Kết quả CTP NV năm tài chính 2025

NET RENTAL INCOME UP 14.1% YOY, LIKE-FOR-LIKE RENTAL GROWTH OF 4.5% AND EPRA NTA PER SHARE UP 12.8% YOY TO €20.39 WITH MEDIUM-TERM GROWTH AMBITION REITERATED

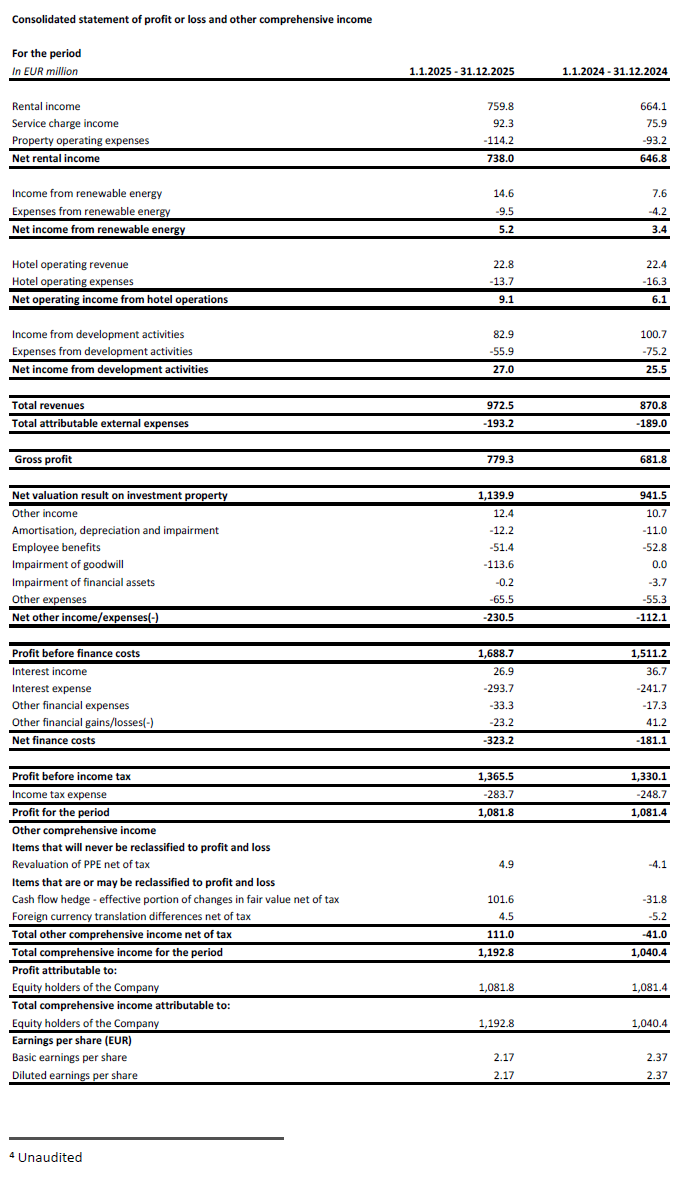

AMSTERDAM, 26 February 2026 – CTP N.V. (CTPNV.AS), (“CTP”, the “Group” or the “Company”) recorded Gross Rental Income of €759.8 million in the year, up 14.4% y-o-y with like-for-like rental growth of 4.5% – an accelerated growth rate versus FY-2024 and mainly driven by indexation and reversion on renegotiations and expiring leases. As at 31 December 2025, the annualised rental income increased to €839.7 million. Together with potential rental income of €152 million coming from 2.0 million sqm of GLA under construction, CTP is on track for the €1 billion rental income target by 2027. Occupancy remained at 93% and the rent collection rate stood at 99.7%.

In 2025, CTP delivered 1,325,000 sqm at a Yield on Cost (“YoC”) of 10.4% with 88% let at completion, bringing the Group’s standing portfolio to 14.6 million sqm of GLA. Strong leasing demand supported by structural tailwinds mainly related to rising disposable incomes in the CEE markets and nearshoring and localisation trends, translated to a record 2,325,000 sqm of leases signed at 4% higher rent levels compared to 2024.

The Gross Asset Value (“GAV”) increased by 15.7% to €18.5 billion. EPRA NTA per share increased by 12.8% to €20.39 resulting in a Total Accounting Return of 16.1% in 2025, maintaining CTP’s industry-leading growth and return profile.

