71 TP3T. Skupina potvrzuje své doporučení EPRA EPS pro rok 2024 pro konkrétní společnost upravené ve výši 0,80 – 0,82 EUR.

K 30. září 2024 měly projekty ve výstavbě celkem 1,9 milionu m2 s potenciálním příjmem z pronájmu 142 milionů EUR při plném pronájmu a očekávaným YoC 10,41 TP3T. Z toho podstatná část bude dodána v roce 2024, protože CTP letos očekává dodávku mezi 1,2 – 1,3 milionu m2.

Pozemková banka skupiny vzrostla na 27,1 milionu m2, z čehož 20,9 milionu m2 je ve vlastnictví a v rozvaze, a zajistila společnosti CTP značný budoucí růstový potenciál. CTP očekává, že díky svému nejlepšímu YoC v oboru bude v nadcházejících letech nadále generovat dvouciferný růst NTA.

Anualizovaný příjem z pronájmu činil 702 milionů EUR, což ilustruje silný peněžní tok našeho stálého portfolia s mírou inkasa nájemného 99,81 TP3T. Zatímco další fáze růstu je již uzavřena s našimi 1,9 milionu m2 GLA ve výstavbě a pozemkem o rozloze více než 27 milionů m2, budeme i nadále generovat dvouciferný růst NTA. Kromě předpronájmu stávajícího plynovodu jsme měli podepsaných dalších 177 000 m2 nájemních smluv na budoucí projekty, jejichž spuštění plánujeme v nejbližší době.

Poptávka po průmyslových a logistických nemovitostech v regionu CEE je poháněna strukturálními hnacími silami poptávky, jako je profesionalizace dodavatelských řetězců prostřednictvím 3PL, e-commerce a nearshoring a friend-shoring, protože region CEE nabízí nejnákladnější umístění v Evropě. Nyní máme více než 101 TP3T našeho portfolia pronajatých asijským nájemcům, kteří vyrábějí v Evropě pro Evropu, což představuje přibližně 201 TP3T naší celkové leasingové aktivity v roce 2024.“

Klíčové informace

| V milionech EUR | 9M-2024 | 9M-2023 | Změna % | 3. čtvrtletí 2024 | Q3-2023 | Změna % |

| Hrubý příjem z pronájmu | 488.4 | 421.5 | +15.9% | 167.5 | 141.1 | +18.8% |

| Čistý příjem z pronájmu | 475.9 | 402.6 | +18.2% | 162.1 | 134.1 | +20.8% |

| Čistý výsledek ocenění investic do nemovitostí | 604.1 | 656.3 | -8.0% | 167.4 | 239.1 | -30.0% |

| Zisk za období | 737.0 | 732.8 | +0.6% | 203.3 | 263.1 | -22.7% |

| Upravený zisk EPRA podle jednotlivých společností | 269.8 | 238.4 | +13.2% | 92.3 | 80.4 | +14.8% |

| V € | 9M-2024 | 9M-2023 | Změna % | 3. čtvrtletí 2024 | Q3-2023 | Změna % |

| Upravený zisk na akcii EPRA pro jednotlivé společnosti | 0.60 | 0.54 | +11.7% | 0.20 | 0.18 | +12.7% |

| V milionech EUR | 30. září 2024 | 31. prosince 2023 |

Změna % | |||

| Investice do nemovitostí ("IP") | 13,378.5 | 12,039.2 | +11.1% | |||

| Investice do nemovitostí ve výstavbě ("IPuD") | 1,616.4 | 1,359.6 | +18.9% | |||

| 30. září 2024 | 31. prosince 2023 |

Změna % | ||||

| EPRA NTA na akcii | €17.52 | €15.92 | +10.1% | |||

| Očekávaný roční obrat projektů ve výstavbě | 10.4% | 10.3% | ||||

| LTV | 44.9% | 46.0% |

Pokračující silná poptávka nájemců pohání růst nájemného

Během prvních 9 měsíců roku 2024 CTP podepsala nájemní smlouvy na 1 495 000 m2, což je nárůst o 4% ve srovnání s 9M-2023, se smluvním ročním příjmem z pronájmu ve výši 100,9 milionu EUR a průměrným měsíčním nájemným za m2 ve výši 5,63 EUR (9M-2023: 5,60 €). Po očištění o rozdíl v mixu zemí vzrostlo nájemné v průměru o 3%.

| Podepsané nájemní smlouvy podle m2 | Q1 | Q2 | Q3 | YTD | Q4 | FY |

| 2022 | 441,000 | 452,000 | 505,000 | 1,398,000 | 485,000 | 1,883,000 |

| 2023 | 297,000 | 552,000 | 585,000 | 1,435,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 577,000 | 1,495,000 |

| Průměrné měsíční nájemné za metr čtvereční (€) | Q1 | Q2 | Q3 | YTD | Q4 | FY |

| 2022 | 4.87 | 4.89 | 4.75 | 4.82 | 4.80 | 4.82 |

| 2023 | 5.31 | 5.56 | 5.77 | 5.60 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.69 | 5.63 |

Přibližně dvě třetiny těchto pronájmů byly uzavřeny se stávajícími nájemci, což je v souladu s obchodním modelem společnosti CTP, který spočívá v růstu se stávajícími nájemci ve stávajících parcích.

Generování cashflow prostřednictvím stálého portfolia a akvizic

Průměrný tržní podíl CTP v České republice, Rumunsku, Maďarsku a na Slovensku se k 30. září 2024 zvýšil na 28,51 TP3T a zůstává největším vlastníkem a developerem průmyslových a logistických nemovitostí na těchto trzích. Skupina je rovněž lídrem na trhu v Srbsku a Bulharsku.

S více než 1 000 klienty má CTP širokou a diverzifikovanou mezinárodní základnu nájemců, kterou tvoří špičkové společnosti se silným úvěrovým ratingem. Nájemci CTP zastupují širokou škálu průmyslových odvětví, včetně výroby, high-tech/IT, automobilového průmyslu, elektronického obchodu, maloobchodu, velkoobchodu a logistiky třetích stran. Základna nájemců je vysoce diverzifikovaná, přičemž žádný jediný nájemce nepředstavuje více než 2,51 TP3T ročního nájemného, což vede ke stabilnímu toku příjmů. Na 50 nejlepších nájemců CTP připadá pouze 33,41 TP3T z jeho nájemného a většina je v několika CTParcích.

Obsazenost společnosti dosáhla 93% (3. čtvrtletí 2023: 93%). Míra udržení klientů skupiny zůstává silná na 91% (Q3-2023: 92%) a demonstruje schopnost CTP využít dlouhodobé vztahy s klienty. Portfolio WAULT dosáhlo 6,5 roku (Q3-2023: 6,6 roku), což je v souladu s cílem Společnosti >6 let.

Úroveň inkasa nájemného činila 99,81 TP3T v 9M-2024 (9M-2023: 99,8%), bez zhoršení platebního profilu nájemců.

Příjem z pronájmu dosáhl 488,4 milionu EUR, meziročně o 15,91 TP3T absolutně více. Na stejném základě vzrostly příjmy z pronájmu o 4,41 TP3T, zejména díky indexaci a reverzi při renegociacích a končících leasingech.

Skupina zavedla opatření k omezení úniku servisních poplatků, což vedlo ke zlepšení poměru čistého příjmu z pronájmu k příjmu z pronájmu z 95,51 TP3T v 9. měsíci 2023 na 97,41 TP3T v 9. měsíci 2024. V důsledku toho se čistý příjem z pronájmu meziročně zvýšil o 18,21 TP3T.

Stále větší část výnosů z pronájmu investičního portfolia společnosti CTP je chráněna proti inflaci. Od konce roku 2019 obsahují všechny nové nájemní smlouvy skupiny doložku o dvojí indexaci, která vypočítává roční nárůst nájemného jako vyšší z těchto hodnot:

- fixní zvýšení o 1,5%-2,5% ročně; nebo

- index spotřebitelských cen[1].

K 30. září 2024 zahrnuje 70% výnosů generovaných portfoliem Skupiny tuto doložku o dvojité indexaci a Skupina očekává, že se bude dále zvyšovat.

Reverzní potenciál zůstal stabilní na 15,1%. Nové nájemní smlouvy byly průběžně podepisovány nad ERV, což ilustruje pokračující silný růst tržního nájemného a podporuje ocenění.