Company-specific adjusted EPRA earnings increased by 11.3% y-o-y to €405.0 million. CTP’s Company-specific adjusted EPRA EPS amounted to €0.85, an increase of 6.3%, slightly below the guidance mainly due to the timing of some development completions moving to Q1-2026. The Group sets Company specific adjusted EPRA EPS guidance for 2026 of €1.01 – €1.03. This implies y-o-y growth of 9% – 11% compared to the 2025 result, adjusted for capitalised interest, still affected by moderate refinancing headwind in 2026, with an acceleration expected for the years after.

CTP expects to deliver between 1.4 million sqm – 1.7 million sqm in 2026, utilizing its industry-leading landbank of 33.8 million sqm, of which 23.9 million sqm is owned and on-balance sheet. This landbank secures substantial future growth potential for CTP, with 55% located in or around existing parks, and 39% located in new parks, each with a potential of over 100,000 sqm GLA. Combined with its industry-leading YoC, CTP expects to continue to generate double-digit NTA growth in the years to come.

The strength of CTP’s platform was underlined in September by S&P’s credit rating upgrade from BBB- to BBB with a stable outlook. The upgrade follows the Q2-2025 action of Moody’s, upgrading CTP’s outlook from Stable to Positive.

We made our first investment in Italy in 2025 – our 11th country. We have already made a strong start - the deal secured an 8.7 million sqm landbank including immediate development potential, with 200,000 sqm scheduled for completion in 2026. CTP expects to deliver 250,000 sqm - 300,000 sqm annually in Italy from 2027 onwards, with a target YoC between 8.5% - 9.5% - a key contributor to the group’s GLA growth moving forward.

Our landbank of 33.8 million sqm represents significant upside for continued shareholder value creation. Our unique integrated model as operator, developer, and growth engine gives us the capacity and flexibility to capture opportunities, both in our existing markets and potential new markets, in line with our global ambitions.

Structural trends such as nearshoring and manufacturing ‘in Europe, for Europe’ are accelerating, illustrated by the continued growth of Asian manufacturing tenants in our portfolio. In the strong and resilient CEE region we continue to see growth in domestic consumption, while in Germany we benefit from the modernisation of the economy.”

Điểm sáng nổi bật[1]

| Tính bằng triệu euro | FY-2025 | FY-2024 | % thay đổi | Q4-2025 | Q4-2024 | % thay đổi |

| Tổng thu nhập cho thuê | 759.8 | 664.1 | +14.4% | 197.8 | 175.7 | +12.6% |

| Thu nhập cho thuê ròng | 738.0 | 646.8 | +14.1% | 189.1 | 170.9 | +10.6% |

| Kết quả định giá ròng bất động sản đầu tư | 1,139.9 | 941.5 | +21.1% | 338.3 | 337.4 | +0.3% |

| Lợi nhuận trong kỳ | 1,081.8 | 1,081.4 | +0.0% | 218.9 | 344.3 | -36.4% |

| Thu nhập EPRA điều chỉnh theo công ty cụ thể | 405.0 | 364.0 | +11.3% | 99.8 | 94.2 | +6.0% |

| Bằng € | FY-2025 | FY-2024 | % thay đổi | Q4-2025 | Q4-2024 | % thay đổi |

| EPS EPRA điều chỉnh theo công ty cụ thể | 0.85 | 0.80 | +6.3% | 0.21 | 0.20 | +3.5% |

|

|

||||||

| Tính bằng triệu euro | 31 Dec. 2025 | 31 Dec. 2024 | % thay đổi | |||

| Bất động sản đầu tư (“IP”) | 16,835.1 | 14,655.3 | +14.9% | |||

| Bất động sản đầu tư đang phát triển (“IPuD”) | 1,368.1 | 1,076.8 | +27.1% | |||

| 31 Dec. 2025 | 31 Dec. 2024 | % thay đổi | ||||

| EPRA NTA trên mỗi cổ phiếu | €20.39 | €18.08 | +12.8% | |||

| YoC dự kiến của các dự án đang xây dựng | 10.0% | 10.3% | ||||

| Giá trị vòng đời (LTV) | 46.1% | 45.3% |

Continued solid tenant demand drives rental growth

During 2025, CTP signed leases for 2,325,000 sqm including Italy, an increase of 10% compared to 2024, with an average monthly rent per sqm of €5.81 (2024: €5.68). Adjusting for the differences among the country mix, market rents increased on average by 4%. This is ahead of inflation, reflecting the healthy supply / demand balance in the CEE region.