Anualizovaný příjem z pronájmu dosáhl k 30. září 2024 výše 702,0 milionů EUR, což je meziroční nárůst o 19,31 TP3T, což ukazuje na silný růst peněžních toků investičního portfolia CTP.

Vývoj 9M-2024 dodán s 10.1% YoC a 95% při dodání

CTP pokračovala v disciplinovaných investicích do svého vysoce ziskového potrubí. Za prvních 9 měsíců Skupina dokončila 545 000 m2 GLA (9M-2023: 566 000 m2), což je o něco méně než loni, kdy bylo online několik projektů, které byly v průběhu roku 2022 odloženy kvůli vyšším stavebním nákladům. Projekty byly dodány za rok 10,11 TP3T, 951 TP3T let a budou generovat nasmlouvaný roční příjem z pronájmu ve výši 33,0 milionů EUR, s dalšími 2,0 miliony EUR očekávaného příjmu, až budou plně obsazeny.

Některé z hlavních dodávek během prvních 9 měsíců roku 2024 byly: 169 000 m2 v CTPark Warsaw West (Polsko), 48 000 m2 v CTPark Zabrze (Polsko), 37 000 m2 v CTPark Budapest Ecser (Maďarsko), 37 000 m2 v East Sadi Sadi mq (Srbsko), 30 000 m2 v CTPark Weiden (Německo), 26 000 m2 v CTPark Bucharest West (Rumunsko), 27 000 m2 v CTPark Katowice (Polsko) a 23 000 m2 v CTPark Arad West (Rumunsko).

Zatímco průměrné stavební náklady v roce 2022 byly kolem 550 EUR na m2, v letech 2023 a 9M-2024 dosáhly 500 EUR na m2. CTP očekává, že se na této úrovni udrží do roku 2024. Skupině to umožní pokračovat v poskytování svého nejlepšího ukazatele indexu (YC) nad 10%, což je také podporováno jedinečným modelem parku CTP a vlastními odbornými znalostmi v oblasti výstavby a nákupu.

K 30. září 2024 měla Skupina ve výstavbě 1,9 milionu m2 budov s potenciálním příjmem z pronájmu ve výši 142 milionů EUR a očekávaným YoC 10,41 TP3T. CTP má dlouhou historii v zajišťování udržitelného růstu prostřednictvím vývoje ve svých stávajících parcích vedeného nájemci. 76% z projektů Skupiny ve výstavbě je ve stávajících parcích, zatímco 15% je v nových parcích, které mají potenciál být rozvinuty na více než 100 000 m2 GLA. Plánované dodávky v roce 2024 jsou předpronajaté 64%. CTP očekává, že při dodání dosáhne předpronájmu 80%-90% v souladu s historickou výkonností. Vzhledem k tomu, že CTP působí na většině trhů jako generální dodavatel, má plně pod kontrolou proces a načasování dodávek, což umožňuje společnosti zrychlit nebo zpomalit v závislosti na poptávce nájemců a zároveň nabídnout nájemcům flexibilitu z hlediska požadavků budovy.

V roce 2024 Skupina očekává dodání 1,2 – 1,3 milionu m2 v závislosti na poptávce nájemců. 177 000 m2 nájemních smluv, které jsou v současné době podepsány pro budoucí projekty, jejichž výstavba ještě nezačala, je dalším příkladem pokračující poptávky ze strany nájemců.

Plocha pozemků CTP k 30. září 2024 činila 27,1 milionu m2 (31. prosince 2023: 23,4 milionu m2), což umožňuje Společnosti dosáhnout cíle 20 milionů m2 GLA do konce desetiletí. Skupina se zaměřuje na mobilizaci stávajícího pozemkového fondu při zachování disciplinované alokace kapitálu při doplňování pozemkového fondu. 60% landbanku se nachází ve stávajících parcích CTP, zatímco 30% je v nových parcích nebo s nimi sousedí, které mají potenciál narůst na více než 100 000 m2. 23% pozemkové banky bylo zajištěno opcemi, zatímco zbývajících 77% bylo ve vlastnictví a odpovídajícím způsobem se promítlo do rozvahy.