| Hợp đồng thuê được ký theo mét vuông | Qúy 1 | Qúy 2 | Qúy 3 | Qúy 4 | Năm tài chính |

| 2023 | 297,000 | 552,000 | 585,000 | 542,000 | 1,976,000 |

| 2024 | 336,000 | 582,000 | 577,000 | 618,000 | 2,113,000 |

| 2025 | 416,000 | 599,000 | 562,000 | 748,000[2] | 2,325,000 |

| Tiền thuê trung bình hàng tháng được ký kết theo mét vuông (€) | Qúy 1 | Qúy 2 | Qúy 3 | Qúy 4 | Năm tài chính |

| 2023 | 5.31 | 5.56 | 5.77 | 5.81 | 5.69 |

| 2024 | 5.65 | 5.55 | 5.69 | 5.79 | 5.68 |

| 2025 | 6.17 | 5.91 | 5.64 | 5.70 | 5.81 |

In total, 71% of leases signed were with existing tenants, in line with CTP’s business model of growing with existing tenants at existing parks.

Cashflow generation through standing portfolio

CTP’s average market share in the Czech Republic, Romania, Hungary, and Slovakia came to 28.4% as at 31 December 2025 and it remains the largest owner and developer of industrial and logistics real estate assets in those markets. The Group is also the market leader in Serbia and Bulgaria.

With more than 1,500 clients, CTP has a wide and diversified international tenant base, consisting of blue-chip companies with strong credit ratings. CTP’s tenants represent a broad range of industries, including manufacturing, high-tech/IT, automotive, e-commerce, retail, wholesale, and 3PLs. The tenant base is highly diversified, with no single tenant accounting for more than 2.2% of the Company’s annual rent roll, which leads to a stable income stream. CTP’s top 50 tenants only account for 33% of its rent roll and the vast majority of our largest clients rent space at multiple CTParks.

The Company’s occupancy remains flat at 93% (2024: 93%). The Group’s client retention rate remains strong at 81% (2024: 87%) and demonstrates CTP’s ability to leverage long-standing client relationships. The portfolio WAULT stood at 6.1 years (2024: 6.4 years).

Rent collection level stood at 99.7% in 2025 (2024: 99.8%), with no deterioration in the payment profile of tenants.

Rental income in 2025 amounted to €759.8 million, up 14.4% y-o-y on an absolute basis, mainly driven by deliveries and like-for-like growth. On a like-for-like basis, rental income grew 4.5%, thanks to indexation and reversion on renegotiations and expiring leases.

Net Rental Income increased 14.1% y-o-y to €738.0 million, with a service charge leakage of the Net Rental Income to Rental Income ratio of 97.1% (2024: 97.4%)

An increasing proportion of the rental income generated by CTP’s investment portfolio benefits from inflation protection. Since end-2019, the Group’s new lease agreements include a CPI-linked indexation clause, which calculates annual rental increases as the higher of:

- mức tăng cố định 1,5%–2,5% một năm; hoặc

- chỉ số giá tiêu dùng[3].

As at 31 December 2025, 73% of income generated by the Group’s portfolio includes this double indexation clause, and the Group expects this to increase further.

The reversionary potential stood at 14.1% at FY-2025 with CTP also continuing to successfully capture rent reversion. New leases have been signed continuously above the Estimated Rental Value (“ERV”), illustrating continued strong market rental growth and supporting valuations. New rents signed were up 4% YoY, adjusting for country mix and reaching record full year levels as tenants continue to recognise the high value of our CTP product offering.

The annualised rental income came to €839.7 million as at 31 December 2025, an increase of 13.1% y-o-y, showcasing the strong cash flow growth of CTP’s investment portfolio.

2025 developments delivered with a 10.4% YoC and 88% let at delivery

CTP tiếp tục đầu tư có tính toán vào dự án có lợi nhuận cao của mình.

In 2025, the Group completed 1,325,000 sqm of GLA (2024: 1,286,000 sqm). The developments were delivered at a YoC of 10.4%, 88% let and will generate contracted annual rental income of €152 million. Some of the main 2025 deliveries included 179k sqm at CTPark Bucharest West, 65k sqm at CTPark Budapest Erd and 58k sqm at CTPark Brno.

Average construction costs in 2024 were around €500 per sqm and remained stable in 2025. This allowed the Group to continue to deliver its industry-leading YoC above 10%, which is also supported by CTP’s unique park model and in-house construction and procurement expertise.