Za předpokladu poměru zástavby 2 m2 pozemku k 1 m2 GLA může CTP na svém zabezpečeném pozemku vybudovat přes 13 milionů m2 GLA. Pozemky CTP jsou drženy v rozvaze za přibližně 50 EUR za m2 a stavební náklady dosahují v průměru přibližně 500 EUR za m2, čímž celkové investiční náklady dosahují přibližně 600 EUR na m2. Stálé portfolio skupiny, vyjma staršího bývalého portfolia Deutsche Industrie REIT, má hodnotu kolem 1 000 EUR za m2.

Monetizace energetického byznysu

CTP pokračuje ve svém plánu expanze pro zavádění fotovoltaických systémů. S průměrnými náklady ~ 750 000 EUR na MWp skupina u těchto investic cílí na YoC 151 TP3T.

Během prvních 9 měsíců Skupina nainstalovala na střechu dalších 19 MWp, které jsou v současné době připojovány k síti. Celkový instalovaný výkon nyní činí 119 MWp.

V 9M-2024 dosáhly výnosy z obnovitelné energie 6,0 milionů EUR, meziročně o 101 TP3T více.

Ambice společnosti CTP v oblasti udržitelnosti jdou ruku v ruce s tím, že stále více nájemců požaduje fotovoltaické systémy, protože jim poskytují i) lepší energetickou bezpečnost, ii) nižší náklady na užívání, iii) soulad se zvýšenou regulací, iv) soulad s požadavky jejich klientů a v) možnost naplnit jejich vlastní ambice v oblasti ESG.

Výsledky ocenění tažené portfoliem a pozitivním přeceněním stálého portfolia

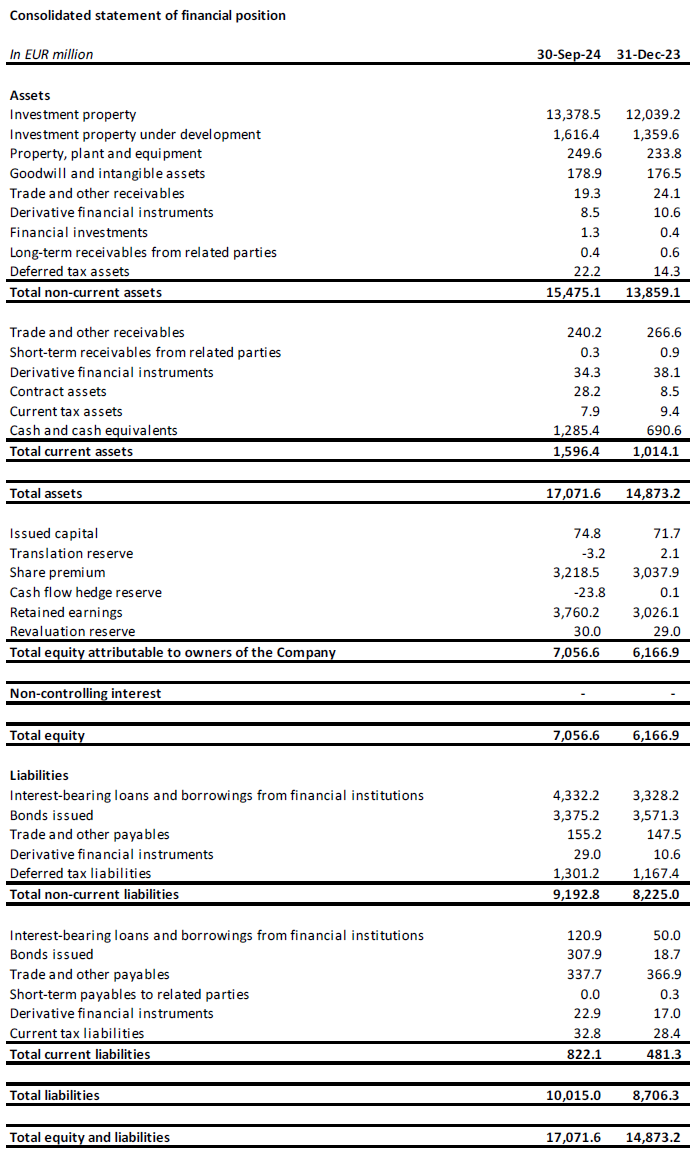

Ocenění investičních nemovitostí („IP“) se zvýšilo z 12,0 miliardy EUR k 31. prosinci 2023 na 13,4 miliardy EUR k 30. září 2024, zejména díky převodu dokončených projektů z investičního majetku ve výstavbě („IPuD“) do IP, přírůstkové akvizice a kladné přecenění.