As at 31 December 2025, the Group had 2.0 million sqm of buildings under construction with a potential rental income of €152 million and sector-leading expected YoC of 10.0%. During 2025 the group started a record 1.5 million sqm of new projects.

CTP has a long track record of delivering sustainable growth through its tenant-led development at its existing parks. 77% of the Group’s projects under construction are at existing parks, while a further 10% across new parks which have the potential to be developed to more than 100,000 sqm of GLA. Planned 2026 deliveries are 30% pre-let (2024: 35%). This lower figure in 2025 is more than offset by the 175,000 sqm (FY-2025: 80,000 sqm) of leases that are already signed for future projects where construction has not yet commenced – a further illustration of continued occupier demand. The pre-let rate in existing parks stood at 23%, while at new parks the pre-let figure was at 62%, showcasing the low risk embedded in the pipeline. CTP expects to reach 80%-90% pre-letting at delivery, in line with historical performance. As CTP acts as general contractor in most markets, it is fully in control of the process and timing of deliveries, allowing the Company to speed-up or slow-down depending on tenant demand, while also offering tenants flexibility in terms of their building requirements. In 2026, the Group expects to deliver between 1.4 million sqm – 1.7 million sqm of GLA.

CTP’s landbank amounted to 33.8 million sqm as at 31 December 2025 (31 December 2024: 26.4 million sqm). The Group is focusing on mobilising its existing landbank, as well as looking globally for additional land acquisition opportunities. 55% of the landbank is located at CTP’s existing parks, while 39% is in, or is adjacent to, new parks which have the potential to grow to more than 100,000 sqm. 29% of the landbank was secured by options, while the remaining 71% was owned and accordingly reflected in the balance sheet.

Assuming a build-up ratio of 2 sqm of land to 1 sqm of GLA, CTP can build approximately 17 million sqm of GLA on its secured landbank. CTP’s land is held on balance sheet at around €60 per sqm and construction costs amount on average to approximately €500 per sqm, bringing total investment costs to approximately €620 per sqm. The Group’s standing portfolio is valued around €1,050 per sqm, resulting in a revaluation potential of around €430 per sqm built.

Kiếm tiền từ kinh doanh năng lượng

CTP tiếp tục kế hoạch mở rộng triển khai hệ thống điện mặt trời. Với chi phí trung bình khoảng 750.000 euro/MWp, Tập đoàn đặt mục tiêu lợi nhuận ròng (YoC - Năng suất trên chi phí) là 15% cho các khoản đầu tư này.

CTP has an installed PV capacity of 154 MWp. In 2025 revenues from renewable energy came to €14.6 million, up 92% y-o-y mainly driven by the increase in capacity installed throughout 2025.

CTP’s sustainability ambitions go hand-in-hand with an increasing number of tenants requesting green energy from photovoltaic systems, as they provide them with i) improved energy security, ii) a lower cost of occupancy, iii) compliance with increased regulation iv) compliance with their clients’ requirements and v) the ability to fulfil their own ESG ambitions.

Kết quả định giá được thúc đẩy bởi đường ống và định giá lại tích cực của danh mục đầu tư hiện tại