IPuD se k 30. září 2024 zvýšil o 18,91 TP3T na 1,6 miliardy EUR, což je způsobeno pokrokem ve vývoji, přičemž většina projektů bude jako obvykle dodána ve čtvrtém čtvrtletí roku.

GAV se k 30. září 2024 zvýšila na 15,2 miliardy EUR, což je o 11,81 TP3T více než k 31. prosinci 2023.

U výsledků za 1. a 3. čtvrtletí se přeceňují pouze projekty IPuD. Přecenění za 3. čtvrtletí 2024 bylo 167,4 milionu EUR, což znamená, že přecenění za prvních 9 měsíců dosáhlo 604,1 milionu EUR, taženo kladným přeceněním projektů IPuD (+351,2 milionu EUR), landbank (+26,1 milionu EUR) a postavením aktiva (+226,9 milionů EUR).

Portfolio Skupiny má konzervativní výnosy z ocenění, s rozšířením reverzního výnosu o 80 bps v posledních dvou letech na 7,21 TP3T. CTP očekává, že výnosy dosáhly vrcholu v sektoru Industrial & Logistics v regionu CEE. S většími pohyby výnosů na západoevropských trzích se výnosový rozdíl mezi CEE a západoevropskou logistikou vrátil k dlouhodobému průměru. CTP očekává, že se rozdíl ve výnosech bude dále snižovat v průběhu času, a to díky vyšším očekáváním růstu v regionu střední a východní Evropy.

CTP očekává další pozitivní růst ERV na pozadí pokračující poptávky nájemců, která je pozitivně ovlivněna sekulárními faktory růstu v regionu CEE. Úrovně nájemného ve střední a východní Evropě zůstávají dostupné; a navzdory výraznému růstu vycházely z výrazně nižších absolutních úrovní než v západoevropských zemích. V reálném vyjádření je nájemné na mnoha trzích střední a východní Evropy stále pod úrovní roku 2010.

EPRA NTA na akcii vzrostla z 15,92 EUR k 31. prosinci 2023 na 17,52 EUR k 30. září 2024, což představuje nárůst o 10,11 TP3T. Nárůst je způsoben především přeceněním (+1,29 EUR), specifickým upraveným EPRA EPS (+0,60 EUR), částečně kompenzovaným vyplacenou dividendou (-0,28 EUR).

Robustní rozvaha a silná likvidita

V souladu se svým proaktivním a obezřetným přístupem má skupina solidní likvidní pozici, která jí umožňuje financovat své růstové ambice, a to díky fixním nákladům na dluh a konzervativnímu profilu splácení.

Během prvních 9 měsíců roku skupina získala 1,8 miliardy EUR:

- Šestiletý zajištěný úvěr ve výši 100 milionů EUR se syndikátem italských a českých bank s fixní celkovou cenou 4,91 TP3T;

- šestiletý zelený dluhopis v hodnotě 750 milionů EUR v MS +220 bps při kuponu 4,75%;

- Sedmiletý zajištěný úvěr ve výši 90 milionů EUR s rakouskou bankou s fixní celkovou cenou 4,91 TP3T;

- sedmiletá zajištěná úvěrová facilita ve výši 168 milionů EUR se syndikátem slovenských a rakouských bank s fixní celkovou cenou 5,11 TP3T;

- Šestiletý zelený dluhopis ve výši 75 milionů EUR vydaný v únoru 2024 v MS +171 bps;

- pětiletá nezajištěná úvěrová facilita ve výši 500 milionů EUR se syndikátem mezinárodních bank s pevnou celkovou cenou 4,71 TP3T; a

- Sedmiletý zajištěný úvěr ve výši 150 milionů EUR navýšený syndikátem italských a českých bank s fixní celkovou cenou 4,35%.

Během roku CTP také dokončila dvě nabídky tendru na dluhopisy, odkoupila zpět 750 milionů EUR krátkodobých dluhopisů, realizovala kapitálový zisk ve výši 31,9 milionu EUR, snížila splatnosti dluhů v letech 2025 a 2026 a proaktivně rozšířila svůj profil splatnosti.