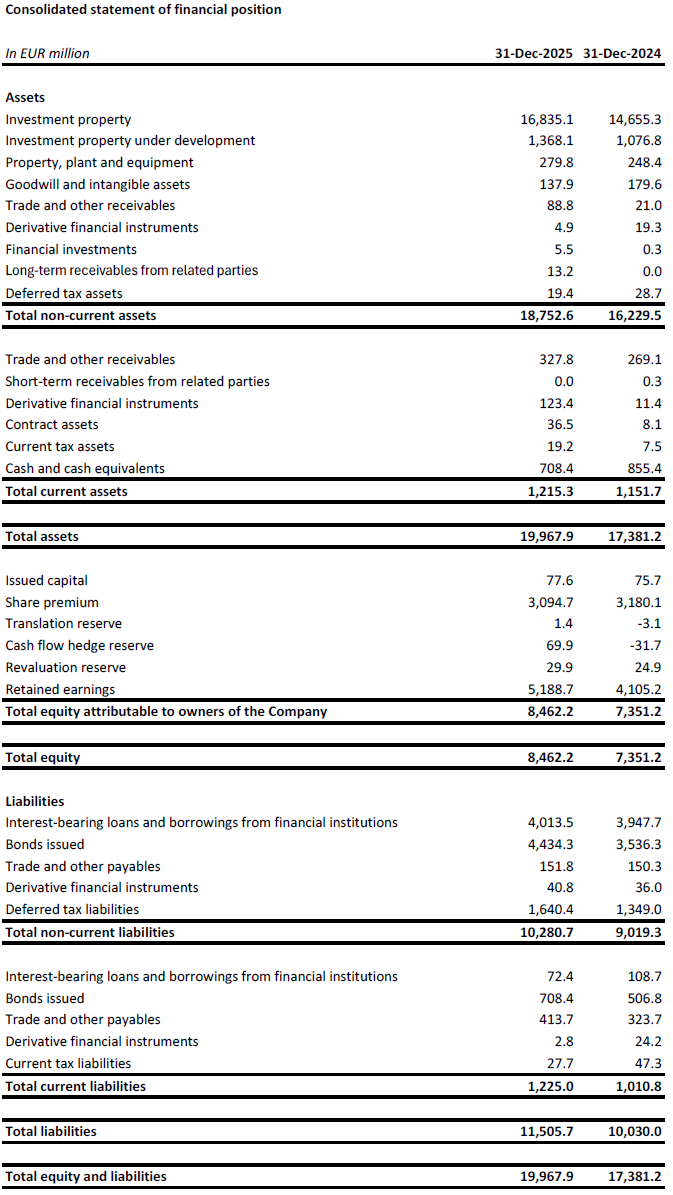

Investment Property (“IP”) valuation increased from €14.7 billion as at 31 December 2024 to €16.8 billion as at 31 December 2025, driven by the transfer of completed projects from Investment Property under Development (“IPuD”) to IP and positive revaluation of standing portfolio.

IPuD increased by 27.1% from 31 December 2024 to €1.4 billion as at 31 December 2025, driven by the CAPEX spent, the revaluation due to increased pre-letting and construction progress, and the start of new construction projects.

GAV increased to €18.5 billion as at 31 December 2025, up 15.7% compared to 31 December 2024.

The revaluation in 2025 came to €1,139.9 million, driven by the positive revaluation of IPuD projects (+€421.6 million), landbank (+€69.8 million), and the standing assets (+€648.6 million).

CTP expects further ERV growth in line with inflation on the back of continued tenant demand, which is positively impacted by the secular growth drivers in the CEE region. CEE rental levels remain affordable; despite the strong growth seen as they have started from significantly lower absolute levels than in Western European countries. In real terms, rents in many Central and Eastern European (“CEE”) markets are still below 2010 levels.

The Group’s portfolio has conservative average reversionary yield of 6.9%. The yield differential between CEE and Western European logistics is expected to decrease over time, driven by the higher growth expectations for the CEE region and increasing activity in the investment markets.

EPRA NTA per share increased from €18.08 as at 31 December 2024 to €20.39 as at 31 December 2025, representing an increase of 12.8% y-o-y.

Bảng cân đối kế toán vững mạnh và vị thế thanh khoản mạnh

Theo cách tiếp cận chủ động và thận trọng, Tập đoàn được hưởng lợi từ vị thế thanh khoản vững chắc để tài trợ cho tham vọng tăng trưởng, với chi phí nợ cố định và hồ sơ trả nợ thận trọng.

During 2025, the Group secured €2.4 billion to fund its organic growth:

- a €1.0 billion dual-tranche green bond with a €500 million six-year tranche at MS +145bps at a coupon of 3.625% and a €500 million ten-year tranche at MS +188bps at a coupon of 4.25%;

- a JPY30 billion (€185 million equivalent) five-year unsecured sustainability-linked loan facility with a syndicate of Asian banks at TONAR +130bps and fixed all-in cost of 4.1%;

- a €500 million five-year unsecured sustainability-linked loan facility with a syndicate of 13 European and Asian banks at fixed all-in cost of 3.7%; and

- a €600 million green bond with a 6.5y maturity at MS +118bps at a coupon of 3.625%.

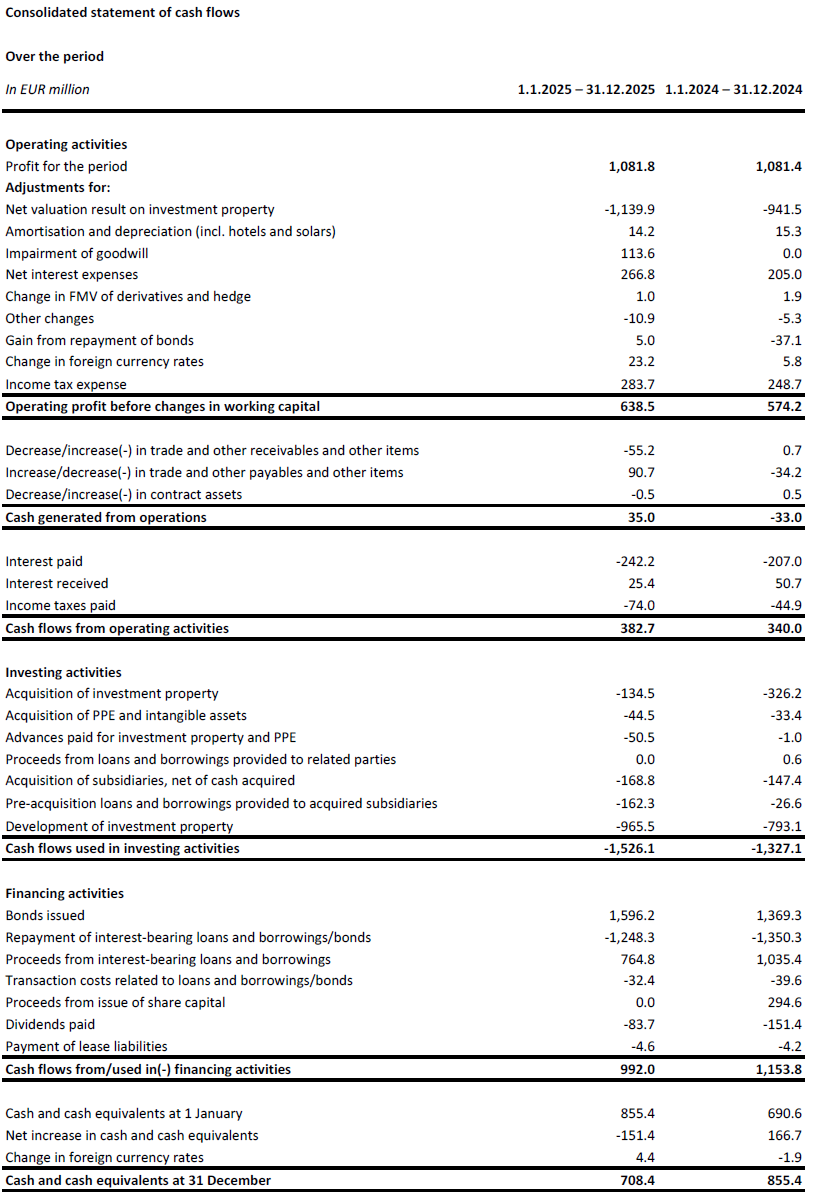

CTP continued to actively manage its bank loan portfolio in 2025. Margin reduction on a further €288 million of secured bank loans was negotiated, and a €609 million were prepaid. Both allowed CTP to achieve material interest rate savings, reducing its overall cost of debt going forward.

The Group’s liquidity position stood at €2.0 billion, comprised of €0.7 billion in cash and cash equivalents, and an undrawn RCF of €1.3 billion.

CTP’s average cost of debt stood at 3.3% (2024: 3.1%), and is now close to our marginal cost of debt. The increase compared to year-end 2024 is due to new funding at a higher rate than our historic average cost of debt. This is expected to increase only slightly in 2026 and from 2027 we expect no material average cost of debt impact from further refinancings. 99.9% of the debt is fixed rate or hedged until maturity.

The average debt maturity came to 4.8 years (2024: 5.0 years).

The Group repaid a €272 million bond in June 2025 and €185 million bond in October 2025 from its available cash reserves.

Additionally, CTP repaid €350 million of bond in January 2026 from available cash reserves. CTP also issued €500 million green bond with a 4.5y maturity at MS +92bps at a coupon of 3.375%, followed by concurrent repurchase of €216 million of bonds dated 2030 with a coupon of 4.75% in January 2026.

CTP’s LTV came to 46.1% as at 31 December 2025, slightly above the target range of 40%-45% due to the acquisition and market entry in Italy in Q4-2025.

The Group’s higher yielding assets, thanks to their gross portfolio yield of 6.5%, lead to a healthy level of cash flow leverage that is also reflected in the normalised Net Debt to EBITDA of 9.3x (2024: 9.1x), which the Group targets to keep below 10x.