Likviditní pozice Skupiny činila 1,8 miliardy EUR, skládající se z 1,3 miliardy EUR v hotovosti a peněžních ekvivalentech a nevyčerpaných RCF ve výši 550 milionů EUR.

Průměrné náklady dluhu CTP činily 2,731 TP3T (31. prosince 2023: 1,951 TP3T), přičemž 99,71 TP3T dluhu bylo fixováno nebo zajištěno do splatnosti. Skupina nekapitalizuje úroky z vývoje, proto jsou všechny úrokové náklady zahrnuty do zisku a ztráty. Průměrná splatnost dluhu dosáhla 5,0 roku (31. prosince 2023: 5,3 roku).

První podstatná nadcházející splatnost Skupiny je 272 milionů EUR[2] dluhopis splatný v červnu 2025, který bude splacen z dostupných hotovostních rezerv.

LTV společnosti CTP dosáhla k 30. září 2024 hodnoty 44,91 TP3T, což je pokles z 46,21 TP3T k 30. červnu 2024 díky ABB[3]. CTP očekává, že LTV bude klesat, protože přecenění vývoje skupiny jsou plně zaúčtována.

Aktiva skupiny s vyšším výnosem díky jejich hrubému výnosu portfolia 6,51 TP3T vedou ke zdravé úrovni pákového efektu peněžních toků, který se také odráží v normalizovaném čistém dluhu vůči EBITDA ve výši 9,0x (31. prosince 2023: 9,2x), který Seskupte cíle tak, aby se udržely pod 10x.

Skupina měla k 30. září 2024 nezajištěný dluh 59% a zajištěný dluh 41%, s dostatkem rezervy v rámci smluv o testu zajištěného dluhu a testu nezatížených aktiv.

S racionalizací cen na trhu dluhopisů jsou nyní podmínky konkurenceschopnější než ceny na trhu bankovních úvěrů, což Skupině umožní více přeorientovat se na nezajištěné úvěry.

| 30. září 2024 | Covenant | |

| Test zajištěného dluhu | 19.5% | 40% |

| Test nezatížených aktiv | 190.6% | 125% |

| Poměr úrokového krytí | 2,75x | 1.5x |

Ve 3. čtvrtletí 2024 Moody's a S&P potvrdily úvěrový rating CTP Baa3 a BBB- se stabilním výhledem.

Dividenda a doporučení potvrzeny

Dynamika leasingu zůstává silná, se silnou poptávkou nájemců a snižující se novou nabídkou, což vede k pokračujícímu růstu nájemného. CTP má dobrou pozici, aby z těchto trendů těžila. Plynovod skupiny je vysoce ziskový a vede ho nájemce. YoC pro plynovod CTP se zvýšil na 10,4% díky klesajícím stavebním nákladům a růstu nájemného. Další fáze růstu je zabudována a financována s 1,9 milionu m2 ve výstavbě k 30. září 2024 s cílem dodat 1,2 – 1,3 milionu m2 v roce 2024.

Robustní kapitálová struktura CTP, disciplinovaná finanční politika, silný přístup na úvěrový trh, přední pozemková banka v oboru, vlastní stavební expertizy a hluboké vztahy s nájemci umožňují CTP plnit své cíle. CTP očekává, že v roce 2027 dosáhne příjmů z pronájmu ve výši 1,0 miliardy EUR, tažených dokončením vývoje, indexací a reverzí, a je na dobré cestě dosáhnout do konce desetiletí 20 milionů m2 GLA a 1,2 miliardy EUR příjmů z pronájmu.

Skupina potvrzuje své 0,80 – 0,82 EUR specifické pro společnost upravené doporučení EPRA EPS pro rok 2024, které se vzhledem k nárůstu akcií po ABB v září očekává směrem ke spodní hranici.

Dividendová politika společnosti CTP spočívá ve výplatě 70% - 80% upraveného zisku na akcii EPRA. Standardně se vyplácí dividenda ve formě poukázek, ale akcionáři se mohou rozhodnout pro výplatu dividendy v hotovosti.

WEBCAST A KONFERENČNÍ HOVOR PRO ANALYTIKY A INVESTORY

Dnes v 9:00 (GMT) a 10:00 (CET) bude společnost pořádat videoprezentaci a sezení s otázkami a odpověďmi pro analytiky a investory prostřednictvím živého internetového vysílání a audiokonference.

Chcete-li sledovat živé vysílání, zaregistrujte se na adrese:

https://www.investis-live.com/ctp/6707916fb2cedb000e393936/laper

Chcete-li se k prezentaci připojit telefonicky, vytočte prosím jedno z následujících čísel a zadejte přístupový kód účastníka. 427163.

Německo +49 32 22109 8334

Francie +33 9 70 73 39 58

Nizozemsko +31 85 888 7233

Spojené království +44 20 3936 2999

Spojené státy +1 646 787 9445

Stisknutím tlačítka *1 položíte otázku, tlačítkem *2 ji odvoláte nebo stisknutím tlačítka *0 požádáte o pomoc operátora.

Záznam bude k dispozici na webových stránkách CTP do 24 hodin po prezentaci: https://www.ctp.eu/investors/financial-reports/

FINANČNÍ KALENDÁŘ CTP

| Akce | Datum |

| Výsledky FY-2024 | 27. února 2025 |

| Výroční valná hromada | 22. dubna 2025 |

| Výsledky za 1. čtvrtletí 2025 | 8. května 2025 |

| Výsledky H1-2025 | 7. srpna 2025 |

| Dny kapitálového trhu | 24.–25. září 2025 |

| Výsledky 3. čtvrtletí 2025 | 6. listopadu 2025 |

KONTAKTNÍ ÚDAJE PRO DOTAZY ANALYTIKŮ A INVESTORŮ:

Maarten Otte, vedoucí oddělení pro vztahy s investory

Mobilní telefon: +420 730 197 500

E-mail: [email protected]

KONTAKTNÍ ÚDAJE PRO DOTAZY MÉDIÍ:

Patryk Statkiewicz, vedoucí marketingu a PR skupiny

Mobilní telefon: +31 (0) 629 596 119

E-mail: [email protected]

O CTP

CTP je největším evropským registrovaným vlastníkem, developerem a správcem logistických a průmyslových nemovitostí podle hrubé pronajímatelné plochy, k 30. září 2024 vlastní 12,6 milionů m2 GLA v 10 zemích. CTP certifikuje všechny nové budovy podle BREEAM Velmi dobré nebo lepší a vydělané hodnocení ESG se zanedbatelným rizikem od Sustainalytics, což podtrhuje její závazek být trvale udržitelným podnikem. Pro více informací navštivte firemní web CTP: www.ctp.eu

Odmítnutí odpovědnosti

Toto oznámení obsahuje určitá výhledová prohlášení týkající se finanční situace, výsledků hospodaření a podnikání společnosti CTP. Tato výhledová prohlášení lze identifikovat podle použití výhledové terminologie, včetně výrazů "věří", "odhaduje", "plánuje", "projektuje", "předpokládá", "očekává", "zamýšlí", "cíle", "může", "má za cíl", "pravděpodobně", "by", "mohl", "může mít", "bude" nebo "měl by" nebo v každém případě jejich negativních nebo jiných variant či srovnatelné terminologie. Výhledová prohlášení se mohou podstatně lišit a často se také liší od skutečných výsledků. V důsledku toho by se na žádné výhledové prohlášení neměl vztahovat nepatřičný vliv. Tato tisková zpráva obsahuje vnitřní informace ve smyslu čl. 7 odst. 1 nařízení (EU) č. 596/2014 ze dne 16. dubna 2014 (nařízení o zneužívání trhu).

[1] Při kombinaci místního CPI a CPI EU-27 / eurozóny pouze omezený počet stropů.

[2] Dlužná částka po vypořádání nabídky dne 28. června 2024.

[3] K 30. září 2024 bylo vypořádáno pouze 227 milionů EUR volně pohyblivých akcií, 73 milionů EUR akcií upsaných generálním ředitelem a zakladatelem bylo vypořádáno v prvním říjnovém týdnu po výplatě dividendy.

Přihlaste se k odběru novinek

Buďte první u nových příležitostí. Nejnovější projekty, volné prostory i tržní trendy od lídra na trhu – přímo do vaší schránky. Přihlaste se k odběru a nic důležitého vám neunikne.