The ICR stood at 2.5x, well above the covenant threshold of 1.5x. The ICR decreased and bottomed out in the first half of 2025 due to increased cost of debt and refinancing cheaper debt at current market levels. Thanks to strong demand and industry leading YoC over 10%, ICR has increased since the second half of 2025, as each euro invested in the pipeline improves the ICR.

The Group’s debt comprised of 70% unsecured debt and 30% secured as at 31 December 2025, with ample headroom under its Secured Debt Test and Unencumbered Asset Test covenants.

As pricing in the bond market rationalised, the conditions are more competitive than the pricing in the bank lending market, which allows the Group to re-balance more towards unsecured lending.

| 31 December 2025 | Giao ước | |

| Kiểm tra nợ có bảo đảm | 13.7% | 40% |

| Kiểm tra tài sản không bị ràng buộc | 187.3% | 125% |

| Tỷ lệ bao phủ lãi suất | 2,5 lần | 1,5x |

In Q3-2025, S&P upgraded CTP’s credit rating from BBB- to BBB with a stable outlook. In January 2025, CTP was assigned an A- credit rating with a stable outlook by the Japanese rating agency JCR. In Q2-2025, Moody’s upgraded outlook from stable to positive on its Baa3 credit rating.

Global ambition

During the 2025 Capital Markets Day CTP’s new ambition of 30 million sqm of GLA by 2030 was announced. This ambition will be primarily delivered from the existing landbank, complimented with accretive land-led acquisitions. The ‘Growth Engine’ of CTP, leveraging strong existing tenant relationships, also drives expansion into new geographies. In 2025 CTP entered Italy, a key contributor to the Group’s future development deliveries with over 1 million sqm to be delivered by 2030. CTP’s intended entry into Vietnam – which will be the start of CTP Asia – will also enhance the future income accretion and development potential of the group. The Group’s landbank has the potential to deliver significant future development profit – value that CTP will unlock to create industry leading shareholder returns.

Capitalisation of interest – Reporting harmonisation

From 2026 onwards, CTP will in accordance with IAS23, capitalise interest expenses associated with qualifying development activities. Not only does this accounting treatment achieve the objective of measuring the cost that fully reflects the investment made by CTP in a development asset, but it also ensures that investors and other relevant stakeholders are able to compare CTP to other listed market participants more easily. In line with market practice CTP is now adopting the policy to to capitalise interest charges – at a rate equal to it’s average cost of debt – on development activities.

2026 Guidance – accelerating EPS growth

Leasing dynamics remain strong, with robust occupier demand, and decreasing new supply leading to continued rental growth. CTP is well positioned to benefit from these trends. The Group’s pipeline is highly profitable, and tenant led. The YoC for CTP’s current pipeline remains at an industry leading 10.0%. The next stage of growth is built-in and financed, with 2.0 million sqm under construction as at 31 December 2025, with a target to deliver between 1.4 million sqm – 1.7 million sqm in 2026.

CTP’s robust capital structure, disciplined financial policy, strong credit market access, industry-leading landbank, in-house construction expertise and deep tenant relationships allow CTP to deliver on its targets. CTP expects to reach €1.0 billion annualised rental income in 2027, driven by development completions, indexation and reversion. The medium-term ambition of achieving 30 million sqm of GLA, doubling the current portfolio also is reiterated.

The Group sets Company specific adjusted EPRA EPS guidance for 2026 of €1.01 – €1.03. This implies year-on-year growth of 9% at the lower end of the range, rising to 11% at the top end of the range when compared to the 2025 result, adjusting for capitalised interest. The EPS growth is driven by development deliveries becoming income-producing, alongside strong underlying growth, with around 4% like-for-like rental growth expected, primarily driven by indexation, but also incorporating the moderate headwind due to refinancing of low coupon bonds in 2026. We expect an acceleration of Company adjusted EPRA EPS growth for the years after given our average cost of debt is now approaching our marginal cost of funding and we expect to maintain our leading shareholders returns profile.

Cổ tức

CTP proposes a final 2025 dividend of €0.32 per ordinary share, which will, subject to approval by the AGM, be paid on 12 June 2026. This will bring the total 2025 dividend to €0.63 per ordinary share, which represents a Company specific adjusted EPRA EPS pay-out of 74% – in line with the Group’s dividend policy to pay-out 70%-80% – and growth of 6.8% compared to 2024. For 2026, the dividend payout ratio range remains unchanged. The default dividend is scrip, but shareholders can opt for payment of the dividend in cash.

Báo cáo tài chính[4]

WEBCAST VÀ HỘI NGHỊ TRỰC TUYẾN DÀNH CHO CÁC NHÀ PHÂN TÍCH VÀ NHÀ ĐẦU TƯ

Hôm nay vào lúc 9 giờ sáng (GMT) và 10 giờ sáng (CET), Công ty sẽ tổ chức buổi thuyết trình video và phiên hỏi đáp dành cho các nhà phân tích và nhà đầu tư, thông qua webcast trực tiếp và cuộc gọi hội nghị âm thanh.

Để xem chương trình phát trực tiếp trên web, vui lòng đăng ký trước tại:

https://www.investis-live.com/ctp/6966135a60049000159a42e5/qplcg

Để tham gia buổi thuyết trình qua điện thoại, vui lòng quay số một trong các số sau và nhập mã truy cập của người tham gia 375644.

Đức +49 32 22109 8334

Pháp +33 9 70 73 39 58

Hà Lan +31 85 888 7233

Vương quốc Anh +44 20 3936 2999

Hoa Kỳ +1 646 233 4753

Nhấn *1 để đặt câu hỏi, *2 để rút lại câu hỏi hoặc *0 để được hỗ trợ từ nhân viên tổng đài.

Bản ghi âm sẽ có trên trang web của CTP trong vòng 24 giờ sau buổi thuyết trình: https://www.ctp.eu/investors/financial-results/

LỊCH TÀI CHÍNH CTP

| Hoạt động | Ngày |

| Q1-2026 results | 30 April 2026 |

| Annual General Meeting | 20 May 2026 |

| H1-2026 results | 30 July 2026 |

| Ngày thị trường vốn | 22-23 September 2026 |

| Q3-2026 results | 29 October 2026 |

THÔNG TIN LIÊN HỆ ĐỂ ĐƯỢC TƯ VẤN TỪ NHÀ PHÂN TÍCH VÀ NHÀ ĐẦU TƯ:

Rob Jones, Head of Investor Relations & PR

Di động: +420 605 482 873

E-mail: [email protected]

Pavel Švihálek, Giám đốc cấp vốn và IR

Di động: +420 724 928 828

E-mail: [email protected]

THÔNG TIN LIÊN HỆ CHO CÁC YÊU CẦU TRUYỀN THÔNG:

E-mail: [email protected]

Giới thiệu về CTP

CTP is Europe’s largest listed owner, developer, and manager of logistics and industrial real estate by gross lettable area, owning 14.6 million sqm of GLA across 11 countries as at 31 December 2025. CTP certifies all new buildings to BREEAM Very good or better and earned a negligible-risk ESG rating by Sustainalytics, underlining its commitment to being a sustainable business. For more information, visit CTP’s corporate website: www.ctp.eu

Tuyên bố miễn trừ trách nhiệm

The audit procedures by statutory auditors are in progress.

Thông báo này chứa một số tuyên bố hướng tới tương lai liên quan đến tình hình tài chính, kết quả hoạt động và kinh doanh của CTP. Những tuyên bố hướng tới tương lai này có thể được nhận biết bằng cách sử dụng các thuật ngữ hướng tới tương lai, bao gồm các thuật ngữ “tin rằng”, “ước tính”, “kế hoạch”, “dự án”, “dự đoán”, “kỳ vọng”, “dự định”, “mục tiêu”, “có thể”, “nhắm tới”, “có khả năng”, “sẽ”, “có thể”, “có thể có”, “sẽ” hoặc “nên” hoặc, trong mỗi trường hợp, các biến thể tiêu cực hoặc các biến thể khác hoặc thuật ngữ tương đương của chúng. Các tuyên bố hướng tới tương lai có thể và thường khác biệt đáng kể so với kết quả thực tế. Do đó, không nên áp đặt bất kỳ ảnh hưởng không đáng có nào lên bất kỳ tuyên bố hướng tới tương lai nào. Thông cáo báo chí này chứa thông tin nội bộ theo định nghĩa tại Điều 7(1) của Quy định (EU) 596/2014 ngày 16 tháng 4 năm 2014 (Quy định về Lạm dụng Thị trường).

[1] Unaudited

[2] Including Italy

[3] Với sự kết hợp giữa CPI địa phương và EU-27/Khu vực đồng tiền chung châu Âu, số lượng mũ giới hạn.

[4] Unaudited

Đăng ký nhận bản tin

Nhận những thông tin chuyên sâu mới nhất từ đơn vị dẫn đầu thị trường bất động sản công nghiệp.